Download

1 / 72

720 likes | 746 Views

IT Audit. M.C. Juan Carlos Olivares Rojas. MSN: juancarlosolivares@hotmail.com jcolivar@itmorelia.edu.mx http://antares.itmorelia.edu.mx/~jcolivar/ @jcolivares Social Network: Facebook, LinkedIn. Hi5. Information Audit Concepts.

E N D

IT Audit M.C. Juan Carlos Olivares Rojas MSN: juancarlosolivares@hotmail.com jcolivar@itmorelia.edu.mx http://antares.itmorelia.edu.mx/~jcolivar/ @jcolivares Social Network: Facebook, LinkedIn. Hi5

Information Audit Concepts • There area lot of definition about what Audit and Information Audit means. • Activity: in pairs try to discuss what’s the diference among Audit, Consult and Advisory. • Audit is an evaluation of a person, organization, system, process, project or product.

Audit • Audits are performed to ascertain the validity and reliability of information, and also provide an assessment of a system's internal control. • The goal of an audit is to express an opinion on the person/organization/system etc. under evaluation based on work done on a test basis. • Information Audit is “review the existing system of information management, identify problems and recommend solutions for those problems” (Elis 1993)

Information Audit • Other definition of Information audit is “an analysis of the communications (processes and information) that take place between agents (people) in a social context (the organisation) using a variety of media and channels (technology).” • Information Audit (IA) is focused in describe how things are done instead of existence; for example, use of a database rather than exist a database.

Information Audit • The IA contex have to set against organizational goals and costraints. • The IA has to try to solve question such as: • What is the purpose of the audited system? • Does it accomplish its purpose? • Is the purpose in line with the purpose and philosophy of the organisation as a whole?

Information Audit • How effectively are resources used? • How are resources accounted for and safeguarded? • How useful is the information system supporting the organisation? • How reliable is the information system? • Does the system comply with regulations and standards?

In Sum… • The goal of the Audit project • Compare what is, • To what should be • To bring the two together • The process is: • Establish what should be • Get support • Find out what is • Create results and recommendations.

Types of Auditing • Exist diferent clasification of Auditing. • By deep Level: General and Technical • General Auditing includes an assesment of diferent areas (i.e., financial, administrative, quality, etc.) in a company at the same time. • Technical Audits are specific such as Information System Audit.

Internal and External Audits • Internal Audits are realized by Individual of the Organization. The advantages are most knowledge of Internal Control and less time in the audit process. The disadvantages can be non-Ethical Reports. • External Audit or Superior Control Audit is realized by Third-People. This is recommended type of audit because is most Ethical and Efficient but required more time.

Field of Information Audit • What are Business Process? • It’s a collection of related, structured activities or tasks that produce a specific service or product (serve a particular goal) for a particular customer or customers. • Activity: Indicate what are the Business Process in a University such as Instituto Tecnologico de Morelia

Business Process • Some Business Process are very similar. • What’s the diference? • It’s the business rules. These are statements that define or constrain some aspect of the business • Activity: Describe the rules of some sport or game such as Soccer, Tenis, Tetris, etc.

What is Audited? • The Information that leads to knowledge • Resources for making information • How info is used • The people who need and create info • Info capture, management and presentation tools • How info is valued

What’s the Point? • Understand information • What is it? • How does it move? • Manage information • What should we spend on it? • How should it flow? • Give information its rightful place as something we pay attention to. • Money • Material goods • Processes

Internal Control • It’s defined as a process effected by an organization's structure, work and authority flows, people and management information systems, designed to help the organization accomplish specific goals or objectives. • It is a means by which an organization's resources are directed, monitored, and measured.

Internal Control • It plays an important role in preventing and detecting fraud and protecting the organization's resources, both physical (e.g., machinery and property) and intangible (e.g., reputation or intellectual property such as trademarks). • Internal control is a key element of the Foreign Corrupt Practices Act (FCPA) of 1977 and the Sarbanes-Oxley Act of 2002, which required improvements in internal control in United States public corporations.

Internal Control • The governance is a very important activity inside organizations because drive and direct the Internal Control. • Procurement plays and importan role in the modern organization because need mechanism to regularize the practices and maintance the justice. • External Control is supported by Goverment Legislation.

Control Models using in Info Audit • Discussion About Methodologies: • ISACA (Information System Audit and Control Association) • COBIT (Common OBjectives for Information and related Technologies) • ITIL (Information Technologies Infraestructure Library)

Other Methodologies • COSO • ISO/IEC 17799:2000 • ISO/IEC 13335 • ISO/IEC 15408 • TickIT • NIST 800-14

An Audit Project • What are the goals of the project? • What is the overall process? • What are the deliverables? • What does the plan look like?

What Are The Goals? • To assess what information and flow the org needs • To assess what information and flow the org now has • To make recommendations about how to get the two to match

What’s the Overall Process? 1. Analyze objectives for ideal process 2,3 Get a mandate and support 4 Plan the audit 5 Perform the audit 6,7 Interpret and Present the results 8,9 Take action 10 Repeat

Deliverables: A Goals-Knowledge-Info Taxonomy • Organizational objective 1 • Knowledge requirement 1.1 • Info that supports requirement • Containers for the information • People who need to know it • Flow • Creation • Use • Disposal • Knowledge requirement 1.2 • Organizational objective 2

Deliverables: Guardian and Stakeholder Profiles Who will you approach in the org and how? • What: Word files, a spreadsheet or Db records • Who are they? • How will you approach them? • What do you know without asking? • How: • Asking around • Quick email or other communication • Org charts or readiness results

Deliverables: Audit Methods What are the available methods ? • Analysis of docs and Dbs • Observation • Trying yourself • Interviews • Meetings • Surveys • Mapping

Deliverables: Audit Methods How will you assess the information resources of your organization? • What: Word, spreadsheet or Db • Analysis, resource, method • Date, time, and staff • How • Try each method • Discuss with guardians and stakeholders • Design for change

Deliverables: Staging Plan In what order should groups and information resources be done? • What: Word Doc, spreadsheet or DB • Groups and sources identified • Dates, times and staff for each • How • Arranged by • Strategic importance and potential for a win • Amount of support and ease or simplicity • Fair representation of all information

Deliverables: Information Analyses The assessment of each dimension of the organization's information. • What? Word, spreadsheet or Db • Data collected • Standard set of • Information Resources • How • Apply methods and plan • Collect data, analyze and revisit if needed

Deliverables: Reports and Presentations What are the analysis methods available? • Side-by-side comparison • SWOT • CATWOE • Clients • Actors • Transformations • Ownership • Environment

Deliverables: Reports and Presentations The official results of the audit • What • Word files, Slide decks • Email messages, meeting agendas • How • Lots of trial inside the team • Test results to supporters • Trial presentations to insiders • Multiple methods to communicate

Deliverables: Follow-Up Plan What should the org do and how will its success be measured? • What • Word file, project plan • Action • Preliminary scope, schedule, and budget • How • Work with appropriate guardians and execs • Focus on highest return projects first • Give lots of leeway to the formation of the exact solution • Caveat the heck out of your estimates

The Team • Audit manager • Understands the org’s business • Ability to listen • Respected • Auditors • Technology analysts • Interviewers • SME (Subject Matter Experts) • Tool designers • Survey construction • Data analysis and presentation techniques • Consultants • Specialist support in the background

Other IA Methodology • Initial review and evaluation of the area to be audited, and the audit plan preparation • Detailed review and evaluation of controls • Compliance testing • Analysis and reporting of results

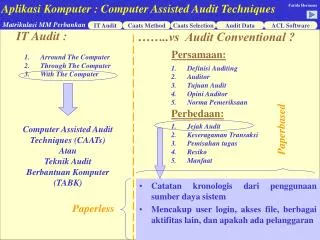

Review of System Documentation • The auditor reviews documentation such as narrative descriptions, flowcharts, and program listings. In desk checking the auditor processes test or real data through the program logic. • Audit throug the Computer: the process of reviewing and evaluating the internal controls in an electronic data processing system.

Audit with The Computer • The utilization of the computer by an auditor to perform some audit work that would otherwise have to be done manually.

Test • Test Data: The auditor prepares input containing both valid and invalid data. Prior to processing the test data, the input is manually processed to determine what the output should look like. The auditor then compares the computer-processed output with the manually processed results.

Test Data Computer Operations Auditors Prepare Test Transactions And Results Transaction Test Data Computer Application System Manually Processed Results Computer Output Auditor Compares

Types of Testing • Compliance Testing: Auditors perform tests of controls to determine that the control policies, practices, and procedures established by management are functioning as planned. This is known as compliance testing. • Substantive testing is the direct verification of financial statement figures. Examples would include reconciling a bank account and confirming accounts receivable.

Parallel Simulation • The test data process data through real programs. With parallel simulation, the auditor processes real client data on an audit program similar to some aspect of the client’s program. The auditor compares the results of this processing with the results of the processing done by the client’s program.

Parallel Simulation Computer Operations Auditors Actual Transactions Computer Application System Auditor’s Simulation Program Auditor Compares Actual Client Report Auditor Simulation Report

Audit Software • Computer programs that permit computers to be used as auditing tools include: • Generalized audit software (CAATS –Computer Assistant Audit Tools and Techniques) • P.C. Software (support)

Records • Extended Records: Specific transactions are tagged, and the intervening processing steps that normally would not be saved are added to the extended record, permitting the audit trail to be reconstructed for these transactions • Snapshot: A snapshot is similar to an extended record except that the snapshot is a printed audit trail

Principles Applied to Info Auditors • The Auditor word comes of the greek auditorium which means “listend” • Auditor was a person who main fuction was listening problems of people in a town and tacke back the Taxes and represent the intereses of Imperial Country.

Auditors Responsabilities • Support the implementation of, and encourage compliance with, appropriate standards, procedures and controls for information systems. • Perform their duties with objectivity, due diligence and professional care, in accordance with professional standards.

Preliminar and Detailed Review • In this Phase we works with documents information systems and other resources. • Preliminar Review is fast and acts as a filter. Detailed Review is important because we assurance the process.

Exam and Evaluation of Information • The most important thing in a organization is asset, frecuently information assets. • What are the principal assets in a Telecomunication Firm such as AT&T, Telmex, etc.? • Cupper in 1976 60% • Cupper, Fiber and Infraestructure 30% aprox. in 2008

Exam and Evaluation of Information • Where are the rest of the money? • Information System • What is the most important thing in Coca-Cola? • The Secret Formula. It’s the same since 1886, only 3 pesons in the world know it. • This formula is patented like a comercial secret

Test of User Control’s • What’s a User Control? • It’s a control which applied to final user or employees. • This process is important because a lot of firms are interesting in their relations with theirs user, employees, providers and third-parts. • In Programming the User Controls are the User Interface (UI). Remember for a end user, the UI is the system.

Substantive Test • Substantive testing is the stage of an audit when the auditor gathers evidence as to the extent of misstatements in client's accounting records. • This evidence is referred to as substantive evidence and is an important factor in determining the auditor's opinion on the financial statements as a whole.