Download

1 / 216

2.16k likes | 2.23k Views

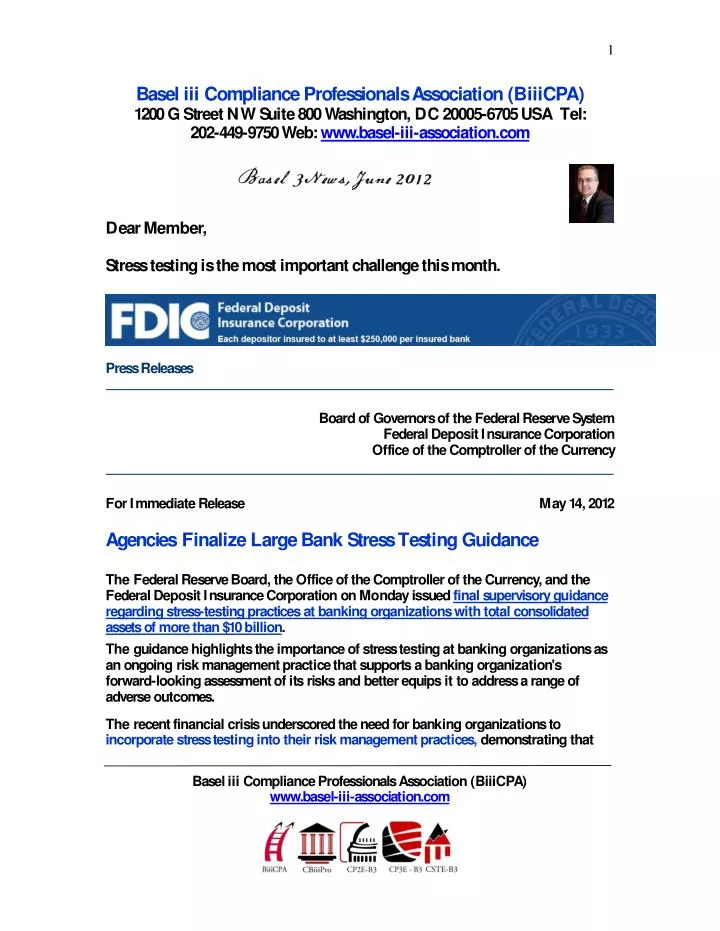

1 Bas e l iii C om p l i a n c e Pr o fe s s iona l s Ass o c i a t i on ( B ii i CPA) 1200 G St r e et N W S u it e 8 0 0 Wa s h i n g t o n , D C 2000 5 - 6705 U S A T el: 20 2 - 449 - 9 750 W e b : w w w.ba s e l - iii - a s soc i a t i o n . com. D ear Mem b er,

E N D

1 BaseliiiComplianceProfessionalsAssociation(BiiiCPA)1200GStreetNWSuite800Washington,DC20005-6705USATel:202-449-9750Web:www.basel-iii-association.com DearMember, Stresstestingisthemostimportantchallengethismonth. PressReleases BoardofGovernorsoftheFederalReserveSystemFederalDepositInsuranceCorporationOfficeoftheComptrolleroftheCurrency ForImmediateReleaseMay14,2012 AgenciesFinalizeLargeBankStressTestingGuidance TheFederalReserveBoard,theOfficeoftheComptrolleroftheCurrency,andtheFederalDepositInsuranceCorporationonMondayissuedfinalsupervisoryguidanceregardingstress-testingpracticesatbankingorganizationswithtotalconsolidatedassetsofmorethan$10billion. Theguidancehighlightstheimportanceofstresstestingatbankingorganizationsasanongoingriskmanagementpracticethatsupportsabankingorganization's forward-lookingassessmentofitsrisksandbetterequipsittoaddressarangeofadverseoutcomes. Therecentfinancialcrisisunderscoredtheneedforbankingorganizationsto incorporatestresstestingintotheirriskmanagementpractices,demonstratingthat BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

2 bankingorganizationsunpreparedforparticularlyadverseeventsandcircumstancescansufferacutethreatstotheirfinancialconditionandviability. Thisguidancebuildsuponpreviouslyissuedsupervisoryguidancethatdiscussestheusesandmeritsofstresstestinginspecificareasofriskmanagement. Theguidanceoutlinesgeneralprinciplesforasatisfactorystresstestingframeworkanddescribesvariousstresstestingapproachesandhowstresstestingshouldbeusedatvariouslevelswithinanorganization. Theguidancealsodiscussestheimportanceofstresstestingincapitalandliquidityplanningandtheimportanceofstronginternalgovernanceandcontrolsaspartofaneffectivestress-testingframework. TheguidancedoesnotimplementthestresstestingrequirementsintheDodd-FrankWallStreetReformandConsumerProtectionAct(Dodd-FrankAct)orintheFederalReserveBoard'scapitalplanrulethatapplytocertaincompanies,asthoserequirementshavebeenorarebeingimplementedthroughseparateproposalsbytherespectiveagencies. However,theagenciesexpectthatbankingorganizationswithtotalconsolidatedassetsofmorethan$10billionwouldfollowtheprinciplessetforthintheguidance--aswellasotherrelevantsupervisoryguidance--whenconductingstresstestinginaccordancewiththeDodd-FrankAct,thecapitalplanrule,andotherstatutoryorregulatoryrequirements. DEPARTMENTOFTHETREASURY OfficeoftheComptrolleroftheCurrencyFEDERALRESERVESYSTEM FEDERALDEPOSITINSURANCECORPORATION SupervisoryGuidanceonStressTestingforBankingOrganizationswithMoreThan$10BillionInTotalConsolidatedAssets AGENCIES:BoardofGovernorsoftheFederalReserveSystem(“Board”or“FederalReserve”);FederalDepositInsuranceCorporation(“FDIC”);OfficeoftheComptrolleroftheCurrency,Treasury(“OCC”). BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

3 ACTION:Finalsupervisoryguidance. SUMMARY:TheBoard,FDICandOCC,(collectively,the“agencies”)areissuingthisguidance,whichoutlineshigh-levelprinciplesforstresstestingpractices,applicabletoallFederalReserve-supervised,FDIC-supervised,andOCC-supervisedbankingorganizationswithmorethan$10billionintotalconsolidatedassets. Theguidancehighlightstheimportanceofstresstestingasanongoingriskmanagementpracticethatsupportsabankingorganization’sforward-lookingassessmentofitsrisksandbetterequipstheorganizationtoaddressarangeofadverseoutcomes. DATES:ThisguidancewillbecomeeffectiveonJuly23,2012. I.Background OnJune15,2011,theagenciesrequestedpubliccommentonjointproposedguidanceontheuseofstresstestingasanongoingriskmanagementpracticebybankingorganizationswithmorethan$10billionintotalconsolidatedassets(theproposedguidance). ThepubliccommentperiodontheproposedguidanceclosedonJuly29,2011. Theagenciesareadoptingtheguidanceinfinalformwithcertainmodificationsthatarediscussedbelow(thefinalguidance). Asdescribedbelow,thisguidancedoesnotapplytobankingorganizationswithconsolidatedassetsof$10billionorless. Allbankingorganizationsshouldhavethecapacitytounderstandtheirrisksandthepotentialimpactofstressfuleventsandcircumstancesontheirfinancialcondition. Theagencieshavepreviouslyhighlightedtheuseofstresstestingasameanstobetterunderstandtherangeofabankingorganization’spotentialriskexposures. The2007-2009financialcrisisfurtherunderscoredtheneedforbankingorganizationstoincorporatestresstestingintotheirriskmanagement,asbankingorganizationsunpreparedforstressfuleventsandcircumstancescansufferacutethreatstotheirfinancialconditionandviability. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

4 Thefinalguidanceisintendedtobeconsistentwithsoundindustrypracticesandwithinternationalsupervisorystandards. Buildinguponpreviouslyissuedsupervisoryguidancethatdiscussestheusesandmeritsofstresstestinginspecificareasofriskmanagement,thefinalguidanceprovidesprinciplesthatabankingorganizationshouldfollowwhenconductingitsstresstestingactivities. Theguidanceoutlinesbroadprinciplesforasatisfactorystresstesting frameworkanddescribesthemannerinwhichstresstestingshouldbeemployedasanintegralcomponentofriskmanagementthatisapplicableatvariouslevelsof aggregationwithinabankingorganizationandthatcontributestocapitalandliquidityplanning. Whiletheguidanceisnotintendedtoprovidedetailedinstructionsforconductingstresstestingforanyparticularriskorbusinessarea,theguidancedescribesseveral typesofstresstestingactivitiesandhowtheymaybemostappropriatelyusedbybankingorganizationssubjecttothisguidance. ThefinalguidancedoesnotimplementthestresstestingrequirementsimposedbytheDodd-FrankWallStreetReformandConsumerProtectionAct(Dodd-FrankAct)onfinancialcompaniesregulatedbytheOCC,FDIC,orBoardwithtotalconsolidatedassetsofmorethan$10billionorbytheBoard’scapitalplanruleonU.S.bankholding companieswithtotalconsolidatedassetsequaltoorgreaterthan$50billion. TheDodd-FrankAct’sstresstestingrequirementsarebeingimplementedthrough separatenoticesofproposedrulemakingbytherespectiveagencies. TheBoardissuedthefinalcapitalplanruleonNovember22,2011. Inlightoftheserecentrulemakingeffortsonstresstesting,theguidanceprovidesbankingorganizationswithprinciplesforconductingtheirstresstestingactivitiesto, amongotherthings,ensurethatthoseactivitiesareadequatelyintegratedintooverallriskmanagement. Theagenciesexpectsuchcompanieswouldfollowtheprinciplessetforthintheguidance–aswellasotherrelevantsupervisoryguidance–whenconductingstresstestinginaccordancewithstatutoryorregulatoryrequirements. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

5 • II.DiscussionofCommentsontheProposedGuidance • Theagenciesreceived17commentlettersontheproposedguidance. • Commentersincludedfinancialtradeassociations,bankholdingcompanies,financialadvisoryfirms,andindividuals.Commentersgenerallyexpressedsupportfortheproposedguidance. • However,severalcommentersrecommendedchangesto,orclarificationof,certainprovisionsoftheproposedguidance,asdiscussedbelow. • Inresponsetothesecomments,theagencieshaveclarifiedtheprinciplessetforthintheguidanceandmodifiedtheproposedguidanceincertainrespectsasdescribedinthissection. • Scopeofapplication • Theproposedguidancewouldhaveappliedtoallbankingorganizationssupervisedbytheagencieswithmorethan$10billionintotalconsolidatedassets. • Specifically, • withrespecttotheOCC,thesebankingorganizationswouldhaveincludednationalbankingassociationsandfederalbranchesandagencies; • withrespecttotheBoard,thesebankingorganizationswouldhaveincludedstatememberbanks,bankholdingcompanies,andallotherinstitutionsforwhichtheBoardistheprimaryfederalsupervisor; • withrespecttotheFDIC,thesebankingorganizationswouldhaveincludedstatenonmemberbanksandallotherinstitutionsforwhichtheFDICistheprimaryfederalsupervisor. • Theproposedguidanceindicatedthatabankingorganizationshould • developandimplementitsstresstestingframeworkinamannercommensuratewithitssize,complexity,businessactivities,andoverallriskprofile. • Somecommenterssupportedthetotalconsolidatedassetthreshold(i.e.,morethan • $10billion),butothersnotedtheimportanceandvalueofstresstestingforsmallerbankingorganizations. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

6 Consistentwiththeproposedguidance,nosupervisedbankingorganizationwith$10billionorlessintotalconsolidatedassetsissubjecttothisfinalguidance. Theagenciesbelievethat$10billionistheappropriatethresholdfortheguidance basedonthegeneralcomplexityoffirmsabovethissize. However,theagenciesnotethatpreviouslyissuedsupervisoryguidanceapplicabletoallsupervisedinstitutionsdiscussestheuseofstresstestingasatoolincertainaspectsofriskmanagement—suchasforcommercialrealestateconcentrations,liquidityriskmanagement,andinterest-rateriskmanagement. Theagenciesreceivedtwocommentssuggestingthatthe$10billiontotalconsolidatedassetthresholdbemeasuredoverafourquarterperiodinordertominimizethelikelihoodthattemporaryassetfluctuationswouldtriggerapplicationoftheguidance. Theagenciesdonotestablishanassetcalculationmethodologyinthefinalguidance;however,bankingorganizationswithassetsnearthethresholdshouldusereasonablejudgmentandconsider,inconjunctionwiththeirprimaryfederalsupervisorasappropriate,whethertheyshouldconsiderpreparingtofollowtheguidance. Threecommentersexpressedconcernthatforeignbankingorganizations(FBOs)arerequiredtofollowstresstestingguidelinesestablishedbytheirhomecountrysupervisorsandsuggestedthattheagenciesgiveconsiderationtothoserequirements. Whendevelopingtheguidance,theagenciessoughttoensurethatitwouldnot introduceinconsistencieswithinternationallyagreedsupervisorystandards. TheagenciesrecognizethatanFBO’sU.S.operationsarepartoftheFBO’sglobalenterprisesubjecttorequirementsofitshomecountry. Theagenciesprovidedsufficientflexibilityintheproposedguidancesothattheguidancecouldapplytovarioustypesoforganizations. Inthisfinalguidance,theagenciesclarifythatcertainaspectsoftheguidancemaynotapplytoU.S.branchesandagenciesofFBOs(suchastheportionsrelatedtocapitalstresstesting)ormayapplydifferently(suchasportionsrelatedtogovernanceandcontrols). Supervisorswilltaketheseissuesintoconsiderationwhenevaluatingtheabilityof U.S.officesofFBOstomeettheprinciplesintheguidance. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

7 Twocommentersexpressedconcernregardingtheapplicationoftheproposedguidancetosavingsandloanholdingcompanies(SLHCs). TheysuggestedthattheBoardissueseparateguidanceforSLHCs,astheseinstitutionswouldfaceadifferentsetofstresstestingassumptionsandscenariosthanbankingorganizations. TheBoardbelievesthattheguidanceisinstructivetoSLHCstothesamedegreeitisforbankholdingcompanies. TheFederalReservebecametheprimaryfederalsupervisorforSLHCsonJuly21,2011,aftertheagenciespublishedtheproposedguidanceforpubliccommentbutbeforetheendofthecommentperiod. WhiletheBoardrecognizesthatcertaindifferencesdoexistbetweenbankholdingcompaniesandSLHCs,theBoardbelievestheguidancecontainsflexibilityadequatetoaccommodatethevariationsinsize,complexity,businessactivities,andoverallriskprofileofallbankingorganizationsthatmeettheassetthreshold. Thus,theguidanceanticipatesthateachbankingorganization,includingeachSLHC,wouldimplementstresstestinginamannerconsistentwithitsownbusinessandriskprofile. Similarly,onecommenteradvocatedthattheOCCproposeseparateguidanceonstresstestingspecificallytailoredtosavingsassociations. TheOCCbecametheprimaryfederalsupervisorforfederalsavingsassociationsonJuly21,2011. WhiletheOCCrecognizesthatcertaindifferencesdoexistbetweennationalbanksandfederalsavingsassociations,theOCCnotesthatthefinalguidancecontainsflexibilityadequatetoaccommodatethevariationsinsize,complexity,businessactivities,andoverallriskprofileofallbankingorganizationsthatmeettheassetthreshold. Thus,itisalsoexpectedthateachfederalsavingsassociationwouldimplementtheguidanceconsistentwithitsownbusinessandriskprofile. SeveralcommentersrequestedclarificationonthelinkagebetweenthestresstestingguidanceandthestresstestingrequirementsintheDodd-FrankAct. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

8 Indevisingtheguidance,theagenciesendeavoredtoensurethattheproposedandfinalguidanceisconsistentwiththestresstestingrequirementsunderthe Dodd-FrankActandbelievethattheprinciplessetforthinthefinalguidanceare usefulwhenconductingthestresstestsrequiredundertheAct. Notably,thefinalguidancewasframedbroadlytoinformabankingorganization’suseofstresstestinginoverallriskmanagement,notjuststresstestsrequiredundertheDodd-FrankAct. Dodd-Frankstresstestswouldgenerallybeconsideredpartofanorganization’soverallstresstestingframeworkasdescribedinthe stresstestingguidance. B.StressTestingPrinciples Asnotedabove,theproposedguidanceidentifiedandincludedadiscussionoffourkeyprinciplesforabankingorganization’sstresstestingframeworkandrelatedstresstestresults,namelythat: Abankingorganization’sstresstestingframeworkshouldincludeactivitiesandexercisesthataretailoredtoandsufficientlycapturethebankingorganization’sexposures,activities,andrisks; Aneffectivestresstestingframeworkemploysmultipleconceptuallysoundstresstestingactivitiesandapproaches; Aneffectivestresstestingframeworkisforward-lookingandflexible;and Stresstestresultsshouldbeclear,actionable,wellsupported,andinformdecision-making. Inthefinalguidance,theagencieshaveincorporatedafifthprinciplespecifyingthatanorganization’sstresstestingframeworkshouldincludestronggovernanceandeffectiveinternalcontrols. TheelementsofthefifthprinciplehadbeensetforthinsectionVIoftheproposedguidance,andthefifthprincipledoesnotexpandonthisaspectoftheproposedguidance. Rather,theagenciesreorganizedthisdiscussionintoafifthprinciple BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

9 inordertounderscoretheimportanceofgovernanceandcontrolsasakeyelementinabankingorganization’sstresstestingframework. Asnotedabove,commentersweresupportiveoftheprinciples-basedapproachandthenotionthatabankingorganization’sstresstestingframeworkshouldbeimplementedinamannercommensuratewithfactorssuchasthecomplexityandsizeoftheorganization. Withmorespecificregardtotheproposedprinciples,commenterssuggestedthatthefinalguidanceaddressthestandardizationofstresstestingthroughtheinclusionofcommoncoefficients,models,orbenchmarks. Thesecommentersexpressedconcernsthatbankingorganizationswouldimplementtheprinciplesinconsistentlyandthatstandardizationwouldhelpregulatorsconductcomparativeanalysesacrossfirms. Anothercommentersuggestedthattheagenciesprescribemoredetailedandintegratedstresstestingbetweendifferententitiesorbusinessunitswithinanorganization. Theagenciesdidnotmodifytheguidanceinresponsetothesecomments. Akeyaspectoftheguidanceistoprovideorganizationsflexibilityonhowtheydesigntheirindividualstresstestingframeworks. Thus,eachbankingorganizationshoulddesignaspecificstresstestingframeworktocapturerisksrelevanttotheorganization. Theagenciesbelievethatprescribingstandardizedstresstestsinthisguidancewouldhaveitsowninherentlimitationsandmaynotappropriatelycoverabankingorganization’smaterialrisksandactivities. Inaddition,commenterssuggestedthattheagenciesmandatepublicreleaseofstresstestingresultsthroughtheguidance. Theagencieshaveconsideredthesecomments,butdonotbelievethefinalguidanceistheappropriateplaceforsucharequirementgivenitsbroaderfocusonbankingorganizations’overallstresstestingframeworks. Theagenciesnote,however,thatbankingorganizationsmayberequiredtodiscloseinformationabouttheirstresstestspursuanttootherstatutory,regulatory,orsupervisoryrequirements. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

10 Afewcommentersstatedthatabankingorganizationshouldexplainandjustifythestresstestingmethodologiesitutilizestoitsprimaryfederalsupervisor. Theagenciesnotethatsupervisorswillexaminefirms’stresstestingmethodologiesthroughthesupervisoryprocess. Onecommenternotedthattheguidanceshouldexplicitlyindicatethatliabilitiesshouldbepartofabankingorganization’sstresstestingactivities;theagenciesintendedthatstresstestingactivitieswouldtakeanorganization’sliabilitiesintoaccountandhaveclarifiedthisinthefinalguidance. Threecommenterssuggestedthatoperationalriskbespecificallyreferencedintheguidance. Inresponse,theagencieshaveclarifiedinthefinalguidancethatoperationalrisk shouldbeamongtherisksconsideredbyanorganization’sstresstestingframework. Anothercommenterexpressedconcernthatthefrequencyofstresstestingand communicationofresultsmighteventuallydesensitizeseniormanagementtothem. Theagenciesbelievethatregularreviewofstresstestresultsisuseful–bothduringperiodsofeconomicdownturnandbenignperiods–andhaveclarifiedthatsuchreviewcanhelpabankingorganizationtrackovertimetheimpactofongoingbusinessactivities,changesinexposures,varyingeconomicconditions,andmarketmovementsonitsfinancial condition. Asidefromtheinclusionofafifthprincipleasdescribedabove,theagencieshaveotherwiseadoptedtheproposedprinciplesinthefinalguidancewithonlyminoradditionalrefinements. C.Stresstestingapproachesandapplications Theproposedguidancedescribedcertainstresstestingapproachesand applications–scenarioanalysis,sensitivityanalysis,enterprise-widetesting,andreversestresstesting–thatabankingorganizationcouldconsiderusingwithinitsstresstestingframework,asappropriate. Theproposedguidanceprovidedthateachbankingorganizationshouldapplytheseapproachesandapplicationscommensuratewithitssize,complexity,andbusinessprofile,andmaynotneedtoincorporateallofthedetailsdescribedintheguidance. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

11 Somecommentersquestionedtheappropriatenumberandtypesofstresstestapproachesanorganizationshouldutilize. Theagenciesdonotbelievethatspecifyinganumberorparticulartypesofapproaches–includingthenumberofscenarios–isappropriateintheguidancegiventhewiderangeofstresstestingactivitiesthatdifferentbankingorganizationsmayundertake. Abankingorganizationshouldchoosetheapproachesthatappropriatelyconsidertheuniquecharacteristicsofthatparticularorganizationandtherelevantrisksitfaces. Theagenciesexpectthatstresstestingmethodologieswillevolveovertimeasbankingorganizationsdevelopapproachesthatbestcapturetheirindividualriskprofiles. Inaddition,theproposedguidancedescribedreversestresstestingasatoolthat wouldallowabankingorganizationtoassumeaknownadverseoutcome,suchassufferingacreditlossthatcausesittobreachaminimumregulatorycapitalratioorsufferingsevereliquidityconstraintsmakingitunabletomeetitsobligations,andthendeducethetypesofeventsthatcouldleadtosuchanoutcome. Thistypeofstresstestingmayhelpabankingorganizationtoconsiderscenariosbeyonditsnormalbusinessexpectationsandseetheimpactofseveresystemiceffectsonthebankingorganization. Italsowouldallowabankingorganizationtochallengecommonassumptionsaboutitsperformanceandexpectedmitigationstrategies. Threecommentersexpresseddoubtsregardingtheeffectivenessofreversestresstesting,astheapproachcouldproduceresultsofquestionablevalueandcapturesunlikely,“extreme”scenarios. Theagenciesreiteratethevalueofreversestresstesting,asithelpsabankingorganizationevaluatethecombinedeffectofseveraltypesofextremeeventsand circumstancesthatmightthreatenthesurvivalofthebankingorganization,evenifinisolationeachoftheeffectsmightbemanageable. Anothercommenterexpressedconcernthattheresultsofseverescenariosusedforreversestresstestingwoulddirectlyleadtoasupervisoryrequirementtoraisecapitaliftheresultsoftheapproachwereunfavorabletotheorganization. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

12 Inaddition,somecommenterssoughtclarificationthatresultswouldnotbeusedbyregulatorstocriticizebankingorganizations. Asstatedintheproposedguidance,agivenstresstestresultwillnotnecessarilyleadtoimmediateactionbyafirm,andinsomecasesstresstestresults–includingthosefromreversestresstests–aremostusefulfortheadditionalinformationtheyprovide. Intermsofsupervisoryresponsestoanorganization’sstresstestingactivities,theagenciesexpecttoconsiderabankingorganization’sstresstestresultsandtheappropriatenessofitsoverallstresstestingframework,alongwithallotherrelevantinformation,inassessingabankingorganization’sriskmanagementpractices,aswellasitscapitalandliquidityadequacy. Theguidancesetsforthsupervisoryexpectationsforprudentriskmanagementpracticesandafirm'sdecisionnottofollowtheprinciplesinthisguidancewillbeexaminedaspartofthesupervisoryprocessandmaybecitedasevidenceofunsafeandunsoundpractices. D.Stresstestingforassessingadequacyofcapitalandliquidity Giventheimportanceofcapitalandliquiditytoabankingorganization’sviability,stresstestingshouldbeappliedtothesetwoareasonaregularbasis. Stresstestingforcapitalandliquidityadequacyshouldbeconductedincoordinationwithabankingorganization’soverallbusinessstrategyandannualplanningcycles. Resultsshouldberefreshedintheeventofmajorstrategicdecisions,orotherchangesthatcanmateriallyimpactcapitalorliquidity. Aneffectivestresstestingframeworkshouldexplorethepotentialforcapitalandliquidityproblemstoariseatthesametimeorexacerbateoneanother. Abankingorganization’sliquiditystressanalysisshouldexploresituationsinwhichthebankingorganizationmaybeoperatingwithacapitalpositionthatexceedsregulatoryminimums,butisnonethelessviewedwithinthefinancialmarketsorbyitscounterpartiesasbeingofquestionableviability. Foritscapitalandliquiditystresstests,abankingorganizationshouldarticulateclearlyitsobjectivesforapost-stressoutcome,forinstancetoremainaviablefinancialmarketparticipantthatisabletomeetitsexistingandprospectiveobligationsandcommitments. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

13 Inresponsetocommentsreceivedontheplanninghorizonforstresstests,theagenciesclarifiedthatwhilecapitalstresstestsshouldgenerallybeconductedwithahorizonofatleasttwoyears,organizationsshouldrecognizethattheeffectsofcertainstressconditionscouldextendbeyondthathorizon. Theagencieshavealsoclarified,inresponsetocomments,thatconsolidatedstresstestsshouldaccountforthefactthatcertainlegalentitieswithintheconsolidatedorganizationarerequiredtomeetregulatorycapitalrequirements. Acommenterrequestedclarificationonwhethercapitalandliquiditystresstestingshouldbeevaluatedinunifiedorseparatestresstests. Theproposedguidancedidnotspecifytheprecisemannerinwhichcapitalandliquiditystresstestsshouldbeperformed. Thefinalguidancenotesthatassessingthepotentialinteractionofcapitalandliquiditycanbechallengingandmaynotbepossiblewithinasinglestresstest,soabankingorganizationshouldexploreseveralavenuestoassessthatinteraction. Inanycase,theagenciesbelievethatstresstestingforbothliquidityandcapitaladequacyshouldbeanintegralpartofabankingorganization’sstresstestingframework. E.Governanceandcontrols Asnotedunderthenewfifthprincipleofthefinalguidance,abankingorganization’sstresstestingframeworkwillbeeffectiveonlyifitissubjecttostronggovernanceandcontrolstoensurethattheframeworkfunctionsasintended. Stronggovernanceandcontrolsalsohelpensurethattheframeworkcontainscoreelements,fromclearlydefinedstresstestingobjectivestorecommendedactions. Importantly,stronggovernanceprovidescriticalreviewofelementsofthestresstestingframework,especiallyregardingkeyassumptions,uncertainties,andlimitations. Abankingorganizationshouldensurethatthestresstestingframeworkisnotisolatedwithinabankingorganization’sriskmanagementfunction,butisfirmlyintegratedintobusinesslines,capitalandasset-liabilitycommittees,andotherdecision-makingbodies. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

14 Aspartoftheiroverallresponsibilities,abankingorganization’sboardandseniormanagementshouldestablishacomprehensive,integratedandeffectivestresstesting frameworkthatfitsintothebroaderriskmanagementofthebankingorganization. Stresstestingresultsshouldbeusedtoinformtheboardaboutalignmentofthebankingorganization’sriskprofilewiththeboard’schosenriskappetite,aswellasinformoperatingandstrategicdecisions. Stresstestingresultsshouldbeconsidereddirectlybytheboardandseniormanagementfordecisionsrelatingtocapitalandliquidityadequacy. Seniormanagement,inconsultationwiththeboard,shouldensurethatthestresstestingframeworkincludesasufficientrangeofstresstestingactivitiesappliedattheappropriatelevelsofthebankingorganization(i.e.,notjustoneenterprise-widestresstest). Severalcommentersraisedconcernsregardingtheproposedresponsibilitiesofabankingorganization’sboardofdirectorswithrespecttostresstestsandtheframework. Onecommenterbelievedthattheboardofdirectorsshouldnotreviewallstresstestresults,butratheronlythosethatwereexpectedtohaveamaterialimpactontheoverallorganization. Anothercommenterexpressedthebeliefthattheboardofdirectorsshouldbeinvolvedinprovidingdirectionandoversightregardingthebankingorganization’sstresstestingframework,butthattheboardofdirectorsshouldnotbeexpectedtobe involveddirectlyinmoreoperationalaspectsoftheframework. Theagencieshavemodifiedthefinalguidancetoclarifythatseniormanagement,nottheboardofdirectors,shouldhavetheprimaryresponsibilityforstresstestingimplementationandtechnicaldesign. However,theagenciesemphasizethatabankingorganization’sboardofdirectorsshouldbeprovidedwithinformationfromseniormanagementonstresstesting developments(includingtheprocesstodesigntestsanddevelopscenarios)andonstresstestingresults(includingfromindividualtests,wherematerial). Asageneralmatter,theboardofdirectorsisalsoresponsibleformonitoringeffectivenessoftheoverallframework,andusingtheresultstoinformtheirdecisionmakingprocess. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

15 Inaddition,thefinalguidancespecifiesthatseniormanagementshould,inconsultationwiththeboardofdirectors,reviewstresstestingactivitiesandresultswithanappropriatelycriticaleyetoensurethatthereisobjectivereviewandthatthestresstestingframeworkincludesasufficientrangeofstresstestingactivitiesappliedattheappropriatelevelsofthebankingorganization. Finally,inresponsetocomments,theagencieshaveclarifiedthatabankingorganization’sminimumannualreviewandassessmentoftheeffectivenessoftheirstresstestingframeworkshouldensurethatstresstestingcoverageiscomprehensive,testsarerelevantandcurrent,methodologiesaresound,andresultsareproperlyconsidered. IV.AdministrativeLawMatters A.PaperworkReductionActAnalysis InaccordancewiththePaperworkReductionAct(“PRA”)of1995theagenciesreviewedthefinalguidance.Theagenciesmaynotconductorsponsor,andanorganizationisnotrequiredtorespondto,aninformationcollectionunlesstheinformationcollectiondisplaysacurrentlyvalidOMBcontrolnumber. Whiletheguidanceisnotbeingadoptedasarule,theagenciesdeterminedthatcertainaspectsoftheguidancemayconstituteacollectionofinformationand,therefore,believeditwashelpfultopublishaburdenestimatewiththeguidance. Inparticular,theaspectsoftheguidancethatmayconstituteaninformationcollectionaretheprovisionsthatstateabankingorganizationshould Haveastresstestingframeworkthatincludesclearlydefinedobjectives, well-designedscenariostailoredtothebankingorganization’sbusinessandrisks,well-documentedassumptions,conceptuallysoundmethodologiestoassesspotentialimpactonthebankingorganization’sfinancialcondition,informativemanagementreports,andrecommendedactionsbasedonstresstestresults;and Havepoliciesandproceduresforastresstestingframework. Theagenciesestimatedthattheabove-describedinformationcollectionsincludedintheguidancewouldtakerespondents,onaverage,260hourseachyear. Thefrequencyofinformationcollectionisestimatedtobeannual.Respondentsarebankingorganizationswithmorethan$10billionintotalconsolidatedassets,asdefinedintheguidance. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

16 Theagenciesreceivedthreecommentlettersregardingthepaperworkburdenoftheguidance,statingthatimplementationwillrequireamultipleofthe260estimatedhours. TheagenciesemphasizethattheguidancedoesnotimplementthestresstestingrequirementsimposedbytheDodd-FrankActortheBoard’scapitalplanrule,anddoesnototherwiseimposemandatorystresstestingrequirements. Theburdenofinformationcollectionsassociatedwithmandatorystresstestswillbe accountedforintherespectiverulesthatimplementthoserequirements. Inaddition,theagenciesbelievethatinsomerespects,theinformationcollection elementsofthisguidanceaugmentcertainexpectationsthatalreadyareinplacerelativetocertainexistingsupervisoryguidance. Theburdenestimatesforthisguidancetakeintoconsiderationonlythosecollectionsofinformation,suchasdocumentationofpoliciesandproceduresandrelevantreports,thatarespecifictothisguidance. Basedonthesefactors,theagenciesbelievetheburdenestimatesincludedintheproposedguidancecontinuetobeappropriate. V.Finalsupervisoryguidance Thetextofthefinalsupervisoryguidanceisasfollows: OfficeoftheComptrolleroftheCurrencyFederalReserveSystem FederalDepositInsuranceCorporation GuidanceonStressTestingforBankingOrganizationswithTotalConsolidatedAssetsofMoreThan$10Billion I.Introduction Allbankingorganizationsshouldhavethecapacitytounderstandfullytheirrisksandthepotentialimpactofstressfuleventsandcircumstancesontheirfinancialcondition. TheU.S.federalbankingagencieshavepreviouslyhighlightedtheuseofstresstestingasameanstobetterunderstandtherangeofabankingorganization’spotentialriskexposures. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

17 The2007-2009financialcrisisunderscoredtheneedforbankingorganizationsto incorporatestresstestingintotheirriskmanagementpractices,demonstratingthat bankingorganizationsunpreparedforstressfuleventsandcircumstancescansufferacutethreatstotheirfinancialconditionandviability. TheFederalReserve,theOfficeoftheComptrolleroftheCurrency,andtheFederalDepositInsuranceCorporation(collectively,the“agencies”)areissuingthisguidancetoemphasizetheimportanceofstresstestingasanongoingriskmanagementpracticethatsupportsbankingorganizations’forward-lookingassessmentofrisksandbetterequipsthemtoaddressarangeofadverseoutcomes. Thisjointguidanceisapplicabletoallinstitutionssupervisedbytheagencieswith morethan$10billionintotalconsolidatedassets. Specifically,withrespecttotheOCC,thesebankingorganizationsincludenationalbankingassociations,federalsavingsassociations,andfederalbranchesandagencies;withrespecttotheBoard,thesebankingorganizationsincludestatememberbanks,bankholdingcompanies,savingsandloanholdingcompanies,andallotherinstitutionsforwhichtheFederalReserveistheprimaryfederalsupervisor;withrespecttotheFDIC,thesebankingorganizationsincludestatenonmemberbanks,statesavingsassociationsandinsuredbranchesofforeignbanks. Theguidancedoesnotapplytoanysupervisedinstitutionbelowthedesignatedassetthreshold. Certainotherexistingsupervisoryguidancethatappliestoallsupervisedinstitutionsdiscussestheuseofstresstestingasatoolincertainaspectsofriskmanagement,suchasforcommercialrealestateconcentrations,liquidityriskmanagement,andinterest-rateriskmanagement. However,noinstitutionatorbelow$10billionintotalconsolidatedassetsissubjecttothisfinalguidance. Buildinguponpreviouslyissuedsupervisoryguidancethatdiscussestheusesandmeritsofstresstestinginspecificareasofriskmanagement,thisguidanceprovidesbroadprinciplesabankingorganizationshouldfollowinconductingitsstresstesting activities,suchasensuringthatthoseactivitiesfitintotheorganization’soverallriskmanagementprogram. Theguidanceoutlinesbroadprinciplesforasatisfactorystresstestingframeworkanddescribesthemannerinwhichstresstestingshouldbeemployedasanintegralcomponentofriskmanagementthatisapplicableatvariouslevelsofaggregation BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

18 withinabankingorganization,aswellasforcontributingtocapitalandliquidityplanning. Whiletheguidanceisnotintendedtoprovidedetailedinstructionsforconductingstresstestingforanyparticularriskorbusinessarea,thedocumentdescribesseveraltypesofstresstestingactivitiesandhowtheymaybemostappropriatelyusedbybankingorganizations. II.OverviewofStressTestingFramework Forpurposesofthisguidance,stresstestingreferstoexercisesusedtoconductaforwardlookingassessmentofthepotentialimpactofvariousadverseeventsandcircumstancesonabankingorganization. Stresstestingoccursatvariouslevelsofaggregation,includingonanenterprise-widebasis. AsoutlinedinsectionIV,thereareseveralapproachesandapplications forstresstestingandabankingorganizationshouldconsidertheuseofeachinitsstresstestingframework. Aneffectivestresstestingframeworkprovidesacomprehensive,integrated,andforwardlookingsetofactivitiesforabankingorganizationtoemployalongwithotherpracticesinordertoassistintheidentificationandmeasurementofitsmaterialrisksandvulnerabilities,includingthosethatmaymanifestthemselvesduringstressfuleconomicorfinancialenvironments,orarisefromfirm-specificadverseevents. Suchaframeworkshouldsupplementotherquantitativeriskmanagementpractices,suchasthosethatrelyprimarilyonstatisticalestimatesofriskorlossestimatesbasedonhistoricaldata,aswellasqualitativepractices. Inthismanner,stresstestingcanassistinhighlightingunidentifiedorunder-assessedriskconcentrationsandinterrelationshipsandtheirpotentialimpactonthebankingorganizationduringtimesofstress. Abankingorganizationshoulddevelopandimplementitsstresstestingframeworkinamannercommensuratewithitssize,complexity,businessactivities,andoverallriskprofile. Itsstresstestingframeworkshouldincludeclearlydefinedobjectives,well-designedscenariostailoredtothebankingorganization’sbusinessandrisks,well-documented BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

19 assumptions,soundmethodologiestoassesspotentialimpactonthebankingorganization’sfinancialcondition,informativemanagementreports,ongoingandeffectivereviewofstresstestingprocesses,andrecommendedactionsbasedonstresstestresults. Stresstestingshouldincorporatetheuseofhigh-qualitydataandappropriateassumptionsabouttheperformanceoftheinstitutionunderstresstoensurethatthe outputsarecredibleandcanbeusedtosupportdecision-making. Importantly,abankingorganizationshouldhaveasoundgovernanceandcontrolinfrastructurewithobjective,criticalreviewtoensurethestresstestingframeworkisfunctioningasintended. Astresstestingframeworkshouldallowabankingorganizationtoconductconsistent,repeatableexercisesthatfocusonitsmaterialexposures,activities,risks,andstrategies,andalsoconductadhocscenariosasneeded. Theframeworkshouldconsidertheimpactofbothfirmspecificandsystemicstresseventsandcircumstancesthatarebasedonhistoricalexperienceaswellasonhypotheticaloccurrencesthatcouldhaveanadverseimpactonabankingorganization’soperationsandfinancialcondition. Bankingorganizationssubjecttothisguidanceshoulddeveloppoliciesonreviewingandassessingtheeffectivenessoftheirstress testingframeworks,andusethosepoliciesatleastannuallytoassesstheeffectiveness oftheirframeworks. Suchassessmentsshouldhelptoensurethatstresstestingcoverageiscomprehensive,testsarerelevantandcurrent,methodologiesaresound,andresultsareproperlyconsidered. III.GeneralStressTestingPrinciples Abankingorganizationshoulddevelopandimplementaneffectivestresstesting frameworkaspartofitsbroaderriskmanagementandgovernanceprocesses. Theframeworkshouldincludeseveralactivitiesandexercises,andnotjustrelyonany singletestortypeoftest,sinceeverystresstesthaslimitationsandreliesoncertainassumptions. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

20 • Theusesofabankingorganization’sstresstestingframeworkshouldinclude,butarenotlimitedto, • augmentingriskidentificationandmeasurement; • estimatingbusinesslinerevenuesandlossesandinformingbusinesslinestrategies; • identifyingvulnerabilities,assessingthepotentialimpactfromthosevulnerabilities,andidentifyingappropriateactions; • assessingcapitaladequacyandenhancingcapitalplanning;assessingliquidityadequacyandinformingcontingencyfundingplans; • contributingtostrategicplanning; • enablingseniormanagementtobetterintegratestrategy,riskmanagement,and capitalandliquidityplanningdecisions;andassistingwithrecoveryandresolutionplanning. • Thissectiondescribesgeneralprinciplesthatabankingorganizationshouldapplyinimplementingsuchaframework. • Principle1: • Abankingorganization’sstresstestingframeworkshouldincludeactivitiesandexercisesthataretailoredtoandsufficientlycapturethebankingorganization’sexposures,activities,andrisks. • Aneffectivestresstestingframeworkcoversabankingorganization’sfullsetofmaterialexposures,activities,andrisks,whetheronoroffthebalancesheet,basedon effectiveenterprise-wideriskidentificationandassessment. • Risksaddressedinafirm’sstresstestingframeworkmayinclude(butarenotlimited to)credit,market,operational,interest-rate,liquidity,country,andstrategicrisk. • Theframeworkshouldalsoaddressnon-contractualsourcesofrisks,suchasthoserelatedtoabankingorganization’sreputation. • Appropriatecoverageisimportantasstresstestingresultscouldgiveafalsesenseofcomfortifcertainportfolios,exposures,liabilities,orbusinesslineactivitiesarenotincluded. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

21 Stresstestingexercisesshouldbepartofabankingorganization’sregularriskidentificationandmeasurementactivities. Forexample,inassessingcreditriskabankingorganizationshouldevaluatethepotentialimpactofadverseoutcomes,suchasaneconomicdownturnordecliningassetvalues,ontheconditionofitsborrowersandcounterparties,andonthevalueof anysupportingcollateral. Asanotherexample,inassessinginterest-raterisk,bankingorganizationsshouldanalyzetheeffectsofsignificantinterestrateshocksorotheryield-curvemovements.Aneffectivestresstestingframeworkshouldbeappliedatvariouslevelsinthebankingorganization,suchasbusinessline,portfolio,andrisktype,aswellasonan enterprise-widebasis. Inmanycases,stresstestingmaybemoreeffectiveatbusinesslineandportfolio levels,asahigherlevelofaggregationmaycloudorunderestimatethepotentialimpactofadverseoutcomesonabankingorganization’sfinancialcondition. Insomecases,stresstestingcanalsobeappliedtoindividualexposuresorinstruments. Eachstresstestshouldbetailoredtotherelevantlevelofaggregation,capturingcriticalriskdrivers,internalandexternalinfluences,andotherkeyconsiderationsattherelevantlevel. Stresstestingshouldcapturetheinterplayamongdifferentexposures,activities,andrisksandtheircombinedeffects. Whilestresstestingseveraltypesofrisksorbusinesslinessimultaneouslymayproveoperationallychallenging,abankingorganizationshouldaimtoidentifycommonriskdriversacrossrisktypesandbusinesslinesthatcanadverselyaffectitsfinancialcondition. Accordingly,stresstestsshouldprovideabankingorganizationwiththeabilitytoidentifypotentialconcentrations–includingthosethatmaynotbereadilyobservableduringbenignperiodsandwhosesensitivitytoacommonsetoffactorsisapparentonlyduringtimesofstress–andtoassesstheimpactofidentifiedconcentrationsofexposures,activities,andriskswithinandacrossportfoliosandbusinesslinesandontheorganizationasawhole. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

22 Stresstestingshouldbetailoredtothebankingorganization’sidiosyncrasiesandspecificbusinessmixandincludeallmajorbusinesslinesandsignificantindividualcounterparties. Forexample,abankingorganizationthatisgeographicallyconcentratedmaydeterminethatacertainsegmentofitsbusinessmaybemoreadverselyaffectedby shockstoeconomicactivityatthestateorlocallevelthanbyaseverenationalrecession. Ontheotherhand,ifthebankingorganizationhassignificantglobaloperations,itshouldconsiderscenariosthathaveaninternationalcomponentandstressconditionsthatcouldaffectthedifferentaspectsofitsoperationsindifferentways,aswellasconditionsthatcouldadverselyaffectallofitsoperationsatthesametime. Abankingorganizationshoulduseitsstresstestingframeworktodeterminewhetherexposures,activities,andrisksundernormalandstressedconditionsarealignedwiththebankingorganization’sriskappetite. Abankingorganizationcanusestresstestingtohelpinformdecisionsaboutitsstrategicdirectionand/orriskappetitebybetterunderstandingtherisksfromitsexposuresorofengagingincertainbusinesspractices. Forexample,ifabankingorganizationpursuesabusinessstrategyforanewormodifiedproduct,andthebankingorganizationdoesnothavelong-standingexperiencewiththatproductorlacksextensivedata, thebankingorganizationcanusestresstestingtoidentifytheproduct’spotentialdownsidesandunanticipatedrisks. Scenariosusedinabankingorganization’sstresstestsshouldberelevanttothedirectionandstrategysetbyitsboardofdirectors,aswellassufficientlyseveretobecredibletointernalandexternalstakeholders. Principle2: Aneffectivestresstestingframeworkemploysmultipleconceptuallysoundstresstestingactivitiesandapproaches. Allmeasuresofrisk,includingstresstests,haveanelementofuncertaintyduetoassumptions,limitations,andotherfactorsassociatedwithusingpastperformancemeasuresandforward-lookingestimates. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

23 Bankingorganizationsshould,therefore,usemultiplestresstestingactivitiesandapproaches(consistentwithsectionIV),andensurethateachisconceptuallysound. Stresstestsusuallyvaryindesignandcomplexity,includingthenumberoffactorsemployedandthedegreeofstressapplied. Abankingorganizationshouldensurethatthecomplexityofanygiventestdoesnotundermineitsintegrity,usefulness,orclarity. Insomecases,relativelysimpletestscanbeveryusefulandinformative.Additionally,effectivestresstestingreliesonhigh-qualityinputdataandinformation toproducecredibleoutcomes. Abankingorganizationshouldensurethatithasreadilyavailabledataandotherinformationforthetypesofstresstestsituses,includingkeyvariablesthatdriveperformance. Inaddition,abankingorganizationshouldhaveappropriatemanagementinformationsystems(MIS)anddataprocessesthatenableittocollect,sort,aggregate,andupdatedataandotherinformationefficientlyandreliablywithinbusinesslinesandacrossthebankingorganizationforuseinstresstesting. Ifcertaindataandinformationarenotcurrentornotavailable,orifproxiesareused,abankingorganizationshouldanalyzethestresstestoutputswithanunderstandingofthosedatalimitations. Abankingorganizationshouldalsodocumenttheassumptionsusedinitsstresstestsandnotethedegreeofuncertaintythatmaybeincorporatedintothetoolsusedforstresstesting. Insomecases,itmaybeappropriatetopresentandanalyzetestresultsnotjustintermsofpointestimates,butalsoincludingthepotentialmarginoferrororstatisticaluncertaintyaroundtheestimates. Furthermore,almostallstresstests,includingwell-developedquantitativetestssupportedbyhigh-qualitydata,employacertainamountofexpertorbusinessjudgment,andtheroleandimpactofsuchjudgmentshouldbeclearlydocumented. Insomecases,whencredibledataarelackingandmorequantitativetestsareoperationallychallengingorintheearlystagesofdevelopment,abanking BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

24 organizationmaychoosetoemploymorequalitativelybasedtests,providedthatthetestsareproperlydocumentedandtheirassumptionsaretransparent. Regardlessofthetypeofstresstestsused,abankingorganizationshouldunderstandandclearlydocumentallassumptions,uncertainties,andlimitations,andprovidethatinformationtousersofthestresstestingresults. Principle3: Aneffectivestresstestingframeworkisforward-lookingandflexible. Astresstestingframeworkshouldbesufficientlydynamicandflexibletoincorporatechangesinabankingorganization’son-andoff-balance-sheetactivities,portfoliocomposition,assetquality,operatingenvironment,businessstrategy,andotherrisksthatmayariseovertimefromfirm-specificevents,macroeconomicandfinancialmarketdevelopments,orsomecombinationoftheseevents. AbankingorganizationshouldalsoensurethatitsMISarecapableofincorporatingrelativelyrapidchangesinexposures,activities,andrisks. Whilestresstestingshouldutilizeavailablehistoricalinformation,abankingorganizationshouldlookbeyondassumptionsbasedonlyonhistoricaldataandchallengeconventionalassumptions. Abankingorganizationshouldensurethatitisnotconstrainedbypastexperienceandthatitconsidersmultiplescenarios,evenscenariosthathavenotoccurredintherecentpastorduringthebankingorganization’shistory. Forexample,abankingorganizationshouldnotassumethatifithassufferednoorminimallossesinacertainbusinesslineorproductthatsuchapatternwillcontinue. Structuralchangesincustomer,product,andfinancialmarketscanpresentunprecedentedsituationsforabankingorganization. Abankingorganizationwithanytypeofsignificantconcentrationcanbeparticularly vulnerabletorapidchangesineconomicandfinancialconditionsandshouldtrytoidentifyandbetterunderstandtheimpactofthosevulnerabilitiesinadvance. Forexample,therisksrelatedtoresidentialmortgageswereunderestimatedforanumberofyearsleadinguptothe2007-2009financialcrisisbyalargenumberofbankingorganizations,andthoseriskseventuallyaffectedthebankingorganizationsinavarietyofways. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

25 Effectivestresstestingcanhelpabankingorganizationidentifyanysuch concentrationsandhelpunderstandthepotentialimpactofseveralkeyaspectsofthebusinessbeingexposedtocommondrivers. Stresstestingshouldbeconductedovervariousrelevanttimehorizonstoadequatelycapturebothconditionsthatmaymaterializeintheneartermandadversesituationsthattakelongertodevelop. Forexample,whenabankingorganizationstresstestsaportfolioformarketandcreditriskssimultaneously,itshouldconsiderthatcertaincreditrisklossesmaytakelongertomaterializethanmarketrisklosses,andalsothattheseverityandspeedofmark-to-marketlossesmaycreatesignificantvulnerabilitiesforthefirm,evenifamorefundamentalanalysisofhowrealizedlossesmayplayoutovertimeseemstoshowlessthreateningresults. Abankingorganizationshouldcarefullyconsidertheincrementalandcumulativeeffectsofstressconditions,particularlywithrespecttopotentialinteractionsamongexposures,activities,andrisksandpossiblesecond-orderor“knock-on”effects. Inadditiontoconductingformal,routinestresstests,abankingorganizationshouldhavetheflexibilitytoconductneworadhocstresstestsinatimelymannertoaddress rapidlyemergingrisks. Theselessroutinetestsusuallycanbeconductedinashortamountoftimeandmaybesimplerandlessextensivethanabankingorganization’smoreformal,regulartests. However,foritsadhoctestsabankingorganizationshouldstillhavethecapacitytobringtogetherapproximatedinformationonrisks,exposures,andactivitiesandassesstheirimpact. Morebroadly,abankingorganizationshouldcontinueupdatingandmaintainingitsstresstestingframeworkinlightofnewrisks,betterunderstandingofthebankingorganization’sexposuresandactivities,newstresstestingtechniques,andanychangesinitsoperatingstructure andenvironment. Abankingorganization’sstresstestingdevelopmentshouldbeiterative,withongoingadjustmentsandrefinementstobettercalibratetheteststoprovidecurrentandrelevantinformation. Bankingorganizationsshoulddocumenttheongoingdevelopmentoftheirstress testingpractices. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

26 Principle4: Stresstestresultsshouldbeclear,actionable,wellsupported,andinformdecision-making. Stresstestingshouldincorporatemeasuresthatadequatelyandeffectivelyconveyresultsoftheimpactofadverseoutcomes. Suchmeasuresmayinclude,forexample,changestoassetvalues,accountingandeconomicprofitandloss,revenuestreams,liquiditylevels,cashflows,regulatorycapital,risk-weightedassets,theloanlossallowance,internalcapitalestimates,levelsofproblemassets,breachesincovenantsorkeytriggerlevels,orotherrelevantmeasures. Stresstestmeasuresshouldbetailoredtothetypeoftestandtheparticularlevelatwhichthetestisapplied(forexample,atthebusinesslineorrisklevel).Somestress testsmayrequireusingarangeofmeasurestoevaluatethefullimpactofcertain events,suchasaseveresystemicevent. Inaddition,allstresstestresultsshouldbeaccompaniedbydescriptiveandqualitativeinformation(suchaskeyassumptionsandlimitations)toallowuserstointerprettheexercisesincontext. Theanalysisandtheprocessshouldbewelldocumentedsothatstresstesting processescanbereplicatedifneedbe. Abankingorganizationshouldregularlycommunicatestresstestresultstoappropriatelevelswithinthebankingorganizationtofosterdialoguearoundstresstesting,keeptheboardofdirectors,management,andstaffapprised,andtoinformstresstestingapproaches,results,anddecisionsinotherareasofthebankingorganization. Abankingorganizationshouldmaintainaninternalsummaryoftestresultstodocumentatahighleveltherangeofitsstresstestingactivitiesandoutcomes,aswellasproposedfollow-upactions. Regularreviewofstresstestresultscanbeanimportantpartofabankingorganization’sabilityovertimetotracktheimpactofongoingbusinessactivities,changesinexposures,varyingeconomicconditions,andmarketmovementsonitsfinancialcondition. Inaddition,managementshouldreviewstresstestingactivitiesonaregularbasisto determine,amongotherthings,thevalidityoftheassumptions,theseverityoftests, BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

27 therobustnessoftheestimates,theperformanceofanyunderlyingmodels,andthestabilityandreasonablenessoftheresults. Stresstestresultsshouldinformanalysisanddecision-makingrelatedtobusinessstrategies,limits,riskprofile,andotheraspectsofriskmanagement,consistentwiththebankingorganization’sestablishedriskappetite. Abankingorganizationshouldreviewtheresultsofitsvariousstresstestswiththestrengthsandlimitationsofeachtestinmind(consistentwithPrinciple2),determineswhichresultsshouldbegivengreaterorlesserweight,analyzethecombinedimpactofitstests,andthenevaluatepotentialcoursesofactionbasedonthatanalysis. Abankingorganizationmaydecidetomaintainitscurrentcoursebasedontestresults;indeed,theresultsofhighlyseverestresstestsneednotalwaysindicatethatimmediateactionhastobetaken. Whereverpossible,benchmarkingorothercomparativeanalysisshouldbeusedtoevaluatethestresstestingresultsrelativetoothertoolsandmeasures–bothinternal andexternaltothebankingorganization–toprovidepropercontextandacheckonresults. Principle5: Anorganization’sstresstestingframeworkshouldincludestronggovernanceandeffectiveinternalcontrols. Similartootheraspectsofitsriskmanagement,abankingorganization’sstresstestingframeworkwillbeeffectiveonlyifitissubjecttostronggovernanceandeffectiveinternalcontrolstoensuretheframeworkisfunctioningasintended.Stronggovernanceandeffectiveinternalcontrolshelpensurethattheframeworkcontainscoreelements,fromclearlydefinedstresstestingobjectivestorecommendedactions. Importantly,stronggovernanceprovidescriticalreviewofelementsofthestresstestingframework,especiallyregardingkeyassumptions,uncertainties,andlimitations. Abankingorganizationshouldensurethatthestresstestingframeworkisnotisolatedwithinabankingorganization’sriskmanagementfunction,butisfirmlyintegratedintobusinesslines,capitalandasset-liabilitycommittees,andotherdecisionmakingbodies. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

28 Alongthoselines,theboardofdirectorsandseniormanagementshouldplaykeyrolesinensuringstronggovernanceandcontrols. Theextentandsophisticationofabankingorganization’sgovernanceoveritsstresstestingframeworkshouldalignwiththeextentandsophisticationofthatframework. Additionaldetailsregardinggovernanceandcontrolsofanorganization’sstresstestingframeworkareoutlinedinsectionVI. IV.StressTestingApproachesandApplications Thissectiondiscussessomegeneraltypesofstresstestingapproachesand applications. Foranytypeofstresstest,bankingorganizationsshouldindicatethespecificpurposeandthefocusofthetest. Definingthescopeofagivenstresstestisalsoimportant,whetheritappliesattheportfolio,businessline,risktype,orenterprise-widelevel,orevenjustforanindividualexposureorcounterparty. Basedonthepurposeandscopeofthetest,differentstresstestingtechniquesaremostuseful. Thus,abankingorganizationshouldemployseveralapproachesand applications;thesemightincludescenarioanalysis,sensitivityanalysis,enterprise-widestresstesting,andreversestresstesting. ConsistentwithPrinciple1,bankingorganizationsshouldapplythesecommensuratewiththeirsize,complexity,andbusinessprofile,andmaynotneedtoincorporateallofthedetailsdescribedbelow. ConsistentwithPrinciple3,bankingorganizationsshouldalsorecognizethatstresstestingapproacheswillevolveovertimeandtheyshouldupdatetheirpracticesasneeded. ScenarioAnalysis Scenarioanalysisreferstoatypeofstresstestinginwhichabankingorganizationapplieshistoricalorhypotheticalscenariostoassesstheimpactofvariouseventsandcircumstances,includingextremeones. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

29 Scenariosusuallyinvolvesomekindofcoherent,logicalnarrativeor“story”astowhycertaineventsandcircumstancescanoccurandinwhichcombinationandorder,suchasasevererecession,failureofamajorcounterparty,lossofmajorclients,naturalorman-madedisaster,localizedeconomicdownturn,disruptionsinfundingorcapitalmarkets,orasuddenchangeininterestratesbroughtaboutbyunfavorableinflationdevelopments. Scenarioanalysiscanbeappliedatvariouslevelsofthebankingorganization,suchaswithinindividualbusinesslinestohelpidentifyfactorsthatcouldharmthosebusinesslinesmost. Stressscenariosshouldreflectabankingorganization’suniquevulnerabilitiestofactorsthataffectitsexposures,activities,andrisks. Forexample,ifabankingorganizationisconcentratedinaparticularlineofbusiness,suchascommercialrealestateorresidentialmortgagelending,itwouldbeappropriatetoexploretheimpactofadownturninthoseparticularmarketsegments. Similarly,abankingorganizationwithlendingconcentrationstooilandgascompaniesshouldincludescenariosrelatedtotheenergysector. Otherrelevantfactorstobeconsideredinscenarioanalysisrelatetooperational,reputationalandlegalriskstoabankingorganization,suchassignificanteventsoffraudorlitigation,orasituationwhenabankingorganizationfeelscompelledtoprovidesupporttoanaffiliateorprovideothertypesofnon-contractualsupporttoavoidreputationaldamage. Scenariosshouldbeinternallyconsistentandportrayrealisticoutcomesbasedonunderlyingrelationshipsamongvariables,andshouldincludeonlythosemitigatingdevelopmentsthatareconsistentwiththescenario. Additionally,abankingorganizationshouldconsiderthebestmannertotryto capturecombinationsofstressfuleventsandcircumstances,includingsecond-orderand“knock-on”effects. Ultimately,abankingorganizationshouldselectanddesignmultiplescenariosthatarerelevanttoitsprofileandmakeintuitivesense,useenoughscenariostoexploretherangeofpotentialoutcomes,andensurethatthescenarioscontinuetobetimelyandrelevant. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

30 Abankingorganizationmayapplyscenarioanalysiswithinthecontextofitsexistingriskmeasurementtools(e.g.,theimpactofaseveredeclineinmarketpricesonabankingorganization’svalue-at-risk(VaR)measure)oruseitasanalternative,supplementalmeasure. Forinstance,abankingorganizationmayusescenarioanalysistomeasuretheimpactofaseverefinancialmarketdisturbanceandcomparethoseresultstowhatisproducedbyitsVaRorothermeasures. Thistypeofscenarioanalysisshouldaccountforknownshortcomingsofotherriskmeasurementpractices. Forexample,marketriskVaRmodelsgenerallyassumeliquidmarketswithknownprices. Scenarioanalysiscouldshedlightontheeffectsofabreakdowninliquidityandofvaluationdifficulties. Oneofthekeychallengeswithscenarioanalysisistotranslateascenariointobalancesheetimpact,changesinriskmeasures,potentiallosses,orothermeasuresofadversefinancialimpact,whichwouldvarydependingonthetestdesignandthetypeofscenarioused. Forsomeaspectsofscenarioanalysis,bankingorganizationsmayuseeconometricorsimilartypesofanalysistoestimatearelationshipbetweensomeunderlyingfactorsordriversandriskestimatesorlossprojectionsbasedonagivendataset,andthen extrapolatetoseetheimpactofmoresevereinputs. Careshouldbetakennottomakeassumptionsthatrelationshipsfrombenignormildlyadversetimeswillholdduringmoreseveretimesorthatestimatingsuchrelationshipsisrelativelystraightforward. Forexample,linearrelationshipsbetweenriskdriversandlossesmaybecomenonlinearduringtimesofstress. Inaddition,organizationsshouldrecognizethattherecanbemultiplepermutationsofoutcomesfromjustafewkeyriskdrivers. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

31 SensitivityAnalysis Sensitivityanalysisreferstoabankingorganization’sassessmentofitsexposures,activities,andriskswhencertainvariables,parameters,andinputsare“stressed”or“shocked.” Akeygoalofsensitivityanalysisistotesttheimpactofassumptionsonoutcomes.Generally,sensitivityanalysisdiffersfromscenarioanalysisinthatitinvolves changingvariables,parameters,orinputswithoutanexplicitunderlyingreasonornarrative,inordertoexplorewhatoccursunderarangeofinputsandatextremeor highlyadverselevels. Inthistypeofanalysisabankingorganizationmayrealize,forexample,thatagivenrelationshipismuchmoredifficulttoestimateatextremelevels. Abankingorganizationmayapplysensitivityanalysisatvariouslevelsofaggregationtoestimatetheimpactfromachangeinoneormorekeyvariables. Theresultsmayhelpabankingorganizationbetterunderstandtherangeofoutcomesfromsomeofitsmodels,suchasdevelopingadistributionofoutputbasedonavarietyofextremeinputs. Forexample,abankingorganizationmaychoosetocalculatearangeofchangestoastructuredsecurity’soverallvalueusingarangeofdifferentassumptionsabouttheperformanceandlinkageofunderlyingcashflows. Sensitivityanalysisshouldbeconductedperiodicallyduetopotentialchangesinabankingorganization’sexposures,activities,operatingenvironment,ortherelationshipofvariablestooneanother. Sensitivityanalysiscanalsohelptoassessacombinedimpactonabankingorganizationofseveralvariables,parameters,factors,ordrivers. Forexample,abankingorganizationcouldbetterunderstandtheimpactonitscreditlossesfromacombinedincreaseindefaultratesandadecreaseincollateralvalues. Abankingorganizationcouldalsoexploretheimpactofhighlyadversecapitalizationrates,declinesinnetoperatingincome,andreductionsincollateralwhenevaluatingitsrisksfromcommercialrealestateexposures. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

32 Sensitivityanalysiscanbeespeciallyusefulbecauseitisnotnecessarilyaccompaniedbyaparticularnarrativeorscenario;thatis,sensitivityanalysiscanprovidebankingorganizationsmoreflexibilitytoexploretheimpactofpotentialstressesthattheymaynotbeabletocaptureindesignedscenarios. Furthermore,bankingorganizationsmaydecidetoconductsensitivityanalysisoftheirscenarios,i.e.,choosingdifferentlevelsorpathsofvariablestounderstandthesensitivitiesofchoicesmadeduringscenariodesign. Forinstance,bankingorganizationsmaydecidetoapplyafewdifferentinterest-ratepathsforagivenscenario. Enterprise-WideStressTesting Enterprise-widestresstestingisanapplicationofstresstestingthatinvolvesassessingtheimpactofcertainspecifiedscenariosonthebankingorganizationasawhole,particularlywithregardtocapitalandliquidity. Asisthecasewithscenarioanalysismoregenerally,enterprisewidestresstestinginvolvesrobustscenariodesignandeffectivetranslationofscenariosintomeasuresofimpact. Enterprise-widestresstestscanhelpabankingorganizationinitseffortstoassesstheimpactofitsfullsetofrisksunderadverseeventsandcircumstances,butshouldbesupplementedwithotherstresstestsandotherriskmeasurementtoolsgiveninherentlimitationsincapturingallrisksandalladverseoutcomesinonetest. Scenariodesignforenterprise-widestresstestinginvolvesdevelopingscenariosthataffectthebankingorganizationasawholethatstemfrommacroeconomic, market-wide,and/orfirm-specificevents. Thesescenariosshouldincorporatethepotentialsimultaneousoccurrenceofbothfirm-specificandmacroeconomicandmarket-wideevents,consideringsystem-wideinteractionsandfeedbackeffects. Forexample,priceshocksmayleadtosignificantportfoliolosses,risingfunding gaps,aratingsdowngrade,anddiminishedaccesstofunding. Ingeneral,itisagoodpracticetoconsultwithalargesetofindividualswithinthebankingorganization–invariousbusinesslines,researchandriskareas–togainawideperspectiveonhowenterprisewidescenariosshouldbedesignedandtoensure BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

33 thatthescenarioscapturetherelevantaspectsofthebankingorganization’sbusinessandrisks. Bankingorganizationsshouldalsoconductscenariosofvaryingseveritytogaugetherelativeimpact. Atleastsomescenariosshouldbeofsufficientseveritytochallengetheviabilityofthebankingorganization,andshouldincludeinstantaneousmarketshocksandstressfulperiodsofextendedduration(e.g.,notjustaoneortwo-quartershockafterwhichconditionsreturntonormal). Selectionofscenariovariablesisimportantforenterprise-widetests,becausethese variablesgenerallyserveasthelinkbetweentheoverallnarrativeofthescenarioandtangibleimpactonthebankingorganizationasawhole. Forinstance,inaimingtocapturethecombinedimpactofasevererecessionandafinancialmarketdownturn,abankingorganizationmaychooseasetofvariablessuchaschangesingrossdomesticproduct(GDP),unemploymentrate,interestrates,stockmarketlevels,orhomepricelevels. However,particularlywhenassessingtheimpactonthewholebankingorganization,usingalargenumberofvariablescanmakeatestmorecumbersomeandcomplicated –soabankingorganizationmayalsobenefitfromsimplerscenariosorfromthose withfewervariables. Bankingorganizationsshouldbalancethecomprehensivenessofcontributingvariablesandtractabilityoftheexercise. Aswithscenarioanalysisgenerally,translatingscenariosintotangibleeffectsonthebankingorganizationasawholepresentscertainchallenges. Abankingorganizationshouldidentifyappropriateandmeaningfulmechanismsfortranslatingscenariosintorelevantinternalriskparametersthatprovideafirm-wideviewofrisksandunderstandingofhowtheserisksaretranslatedintolossestimates. Notallbusinessareasareequallyaffectedbyagivenscenario,andproblemsinonebusinessareacanhaveeffectsonotherunits. However,foranenterprise-widetest,assumptionsacrossbusinesslinesandriskareasshouldremainconstantforthechosenscenario,sincetheobjectiveistoseehowthebankingorganizationasawholewillbeaffectedbyacommonscenario. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

34 ReverseStressTesting Reversestresstestingisatoolthatallowsabankingorganizationtoassumeaknownadverseoutcome,suchassufferingacreditlossthatbreachesregulatorycapitalratiosorsufferingsevereliquidityconstraintsthatrenderitunabletomeetitsobligations,andthendeducethetypesofeventsthatcouldleadtosuchanoutcome. Thistypeofstresstestingmayhelpabankingorganizationtoconsiderscenariosbeyonditsnormalbusinessexpectationsandseetheimpactofseveresystemiceffectsonthebankingorganization. Italsoallowsabankingorganizationtochallengecommonassumptionsaboutitsperformanceandexpectedmitigationstrategies. Reversestresstestinghelpstoexploreso-called“breakthebank”situations,allowingabankingorganizationtosetasidetheissueofestimatingthelikelihoodofsevereeventsandtofocusmoreonwhatkindsofeventscouldthreatentheviabilityofthebankingorganization. Thistypeofstresstestingalsohelpsabankingorganizationevaluatethecombined effectofseveraltypesofextremeeventsandcircumstancesthatmightthreatenthesurvivalofthebankingorganization,evenifinisolationeachoftheeffectsmightbemanageable. Forinstance,reversestresstestingmayhelpabankingorganizationrecognizethata certainlevelofunemploymentwouldhaveasevereimpactoncreditlosses,thatamarketdisturbancecouldcreateadditionallossesandresultinrisingfundingcosts,andthatafirm-specificcaseoffraudwouldcauseevenfurtherlossesandreputationalimpactthatcouldthreatenabankingorganization’sviability. Insomecases,reversestresstestscouldrevealtoabankingorganizationthat“breakingthebank”isnotasremoteanoutcomeasoriginallythought. Giventhenumerouspotentialthreatstoabankingorganization’sviability,theorganizationshouldensurethatitfocusesfirstonthosescenariosthathavethelargestfirm-wideimpact,suchasinsolvencyorilliquidity,butalsoonthosethatseemmostimminentgiventhecurrentenvironment. Focusingonthemostprominentvulnerabilitieshelpsabankingorganizationprioritizeitschoiceofscenariosforreversestresstesting. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

35 However,abankingorganizationshouldalsoconsiderawiderrangeofpossiblescenariosthatcouldjeopardizetheviabilityofthebankingorganization,exploringwhatcouldrepresentpotentialblindspots. Reversestresstestingcanhighlightpreviouslyunacknowledgedsourcesofriskthatcouldbemitigatedthroughenhancedriskmanagement. V.StressTestingforAssessingtheAdequacyofCapitalandLiquidity Therearemanyusesofstresstestingwithinbankingorganizations. Prominentamongthesearestresstestsdesignedtoassesstheadequacyofcapitalandliquidity. Giventheimportanceofcapitalandliquiditytoabankingorganization’sviability,stresstestingshouldbeappliedinthesetwoareasinparticular,includinganevaluationoftheinteractionbetweencapitalandliquidityandthepotentialforbothtobecomeimpairedatthesametime. Depletionsandshortagesofcapitalorliquiditycancauseabankingorganizationtonolongerperformeffectivelyasafinancialintermediary,beviewedbyitscounterpartiesasnolongerviable,becomeinsolvent,ordiminishitscapacitytomeetlegalandfinancialobligations. Abankingorganization’scapitalandliquiditystresstestingshouldconsiderhowlosses,earnings,cashflows,capital,andliquiditywouldbeaffectedinanenvironmentinwhichmultiplerisksmanifestthemselvesatthesametime,forexample,anincreaseincreditlossesduringanadverse interest-rateenvironment. Additionally,bankingorganizationsshouldrecognizethatattheendofthetimehorizonconsideredbyagivenstresstest,theymaystillhavesubstantialresidualrisksorproblemexposuresthatmaycontinuetopressurecapitalandliquidityresources. Stresstestingforcapitalandliquidityadequacyshouldbeconductedincoordinationwithabankingorganization’soverallstrategyandannualplanningcycles. Resultsshouldberefreshedintheeventofmajorstrategicdecisions,orotherdecisionsthatcanmateriallyimpactcapitalorliquidity. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

36 Bankingorganizationsshouldconductstresstestingforcapitalandliquidityadequacyperiodically. CapitalStressTesting Capitalstresstestingresultscanserveasausefultooltosupportabankingorganization’scapitalplanningandcorporategovernance. Theymayhelpabankingorganizationbetterunderstanditsvulnerabilitiesandevaluatetheimpactofadverseoutcomesonitscapitalpositionandensurethatthebankingorganizationholdsadequatecapitalgivenitsbusinessmodel,includingthecomplexityofitsactivitiesanditsriskprofile. Capitalstresstestingcomplementsabankingorganization’sregulatorycapitalanalysisbyprovidingaforward-lookingassessmentofcapitaladequacy,usuallywithaforecasthorizonofatleasttwoyears(withtherecognitionthattheeffectsofcertainstressconditionscouldextendbeyondtwoyearsforsomestresstests),andhighlightingthepotentialadverseeffectsoncapitallevelsandratiosfromrisksnotfullycapturedinregulatorycapitalrequirements. Itshouldalsobeusedtohelpabankingorganizationassessthequalityand compositionofcapitalanditsabilitytoabsorblosses. Stresstestingcanaidcapitalcontingencyplanningbyhelpingmanagementidentify exposuresorrisksinadvancethatwouldneedtobereducedandactionsthatcouldbetakentobolstercapitallevelsorotherwisemaintaincapitaladequacy,aswellasactionsthatintimesofstressmightnotbepossible–suchasraisingcapital. Capitalstresstestingshouldincludeexercisesthatanalyzethepotentialforchangesinearnings,losses,reserves,andotherpotentialeffectsoncapitalunderavarietyofstressfulcircumstances. Suchtestingshouldalsocaptureanypotentialchangeinrisk-weightedassets,theabilityofcapitaltoabsorblosses,andanyresultingimpactonthebankingorganization’scapitalratios. Itshouldincludeallrelevantrisktypesandotherfactorsthathaveapotentialtoaffectcapitaladequacy,whetherdirectlyorindirectly,includingfirm-specificones. Abankingorganizationshouldalsoexplorethepotentialforpossiblebalancesheet expansiontoputpressureoncapitalratiosandconsiderriskmitigationandcapitalpreservationoptions,otherthansimplyshrinkingthebalancesheet. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

37 Capitalstresstestingshouldassessthepotentialimpactofabankingorganization’smaterialsubsidiariessufferingcapitalproblemsontheirown–suchasbeingunabletomeetlocalcountrycapitalrequirements–eveniftheconsolidatedbankingorganizationisnotencounteringproblems. Wherematerialrelativetothebankingorganization'scapital,counterpartyexposuresshouldalsobeincludedincapitalstresstesting. Enterprise-widestresstesting,asdescribedinsectionIV,shouldbeanintegralpartofabankingorganization’scapitalstresstesting. Suchenterprise-widetestingshouldincludeproformaestimatesofnotonlypotentiallossesandresourcesavailabletoabsorblosses,butalsopotentialplannedcapital actions(suchasdividendsorsharerepurchases)thatwouldaffectthebankingorganization’scapitalposition,includingregulatoryandothercapitalratios. Thereshouldalsobeconsiderationoftheimpactonthebankingorganization’sallowanceforloanandleaselossesandotherrelevantfinancialmetrics. Evenwithveryeffectiveenterprise-widetests,bankingorganizationsshouldusecapitalstresstestinginconjunctionwithotherinternalapproaches(inadditiontoregulatorymeasures)forassessingcapitaladequacy,suchasthosethatrelyprimarilyonstatisticalestimatesofriskorlossestimatesbasedonhistoricaldata. Liquiditystresstesting Abankingorganizationshouldalsoconductstresstestingforliquidityadequacy.Throughsuchstresstestingabankingorganizationcanworktoidentify vulnerabilitiesrelatedtoliquidityadequacyinlightofbothfirm-specificandmarket-widestresseventsandcircumstances. Effectivestresstestinghelpsabankingorganizationidentifyandquantifythedepth,source,anddegreeofpotentialliquidityandfundingstrainandtoanalyzepossibleimpactsonitscashflows,liquidityposition,profitability,andotheraspectsofitsfinancialconditionovervarioustimehorizons. Forexample,stresstestingcanbeusedtoexplorepotentialfundingshortfalls,shortagesinliquidassets,theinabilitytoissuedebt,exposuretopossibledeposit outflows,volatilityinshort-termbrokereddeposits,sensitivityoffundingtoaratingsdowngrade,andtheimpactofreducedcollateralvaluesonborrowingcapacityattheFederalHomeLoanBanks,theFederalReservediscountwindow,orothersecured BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

38 wholesalefundingsources. Liquiditystresstestingshouldexplorethepotentialimpactofadversedevelopmentsthatmayaffectmarketandassetliquidity,includingthefreezingupofcreditandfundingmarkets,andthecorrespondingimpactonthebankingorganization. Suchtestscanalsohelpidentifytheconditionsunderwhichbalancesheetsmightexpand,thuscreatingadditionalfundingneeds(e.g.,throughaccelerateddrawdownsonunfundedcommitments). Thesetestsalsohelpdeterminewhetherthebankingorganizationhasasufficientliquiditybuffertomeetvarioustypesoffutureliquiditydemandsunderstressfulconditions. Inthisregard,liquiditystresstestingshouldbeanintegralpartofthedevelopmentandmaintenanceofabankingorganization’scontingencyfundingplanning. LiquiditystresstestingshouldincludeenterprisewidetestsasdiscussedinsectionIV,butshouldalsobeapplied,asappropriate,atlowerlevelsofthebankingorganization,andinparticularshouldaccountforregulatoryorsupervisoryrestrictionson inter-affiliatefundingandassettransfers. Aswithcapitalstresstesting,bankingorganizationsmayneedtoconductliquiditystresstestsatboththeconsolidatedandsubsidiarylevel. Inundertakingenterprise-wideliquiditytestsbankingorganizationsshouldmakerealisticassumptionsastotheimplicationsofliquiditystressesinonepartofthebankingorganizationonotherparts. Aneffectivestresstestingframeworkshouldexplorethepotentialforcapitalandliquidityproblemstoariseatthesametimeorexacerbateoneanother. Forexample,abankingorganizationinastressedliquiditypositionisoftenrequiredtotakeactionsthathaveanegativedirectorindirectcapitalimpact(e.g.,sellingassetsatalossorincurringfundingcostsatabovemarketratestomeetfundingneeds). Abankingorganization’sliquiditystressanalysisshouldexploresituationsinwhichthebankingorganizationmaybeoperatingwithacapitalpositionthatexceedsregulatoryminimums,butisnonethelessviewedwithinthefinancialmarketsorbyitscounterpartiesasbeingofquestionableviability. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

39 Assessingthepotentialinteractionofcapitalandliquiditycanbechallengingandmaynotbepossiblewithinasinglestresstest,soorganizationsshouldexploreseveralavenuestoassessthatinteraction. Aswithotherapplicationsofstresstesting,foritscapitalandliquiditystresstests,itisbeneficialforabankingorganizationtoarticulateclearlyitsobjectivesfora post-stressoutcome,forinstancetoremainaviablefinancialmarketparticipantthat isabletomeetitsexistingandprospectiveobligationsandcommitments. Insuchcases,bankingorganizationswouldhavetoconsiderwhichmeasuresoffinancialconditionwouldneedtobemetonapost-stressbasistosecuretheconfidenceofcounterpartiesandmarketparticipants. VI.GovernanceandControls AsnotedunderPrinciple5,abankingorganization’sstresstestingframeworkwillbeeffectiveonlyifitissubjecttostronggovernanceandcontrolstoensuretheframeworkisfunctioningasintended. Theextentandsophisticationofabankingorganization’sgovernance overitsstresstestingframeworkshouldalignwiththeextentandsophisticationofthatframework. Governanceoverabankingorganization’sstresstestingframeworkrestswiththebankingorganization’sboardofdirectorsandseniormanagement. Aspartoftheiroverallresponsibilities,abankingorganization’sboardandseniormanagementshouldestablishacomprehensive,integratedandeffectivestresstesting frameworkthatfitsintothebroaderriskmanagementofthebankingorganization. Whiletheboardisultimatelyresponsibleforensuringthatthebankingorganizationhasaneffectivestresstestingframework,seniormanagementgenerallyhasresponsibilityforimplementingthatframework. Seniormanagementdutiesshouldincludeestablishingadequatepoliciesandproceduresandensuringcompliancewiththosepoliciesandprocedures,assigningcompetentstaff,overseeingstresstestdevelopmentandimplementation,evaluatingstresstestresults,reviewinganyfindingsrelatedtothefunctioningofstresstestprocesses,andtakingpromptremedialactionwherenecessary. Seniormanagement,directlyandthroughrelevantcommittees,alsoshouldbe BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

40 responsibleforregularlyreportingtotheboardonstresstestingdevelopments(includingtheprocesstodesigntestsanddevelopscenarios)andonstresstestingresults(includingfromindividualtests,wherematerial),aswellasoncompliancewithstresstestingpolicy. Boardmembersshouldactivelyevaluateanddiscussthisinformation,ensuringthatthestresstestingframeworkisinlinewiththebankingorganization’sriskappetite,overallstrategyandbusinessplans,andcontingencyplans,directingchangeswhereappropriate. Abankingorganizationshouldhavewrittenpolicies,approvedandannuallyreviewedbytheboard,thatdirectandgoverntheimplementationofthestresstesting frameworkinacomprehensivemanner. Policies,alongwithprocedurestoimplementthem,should:Describetheoverallpurposeofstresstestingactivities; Articulateconsistentandsufficientlyrigorousstresstestingpracticesacrosstheentirebankingorganization; Indicatestresstestingrolesandresponsibilities,includingcontrolsoverexternalresourcesusedforanypartofstresstesting(suchasvendorsanddataproviders); Describethefrequencyandprioritywithwhichstresstestingactivitiesshouldbe conducted; Indicatehowstresstestresultsareused,bywhom,andoutlineinstancesinwhichremedialactionsshouldbetaken;and Bereviewedandupdatedasnecessarytoensurethatstresstestingpracticesremainappropriateandkeepuptodatewithchangesinmarketconditions,bankingorganizationproductsandstrategies,bankingorganizationexposuresandactivities,thebankingorganization’sestablishedriskappetite,andindustrystresstestingpractices. Astresstestingframeworkshouldincorporatevalidationorothertypeofindependentreviewtoensuretheintegrityofstresstestingprocessesandresults,consistentwithexistingsupervisoryexpectations. Ifabankingorganizationengagesathirdpartyvendortosupportsomeorallofitsstresstestingactivities,thereshouldbeappropriatecontrolsinplacetoensurethat BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

41 thoseexternallydevelopedsystemsandprocessesaresound,appliedcorrectly,andappropriateforthebankingorganization’srisks,activities,andexposures. Additionally,seniormanagementshouldbemindfulofanypotentialinconsistencies,contradictions,orgapsamongitsstresstestsandassesswhatactionsshouldbetakenasaresult. Internalauditshouldalsoprovideindependentevaluationoftheongoingperformance,integrity,andreliabilityofthestresstestingframework. Abankingorganizationshouldensurethatitsstresstestsaredocumentedappropriately,includingadescriptionofthetypesofstresstestsandmethodologies used,keyassumptions,results,andsuggestedactions. Seniormanagement,inconsultationwiththeboard,shouldreviewstresstestingactivitiesandresultswithanappropriatelycriticaleyeandensurethatthereisobjectivereviewofallstresstestingprocesses. Theresultsofstresstestinganalysesshouldfacilitatedecision-makingbytheboardandseniormanagement. Stresstestingresultsshouldbeusedtoinformtheboardaboutalignmentofthebankingorganization’sriskprofilewiththeboard’schosenriskappetite,aswellasinformoperatingandstrategicdecisions. Stresstestingresultsshouldbeconsidereddirectlybytheboardandseniormanagementfordecisionsrelatingtocapitalandliquidityadequacy,includingcapitalcontingencyplansandcontingencyfundingplans. Seniormanagement,inconsultationwiththeboard,shouldensurethatthestresstestingframeworkincludesasufficientrangeofstresstestingactivitiesappliedattheappropriatelevelsofthebankingorganization(i.e.,notjustoneenterprise-widestresstest). Soundgovernancealsoincludesusingstresstestingtoconsidertheeffectivenessofabankingorganization’sriskmitigationtechniquesforvariousrisktypesovertheirrespectivetimehorizons,suchastoexplorewhatcouldoccurifexpectedmitigationtechniquesbreakdownduringstressfulperiods. VII.Conclusion Abankingorganizationshouldusetheprincipleslaidoutinthisguidancetodevelop, BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

42 implement,andmaintainaneffectivestresstestingframework. Suchaframeworkshouldbeadequatelytailoredtothebankingorganization’ssize,complexity,risks,exposures,andactivities. Akeypurposeofstresstestingistoexplorevarioustypesofpossibleoutcomes,includingrareandextremeeventsandcircumstances,assesstheirimpactonthebankingorganization,andthenevaluatetheboundariesuptowhichthebankingorganizationplanstobeabletowithstandsuchoutcomes. Stresstestingmaybeparticularlyvaluableduringbenignperiodswhenothermeasuresmaynotindicateemergingrisks. Whilestresstestingcanprovidevaluableinformationregardingpotentialfutureoutcomes,similartoanyotherriskmanagementtoolithaslimitationsandcannotprovideabsolutecertaintyregardingtheimplicationsofassumedeventsandimpacts. Furthermore,managementshouldensurethatstresstestingactivitiesarenotconstrainedtoreflectpastexperiences,butinsteadconsiderabroadrangeofpossibilities. Nosinglestresstestcanaccuratelyestimatetheimpactofallstressfuleventsandcircumstances;therefore,abankingorganizationshouldunderstandandaccountforstresstestinglimitationsanduncertainties,andusestresstestsincombinationwithotherriskmanagementtoolstomakeinformedriskmanagementandbusinessdecisions. BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com

43 GuidelinesonStressedValue-At-Risk(StressedVaR)andontheIncrementalDefaultandMigrationRiskCharge(IRC) 16May2012 TheEBApublishedtodaytwosetsofGuidelinesonStressedValue-At-Risk(StressedVaR)andontheIncrementalDefaultandMigrationRiskCharge(IRC)modellingapproachesemployedbycreditinstitutionsusingtheInternalModelApproach(IMA). TheseGuidelinesareseenasanimportantmeansofaddressingweaknessesintheregulatorycapitalframeworkandintheriskmanagementoffinancialinstitutions. TheirobjectiveistocontributetoalevelplayingfieldandtoenhanceconvergenceofsupervisorypracticesacrosstheEU. NationalcompetentauthoritiesareexpectedtoimplementtheprovisionssetoutintheGuidelineswithinsixmonthsaftertheirpublication. Afterthatdate,thecompetentauthoritiesmustensurethatinstitutionscomplywiththeGuidelineseffectively. GuidelinesonStressedValue-At-Risk(StressedVaR) TheseGuidelinesincludeprovisionsonStressedVaRmodellingbycreditinstitutionsusingtheInternalModelApproachforthecalculationoftherequiredcapitalformarketriskinthetradingbook. ThemainprovisionsoftheGuidelinesrelateto: BaseliiiComplianceProfessionalsAssociation(BiiiCPA) www.basel-iii-association.com