Download

1 / 8

90 likes | 656 Views

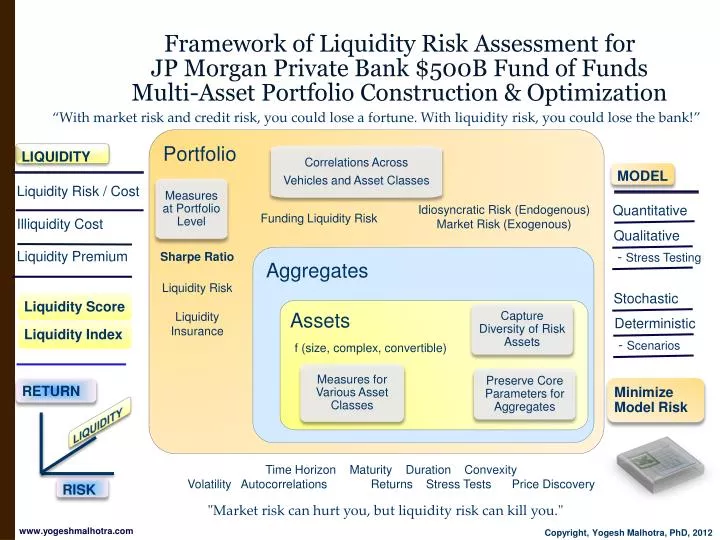

Framework of Liquidity Risk Assessment for JP Morgan Private Bank $500B Fund of Funds Multi-Asset Portfolio Construction & Optimization. “With market risk and credit risk, you could lose a fortune. With liquidity risk, you could lose the bank!”. LIQUIDITY. MODEL. Liquidity Risk / Cost.

E N D

Framework of Liquidity Risk Assessment forJP Morgan Private Bank $500B Fund of FundsMulti-Asset Portfolio Construction & Optimization “With market risk and credit risk, you could lose a fortune. With liquidity risk, you could lose the bank!” • LIQUIDITY • MODEL • Liquidity Risk / Cost • Quantitative • Portfolio • Illiquidity Cost • Qualitative • Correlations Across • Vehicles and Asset Classes • Liquidity Premium • - Stress Testing • Stochastic • Measures at Portfolio Level • Liquidity Score • Deterministic • Liquidity Index Idiosyncratic Risk (Endogenous) Market Risk (Exogenous) • - Scenarios Funding Liquidity Risk • RETURN • MinimizeModel Risk Sharpe Ratio Liquidity Risk Liquidity Insurance • Aggregates • LIQUIDITY • RISK • Assets Capture Diversity of Risk Assets f (size, complex, convertible) Measures for Various Asset Classes Preserve Core Parameters for Aggregates Time Horizon Maturity Duration Convexity Volatility Autocorrelations Returns Stress Tests Price Discovery "Market risk can hurt you, but liquidity risk can kill you."

Current State of Liquidity Research • Late in Liquidity Focus • Efficient, Complete, Frictionless Markets • Market MicrostructureSingle Asset FocusTypically Equities* • HF Liquidity Ser. Corr.Liquidity-Optimized Portfolio (Lo, 2010) • MV Liquidity obj. function • HFs Time Liquidity,Spurious Serial Correlation: HF ReturnsSharpe Ratios Biased Up • Liquidity Risks & Correlation Risks(Acharya & Schaefer 2006) • Asset Return Shocks Liquidity Shocks • Prices exhibit 2 RegimesNormal & Illiquidity(Capital and Collateral) • Tightness, Depth, Resilience (Kyle, 1985) "Liquidity is a great metaphor, but we still don't have an unambiguous definition of it." • Market Liquidity Asset trades quickly & little price impact for big volume. • F(time, price, volume) • Funding LiquidityCF to fund assets and meet obligations as they’re due. • S.T. CFIN L.T. CFOUTMaturity Transformation • Liquidity and SolvencySystemic Risk of Failure • Two Minimum Standards(Funding Liquidity Buffers)Liquidity Coverage Ratio, 30- High Quality Liquid AssetsNet Stable Funding Ratio- Minimum Stable Funding • Measure, Monitor, Manage Currencies | Stress Testing • Forward Liquidity ExposureCounter-Balancing Capacity- ‘Liquidity Buffer’ (Fiedler)- BSL = CBC - FLE- Transfer Pricing of Liquidity • LiquificationAlgorithm/Score- Term Structure, Repo, FAI • Interest Rate Risk Gaps & Liquidity Risk Gaps (Matz)LG: A&L |CF (Time)RG: A&L |Re-Price (Time) • Capital Market PlayersUnpredictable Variation in Transaction Costs (t,p,v) • Risk ManagersUnpredictable Variation in FundingCash Shortfalls • Focus on CFs instead of PVs for Funding Liquidity (Fiedler, Deutsche Bnk, 2000)Liquidity Term Structure • AI Liq. Ser. Corr. (Barclay) • Heat Map, Beyond VaR, Stress Test (McKinsey). • Risk Parity (PIMCO) • Non-Normality Serial Correlation, Fat Tails, Correlation Breakdown35% lock up for 5% payout.Severity & Likelihood.Higher FI, Lower S&L.Unsmoothing AI Risk. (Sheikh & Qiao, JPM ’09, ‘10).Yields, Liquidity, Risk JPM 11BSL Simulation MC (Algo.) • CF Gaps (Moody’s) • VaR: Not Subadditive: • Not coherent measure.R(L1+L2)R(L1)+R(L2) • Liquidity Adjusted VaRES, ETL, CVAR, SpectralMerrill VaR $92M, Loss $18B • (Black Swans, Fat Tails) • Mean-Variance/CAPM/Sharpe Ratio (Normal): Ignore Liquidity Risk. • Price Impact: Large TradeMarket Microstructure LVaR = position ($) * [-drift (%) + volatility *deviate + LC]; 0.5*spread " No single measure captures the various aspects of liquidity in financial markets."

Current State of Liquidity Risk Measures “Comparing individual assets’ liquidities is problematic because one asset could be more liquid along one dimension of transaction costs while the other is more liquid in a different dimension.” • Tightness, Depth, Resilience (Kyle, 1985) • Aggregates of Multiple Basic Liquidity MeasuresBid Ask, Volume, Turnover, Loeb Price Impact (Lo 2010)(Amount of Trading, Cost) • Serial Correlation as proxy. • Liquidity Adjusted CAPM(Acharya& Pedersen, 2005 JFE)Risky and has CommonalityConstant Trading Frictions • Volume Weighted Spreads • 1. Bid Ask Spread, • 2.Transactions (Volume), • 3.Volume Weighted Spreads • Popular Liquidity Models • (Price, Quantity, Time) • Bid-Ask Spread Exogenous • Position Size Endogenous • Resiliency (Rare) • Trading Volume (Flawed) • - Flash Crash • Aggregates of Multiple Basic Liquidity Measures • Long-Short Index MeasureChacko, Das, Fan (2012)Long the ETFsShort components of ETFs • Liquidity as Shadow Asset: Kinlaw et al. (2012)- Identify optimal weights by maximizing expected utility- Substitute illiquid asset for liquid equity- Solve for illiquid asset return based on σand ρ- Estimate AR(1) Model using least squares- De-smooth the time series • Liquidity as Real Option:Ang & Bollen (2008)Investor’s decision to withdraw capital: real optionLockups & Notice periods: exercise restrictions: reduction in the value of liquidity option. • Autocorrelations as Proxy For HF Liquidity (Lo, 2005) Dynamic and Nonlinear Exposures; Credit and Liquidity Risk; Leverage & CollateralHF Serial Correlation: • Proxy for Frictions: LiquidityIlliquidMark to ‘Smooth’=> Sharpe Ser. Corr. Basel Committee Jarrow & Protter (2005) Stange and Kaserer (2008) Giot & Gramming (2005) Bangia et al. (2001) Berkowitz (2000) "No bank can ever afford to hold enough liquidity during normal times to be able to survive a severe or prolonged funding disruption."

Autocorrelation Measure of Relative Liquidity &Setup for a Wall Street Asset Management Firm "Liquidity risk today is where credit risk was 10 years ago." • Assets: SpecificAssets: General Portfolio • Portfolio LiquidityWeighted Average of Asset Liquidity • Portfolio Risk Buckets • Market Risk, Inflation Hedge, Illiquid, Liquidity • Alternative MeasurePortfolios Days to Liquidate = TS • = Asset i Market ValueTS = Time to liquidate i • WALF = • LF = Liq. Rank * Duration Factor * Price Effect • Relative Liquidity Absolute Liquidity • Use data point for liquidity premium size for an asset class • NA, Limited research for illiquid assets • Rule of thumb, Return Premium for PE = 6% • Return premium = Skill + Leverage + Liquidity • Taking all three equal, Y for PE = 2% • Use above to compute Y for other Asset Classes. • Representative Y for Assets • Currency ~ 0Large Cap Very lowConvertible Bonds 1.65%Private Equity 2.00%Direct Real Estate 2.74% • Relative LiquiditySerial Correlation Ser. Corr. or Autocorrelation of same asset’s prices across time. • Liquidity Premium • LiquiditySer. Corr. • Serial Correlation Y • Scale for Relative Liquidity • How fast price (t) decays - Faster decay, more liquid • How long stale price (t) lasts- More it affects, less liquid- Longer it lasts, less liquid • Y Proxy for Liquidity Risk • Plot serial correlations • Use Model to find Decay • Measure Decay Factor • Constant a • Exponential Decay Factor b • Time Lag X: t+1, t+2, … • Liquidity Premium 0 to 1.0:b = 1.0 No Decayb > 1.0 Not Real (time)b = 0 No Ser. Corr.b < 0 Not Real (-,+,-,+) • Asset Allocation Risk Parity • Illiquidity of HF assets Spurious Ser. Corr. of HF returns Reported returns are smoother than true returns. Downward bias on estimated return variance, +ve Ser. Corr. Correcting for smoothed returns Worse Sharpe ratios. (GetmansyJFE 2004) • Liquidity Risk (time, price, volume)UnsustainableS.T. CFIN L.T. CFOUT • Mismatch Between • Asset Holding PeriodInvestment Horizon • Normal regime: MatchIlliquidity regime: MismatchSeparate Models for the Two " In times of financial crisis, asset prices in some markets may reflect the amount of liquidity available in the market rather than the future earning power of the asset."

Post-2008 Trends Requiring Research Advances forWall Street Firm Multi-Asset Portfolio of 16 Asset Classes " People have known since Mandelbrot in 1963 that returns are not normally distributed." • Alternative Investments Liquidity Fund of Funds • Liquidity Risk Paradox • Illiquid Bid-Ask, Volume • Alternative Measures • Market Cap, % Stock Ownership, Size of Fixed Income InstrumentE.g.: StatPro • Asset Risk vs. Fund Risk • Liquidity Position vs. Fund • Liquidity Crisis • UnsustainableS.T. CFIN L.T. CFOUT • Fund of Fund Trade-Offs • Liquidity • Maturity • Size • Performance • . • Liquidity VolumeHFT => artificial liquidity • Liquidity vs. Volatility • Risk Volatility (Model Risk) • Loss Probability • Potential Magnitude • EL | Long Periods • Liquidity / Market Activity Leading indicator of price movement(Correlations) • Greater time available for liquidation, lesser risk. • Simple assets more liquid than complex assets. • OTC Markets are ‘thin’ but Exchanges are ‘deep.’ • . • Alternative Investments • High Market Liquidity RiskTrading Costs, Cash Mgmt., Volatility, Return* • Liquidity Management • Transparency of Underlying • Real Time* Liquidity • Stressed* Liquidity • Liquidity Inhibitors • Liquidity Strategy • Redemptions, Lockups & Gates • Expectations • Past Illiquidity/Loss • Can’t Predict Future Illiquidity/Loss: Regime [1 2]Illiquidity [Premium Discount] • Hidden RisksQuiet FactorsNegative Convexity (Callable)Mark to Market (Correlations) • New Global Risk Indicators • Credit spreads • Bid-Ask Spreads • Trade Volumes • Correlation Matrices • Forward Duration Curves • Positions Outstanding • New Macro Risk Indicators • Systemic vs. Specific Risk • Tradition VIX as IndicatorBreakdown of VIX, Volatility • Non-Normal Returns‘Chaotic’ Returns • No Risk-Free Rates • Inflation Expectations • Future Volatility Concerns • Future Credit Concerns • Sovereign Default "I'd just caution you that models are backward-looking. The future isn’t the past."

Framework of Liquidity Assessment forWall Street Asset Management Firm’s Multi-Asset Portfolio Construction & Optimization • Liquidity [Risk] Measures: Asset Classes, Aggregates, Portfolio • Framework • 16-Asset Class Portfolio Liquidity Assessment • Defined Asset Classes & Aggregates (Vehicles) • Endogenous Liquidity: Time / Maturity / Duration, Volatility / Autocorrelations, Returns / Stress Tests: Price Discovery • 16-Asset Class Portfolio Optimization: Sharpe / Liquidity Risk / Liquidity Insurance • Funding Liquidity Risk, Asset Liquidity Risk • Idiosyncratic (Endogenous), Market (Exogenous) • Models: Quantitative + Qualitative, Stochastic + Deterministic Stress Testing Scenarios Minimize Model Risk • Assets Modeled: Hedge Funds (HF), Alternative Investments, Equities, Commodities, Fixed Income, Bonds, Currencies "Normality has been an accepted wisdom in economics and finance for a century or more. Yet in real-world systems, nothing could be less normal than normality. Tails should not be unexpected, for they are the rule."

Portfolio ConstructionFramework: An Overview MODELS / MEASURES Aggregate the Measures • PORTFOLIOReturnsLiquidity CostsCorrelationsVolatilities • Normalize the • Measures • AGGREGATESReturnsLiquidity CostsCorrelationsVolatilities • Standardize theMeasures • ASSETSReturnsLiquidity CostsCorrelationsVolatilities • Select Most Robust Measures "It is truly an art to build a long-term robust quantitative model that will perform well out-of-sample and through several different types of market environments.”

REPLICATE VALIDATE Implementation Model MODELS / MEASURES SIMULATE • PARAMETERS • Market Data • STRESS TESTS • Data Feeds • SHOCKS • Other Updates "I think you should be ambitious about your models, and push them as far as you can, but you need to be aware they will fail - and under what circumstances.”