Download

1 / 117

1.17k likes | 1.32k Views

Expenditure Statement Reconciliation and Review. FIN 160. Course Modules. Overview Reconciliation Review Certification Reconciling Items Salaries. Module 1: Overview. Module 1 Objectives: At the end of this module you will be able to:

E N D

Course Modules • Overview • Reconciliation • Review • Certification • Reconciling Items • Salaries

Module 1: Overview Module 1 Objectives: At the end of this module you will be able to: Explain the role of reconciliation, review, and certification and why we have internal controls Contrast two types of internal controls and explain the role of reconciliation

Stanford’s Sources of Revenue • Stanford University is a $3.2 billion non-profit organization. The University's revenue includes: • Sponsored Research • Student Income • Gifts • Investment Income Sources of Revenue

Reconciling Is an Internal Control • Internal controls are practices that help prevent errors and irregularities from occurring • If errors or irregularities do occur, they are detected in a timely manner • Consequences arising from reporting errors are kept to a minimum and are quickly resolved

Internal Controls Types • Preventive controls attempt to deter or prevent undesirable events from occurring. They are proactive controls that help to prevent a loss. • Examples: • Proper approval and authorization • Segregation of duties • Adequate documentation • Physical control over assets • Detective controls attempt to detect undesirable acts after they have occurred. They provide evidence that a loss has occurred but do not prevent a loss from occurring. • Examples: • Reconciliation, Review, Certification • Analysis of variance • Physical inventory audit

Reconciliation • Reconciliation is the process of comparing the entries on reports to those on supporting documents and, if differences exist between them, finding the cause and bringing the two records into agreement.

Review • Review is inspection: a formal examination that analyzes reasonability of charges and confirms that they are allowable, beneficial, and represent current level of effort expended on the project.

Certification • Certification is an official examination of reconciled statements between the reviewer and the Principal Investigator (PI). The PI's certification assures that all expenses charged to the account are allowable, allocable to the project, and reasonable. The certification also assures that expenditures are for items or services purchased and used during the project period as specified by the award.

Why We Must Reconcile • Stanford’s Code of Conduct (AGM 1) states: “All accounts, financial reports … must be accurate, clear and complete” • Transaction coding errors affect financial reports and subsequent decisions • University imposes stewardship responsibilities for expenditures

Review • Why do we have internal controls? • Contrast the two types of internal controls.

Module 2: Reconciliation Module 2 Objectives: At the end of this module you will be able to: • Read and understand an expenditure report • Reconcile non-salary transactions shown on your expenditure statements

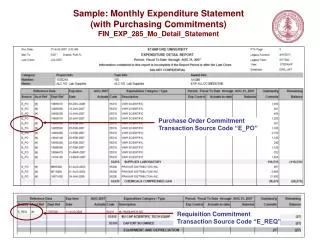

Expenditure Detail Report • The Expenditure Detail Report is a financial report which summarizes budgets, expenditures, and balances for an account. • The report is available via ReportMart3 on or after the 6th workday of the following month.

Obtaining Your Expenditure Report • Administrators can choose to have their Monthly Expenditure Statement (285) printed centrally and mailed to the Task Manager or to print them on their local printer. • When printed centrally, the report will be in either PTD (project-to-date) or FTD (fiscal-to-date) format depending on the type of PTA requested. • When printed locally, use of the PTD prompt will ensure appropriate results when conducting a search that will return both FTD and PTD types of Awards.

Opting Out of Hard Copies • Task Managers or Department Administrators can opt-in or opt-out of receiving hard copies of Expenditure Statements. • Download the template from http://fingate.stanford.edu/staff/finreporting/quicksteps/opt_hardcopy_mo_exp_statement.html • Follow instructions to complete template and e-mail to: Sponsored: lerwin@stanford.edu Non-sponsored: jeand@stanford.edu

Case Study #1 • The Expenditure Report • Now let’s take a look at an actual report

Reconciling Reports • Reconciliation is the process of comparing the entries on reports to those on supporting documents and resolving any discrepancies. • Reconciliation should occur regularly, after month end close.

Why Reconciling Is Important • Ensures transactions are valid and accurately recorded • Ensures all transactions are recorded • Ensures transactions are properly authorized • Ensures transactions are recorded in a timely manner • Reconciliation should occur regularly, after month end close

Reconcile vs. Review Where the inspection occurs

Basic Reconciling Steps • Gather appropriate backup (source) documents and information • Verify recorded transactions • Verify commitments • Correct errors • Initial and date reports

Step 1 Gather Documents • Expenditure reports • Source Documents, such as • Purchase orders • Invoices • Receiving documents • Purchase cards receipts • Prior month report(s) with corrections / notations • Fund restrictions • Tools & Resources

Fund Restrictions • Sponsored Projects • Grant or Contract • REF 216 Award Config Report (quick reference) • Other awards • REF 225 Fund Authorization • Your department’s mechanism for summarizing restrictions Award Type List Values

Where to Find Help • Check the Expenditure web site for Report Job Aid • Sample reports have live links for additional information about many fields Expenditure Report Job Aid

Resources & Tools • Reference Code Table • Coding tools • Unallowable Costs • List of Unallowable Expenditure Types • Expenditure Type Lookup (Expenditure Codes and Descriptions) • Coding a Transaction Flowchart • Monthly Reconciliation Guidance Monthly Reconciliation Guidance Coding Transaction Flowchart Reference Code Table

Step 2 Verify Recorded Transactions • Verify transactions & compare each transaction on the Expenditure Detail Report to source documents as required • Confirm overhead rates (burdening) • Investigate questionable transactions • Check to see if all expected transactions are on the report • Review “pending / commitment file” if applicable • Check prior expenditure statements for corrections that should appear on current statement

Investigate Questionable Transactions • Review recorded transactions and investigate those that you don't recognize or appear unusual. • Compare transactions to source documents as needed. • Review infrequent transactions.

Investigation Questions • Why might an invoice payment not appear on the expenditure report? • What does Accounts Payable require in order to pay a vendor? • Why might an iJournal not go through in the same month it was submitted?

Investigation Suggestions (continued) Take FIN-0210 Intro to iJournals for further training

What Is Burdening? • Certain University infrastructure, administrative, and benefit costs cannot easily be attributed to specific programs or activities. • The University assesses a charge, or burden rate, on certain activities to recover a portion of these costs, which include: • Facilities and Administrative Costs (indirect costs) • Infrastructure • Staff Benefits • Additional information about these burdens and specific rates is available on the Stanford Rates page. Stanford Rates Page

Find the Correct Rate • Facilities & Administrative Cost (F&A) for most sponsored projects • Infrastructure Charge (ISC) for most non-sponsored projects Implementing Infrastructure

Step 3 Verify Commitments • What are commitments? • They are firm obligations generated in our financial systems • Amount shown is based on certain salary obligations and expenditure transactions in process

Hard Commitments (Encumbrances) Are Calculated by the System • Future salary • As entered in PeopleSoft, allocated based upon Labor Distribution Schedule entered in Oracle • Future student-related expenses • As entered in GFS, PeopleSoft Financial Aid or Student Financial modules • Approved Requisitions and Purchase Orders • As entered in Oracle iProcurement • Related burdens • Fringe benefits, indirect costs, etc. • Source code on report for all commitment transactions will start with “E” (for encumbrance)

Hard Commitments Will NOT Include: • Wage estimates for employees paid hourly (includes bargaining unit) • Additional recurring pay (SUP, HAP, etc.) • Credits for future vacations • iOU • PCard • iJournals • Feeder journals (inter-departmental charges)

Suppressing Hard Commitments • User has the ability to suppress (remove commitments) by PO line using Web Inquiry • Suppressing removes the commitment from expenditure reports only • If an invoice for this PO subsequently comes in, it will be paid

Correcting Hard Commitments on Approved Purchase Orders • Launch the Requisition and Purchase Order Query • https://ofweb.stanford.edu • View your purchase order commitments • Click the suppress box next to the line(s) of the commitment you want to suppress IMPORTANT: The suppress action is NOT reversible!

Salary Commitment Adjustments • Salary commitments are automatically adjusted when changes are made in Labor Distribution • Examples • Terminations • New hires • Percentages of effort

Step 4 Correct Inaccuracies • Once an inaccuracy is discovered, corrective action must be taken as soon as possible. • If an expenditure is incorrectly charged, the approver should initiate a correcting journal entry. • The reconciler should verify that the correcting journal entry has posted.

How to Correct Inaccuracies (non-salary) • Correct in system where error occurred (e.g., GFS or AP) • Use iJournal for corrections of iJournal errors • Policy: See AGM 38 Cost Transfers • Checklist for cost transfers Checklist for Cost Transfers

Fixing Recurring Transactions • Change coding errors in originating system for recurring transactions • For an approved PO http://www.stanford.edu/services/oracle/purchasing/training.html • For capital equipment, contact your Department Property Administrator (DPA)

Transactions Involving Capital Expenditure Codes – Purchase Data • Use PTAE Equipment Change Template • to change expenditure type • to change PTA used for purchase • http://ora.stanford.edu/ora/pmo/dpa_resources/reconciliation.asp • If caught BEFORE any payments are made, send request to • changemypta@lists.stanford.edu • Procurement Office will change the PO to reflect new PTA data PTAE Equipment Change Template

What Do Corrections Look Like? iJournal transactions appear on expenditure reports after approval You don’t have to wait until next month-end to confirm the correction. New data is available throughout the month.

Correct Errors as Soon as Identified • Reconcile and review within 2 months of the last day of the month being reviewed • Complete expense transfers within 2 months of end of the academic quarter Although report data is available throughout the month to answer questions, best practice is to wait to reconcile until after month end close.

Step 5 Initial, Date, and Retain Reports • Initial and date the reports to document that a reconciliation was performed.