Download

1 / 23

230 likes | 393 Views

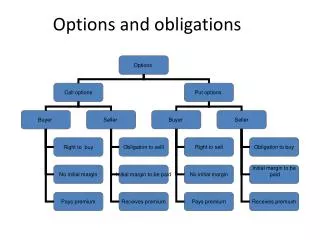

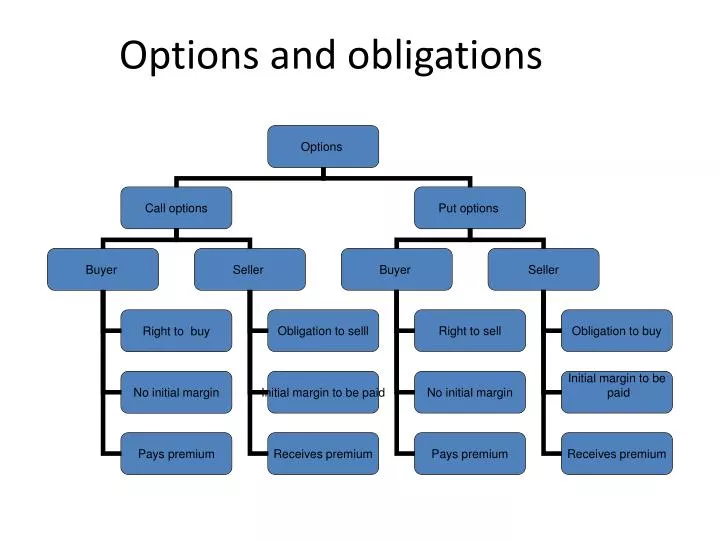

Options and obligations . Margining system for Seller of Options. Initial Margin- Risk margin Premium margin Assignment margin Initial margin –According SPAN formula- Historical volatility of asset in the past If price of the asset increases- Call Writer’s financial loss increases

E N D

Margining system for Seller of Options • Initial Margin- Risk margin • Premium margin • Assignment margin • Initial margin –According SPAN formula- Historical volatility of asset in the past • If price of the asset increases- Call Writer’s financial loss increases • If price of the asset decreases- Put Writers’ financial loss increases

Margining-Continuing • Premium margin- Deposit of collected premiums by the Seller of options with the clearing house • Increase in the premium- result additional margin to be brought than at the premium when they sold options and vice versa

Long call and short call -example • Assume that Mr.ABC has purchased a call option on stock X at Rs.100 by paying a premium of Re1 to the seller of a call option Mr.PQR .Let us see the range of prices above and below the exercise price and observe the profit trend of both the buyer and the seller

Long put and Short put –example • Assume that Mr.ABC has purchased a put option on stock X at Rs.100 by paying a premium of Re1 to the seller of a put option Mr.PQR . Let us see the range of prices above and below the exercise price and observe the profit trend of both buyer and seller

In the money-At the money • Call option: when stock price raises than the strike price and brings money to the buyer • Put option :when stock price declines than the strike price and brings money to the buyer • When the strike and stock prices are the same – no advantage position to exercise

Out of the money • There is no definitive advantage in exercising an option in situation –Out of the money – no need to abandon . • Example

Intrinsic value and Time value of the option • Option premium-Option price • =Intrinsic value + Time value or Extrinsic value • Intrinsic value of the option : the part of premium which represents to the extent to which the option is I-T-M;Intrinsic value of the option – never be negative : A-T-M and O-T-M => intrinsic value is zero

Intrinsic value of the option • Consider a share currently trading at Rs.235. Assume you hold a Rs.200 call and a Rs.260 call . At the same time you also hold a Rs.200 put and a Rs.260

Time value of the option • Quantification of the probability of the change in the underlying price to become in the money during the remaining period of option • Time value= Option premium-Intrinsic value • Value of option-Intirnsic value= Time value of the option • If the option is A-T-M and O-T-M the entire premium is time value of option

Effect of time decay • Assume that we bought a call option with exercise price of Rs235 and the share price in the market is Rs 240 . It is also known that we paid a premium of Rs.32 for this 60 day contract How much of this 2 month option’s premium is time value ?

Valuation of Options B-S model • Black and Scholes -1973 • Direct work of Rober merton , Black and Scholes • 1997-Nobel winners Robert merton and Scholes • 1995- Black died • “The pricing of options and corporate liabilities “ • Stock price , strike price , expiration date , risk free rate of return and the standard deviation of stock return (volatility)

B-S model • C=SN(d1)-Xe-rt N(d2) • C= price of the call option • S= price of the underlying stock • X=options exercise price • R=risk free interest • T=current time until expiration • N=area under the normal curve • D1=[ln(S/X)+(r+σ2/2)T]/ σ T1/2 • D2 = d1- σ T1/2

Option Problems-Call and Put • Tata Motors stock is currently selling for Rs.750 . There is call option on Tata motors with a maturity of 90 days and an exercise price of Rs.800 .The volatility in the stock price is estimated to be 22% The risk free rate is 8% What will be the price of call option?

Synthetic Long call strategy –Buy Stock and Buy Put • Buy the stock – anticipating the price rise • Instead – If price comes down –to have insurance –Put option • The strike price either equals the stock bought or below i-e A-T-M or O-T-M • Strategy is resembling like a call option but not real call option • Risk (Maximum losses)Stock price +put premium –put strike price • Break even : Stock price+ Put premium • Investor- conservatively bullish

Synthetic call –Buy stock and Buy put • Holding the stock for reaping the benefits ,dividends ,rights and so on but at the same time insuring against an adverse price movement • Simple buy call- no underlying • Example • ABC ltd is trading at Rs.4000 on 4th July • Buy 100 shares of the stock at Rs4000 • Buy 100 July put options with a strike price of Rs.3900 at a premium of Rs143.80 per put • Pay off the synthetic call: Payoff from the stock+ Pay off from the put option

Pay off diagrams • + = Buy Buy synthetic call Stock Put

Synthetic put /Protective Call /Synthetic Long put /Synthetic Short • Short on a stock • Buy the call either A-T-M or O-T-M • In case the price falls he will gain out of the price fall • If any unexpected price –loss is limited • Pay off the long call compensates the loss out of the stock short position • Bearish and to protect from the unexpected price increase

Synthetic put /Protective Call /Synthetic Long put /Synthetic Short • The expectation of the investor is – prices will go down but against the price rise • Risk: call strike price –stock price +premium • Reward : Maximum stock price-call option pay off • Maximum is Comparision of Stock price and Stock sold at • Breakeven Stock price –call premium

Synthetic put /Protective Call /Synthetic Long put /Synthetic Short • Example ABC ltd is trading at Rs.4457 in June . An investor Mr.A buys a Rs.4500 call for Rs100 while shorting the stock at Rs.4457

Synthetic put /Protective Call /Synthetic Long put /Synthetic Short + = • Sell Stock Buy call Synthetic short

Covered call –owning the stock and sell call • When to use:usually adopted by the investor owns who is neutral to moderately bullish about the stock • But bearish in the near term • The target price at which he wants exit- strike price and should O-T-M • Investor earns premium from the buyer of call option –at or below the strike price

Covered call –buy stock + Sell call • Example :Mr A bought XYZ Ltd for Rs.3850 and simultaneously sells a call at a strike price of Rs.4000. The price of XYZ ltd stays at or below Rs.4000 . The call buyer will not exercise the call option Mr.A will keep the premium of Rs.80 . Mr A bought XYZ ltd for Rs.3850 and the call option .If the stock moved between Rs.3850 to 3950 Profit is ? • The price of stock moves to Rs.4100