Download

1 / 26

260 likes | 415 Views

Adjustments to Income. For AGI and From AGI. Deductions For AGI Had any expenses as an educator Received income from self-employment Paid a penalty for early withdrawal of savings Paid alimony Made contributions to a traditional IRA Paid student loan interest

E N D

For AGI and From AGI • Deductions For AGI • Had any expenses as an educator • Received income from self-employment • Paid a penalty for early withdrawal of savings • Paid alimony • Made contributions to a traditional IRA • Paid student loan interest • Received income from jury duty that was turned over to an employer • Paid college tuition • Deductions From AGI • Standard Deduction • Itemized Deduction

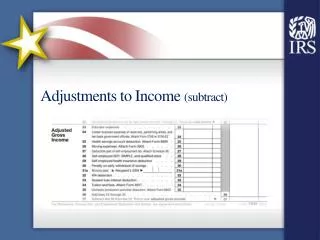

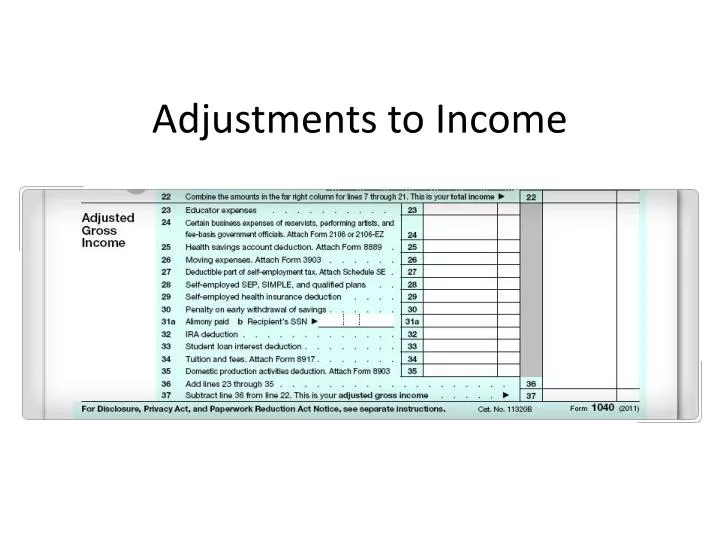

Adjustments Breakdown • The taxpayer's total adjusted gross income (AGI) is the amount that is used to compute some limitations, such as the medical and dental deduction on Schedule A and the credit for child and dependent care expenses. To find the taxpayer's AGI, follow the instructions on Form 1040: • Add the amounts in the far right column of the Income section (lines 7 through 21) and enter the result on line 22. This is the taxpayer's total income. • Add the Adjustments to Income (the amounts in lines 23 through 35) and enter the result on line 36. These are the total Adjustments. • Subtract line 36 from line 22 and enter the result on line 37. This is the AGI.

Types of Expenses For AGI • Had any expenses as an educator • Received income from self-employment • Paid a penalty for early withdrawal of savings • Paid alimony • Made contributions to a traditional IRA • Paid student loan interest • Received income from jury duty that was turned over to an employer • Paid college tuition

Educator Expenses • Who Qualifies? • Teacher, instructor, counselor, principal, or aide for grades K-12, employed at least 900 hours are eligible( ineligible are Home-School) • Expenses that qualify include books, supplies, equipment (including computer equipment, software, and services), and other materials used in the classroom. • Expenses that do not qualify are home schooling, nonathletic supplies for physical education, or health courses.

Educator Expenses Continued • Individual • can deduct no more than $250 • Spouse (both are educators) • Can deduct no more than $500 together if you exceed this for either spouse the excess may be treated as an itemized employment-related deduction on Schedule A. • Each taxpayer can not deduct more than $250 • Educator expenses are reduced by any of these applicable reimbursements: • Any reimbursement that is not listed on Form W-2( from the school you worked) • Redeemed tax-free interest on U.S. Series EE and I Savings Bonds • Excludable payments from a Qualified Tuition Program (QTP) or Coverdell Education Savings Account (ESA)

Self Employment Tax • A portion of self employment tax is deductible • Must complete Form SE • Line 27 on the Adjustments for Gross Income • 50% of SE deductible

Early Withdrawal Penalty • Taxpayers can adjust their income by deducting penalties they paid for withdrawing funds from a deferred interest account before maturity. • Must have Form 1099-INT, Interest Income, or Form 1099-OID, Original Issue Discount, documenting the penalty. • The penalty is entered into the interest statement of TaxWise.

Alimony Paid • Tax payer paying a spouse or former spouse under a divorce or separation instrument • Payments made in form of: • Cash • Payment of spouse’s expenses(such as medical bills, housing costs, and other expenses can qualify as alimony.) • Child support and voluntary payments are not deductible • Taxpayer considers qualified payments as deductible income • Taxpayer receiving alimony must treat it as income

Where to Look/Tips • Alimony Requirements in the Adjustments section of the Volunteer Resource Guide (Tab E). • For additional information on alimony, refer to the Alimony chapter in Publication 17 and Publication 504, Divorced or Separated Individuals.

IRA Contributions • A traditional IRA is any IRA that is not a Roth or Simple IRA. • Benefits of a traditional IRA: • Some contributions may be deductible • Amounts are not taxed until distributed • Retirement Savings Contribution Credit

IRA Contributions-Guidelines to Follow • Eligibility Requirements: • Types of IRAs: Verify the types to which the taxpayer and spouse contributed. Only contributions to traditional IRAs are deductible. • Age Limit: Taxpayers can contribute to a traditional IRA only if they are less than 70 ⅟₂ years of age at the end of the tax year. • Compensation: Individuals must have taxable compensation (wages, self-employment income, commissions, taxable alimony, taxable scholarships or fellowships. • Time limits: Contributions must be made by the due date for filing the return, not including extensions. Verify with taxpayer that contributions were made by the due date of the return.

IRA Contributions-Guidelines to Follow • Factors that affect whether Traditional IRA are deductible are: • Whether the taxpayer (or spouse, if Married Filing Jointly) is covered by a retirement plan at work, and • The taxpayer's Modified Adjusted Gross Income (MAGI) before taking the deduction. • If the taxpayer or spouse is covered by a retirement plan, the deduction amount will be reduced or eliminated if the MAGI on the tax return is above a certain limit.

IRA Contributions Limits • There is a limit on the amount taxpayers can contribute to traditional IRAs. The total contribution—that is, the combined contributions to all accounts, including Roth and traditional IRAs—cannot be more than the smaller of: • $5,000 ($6,000 if age 50 or older by the end of the tax year), or • A taxpayer's compensation includible as income for the year

IRA Contributions Limits Continued • Spousal IRAs are also subject to certain limitations. If married taxpayers file a joint return and one spouse's compensation is less than the other spouse's compensation, the most that can be contributed for the year to the spousal IRA is the smaller of the following amounts: • $5,000 ($6,000 if age 50 or older), or • The total compensation includible in the gross income of both spouses for the year reduced by all of the following: Traditional IRA contributions for the spouse with the greater compensation, and • Any contribution for the year to a Roth IRA for the spouse with the greater compensation • In other words, as long as they file a joint return, married taxpayers' combined IRA contributions cannot exceed their combined compensation, and neither spouse can contribute more than $5,000 (or $6,000 for 50 and older) to their own IRA.

Links and Helpful Tips • For more information on all types of IRAs, refer to the Individual Retirement Arrangements (IRAs) chapter in Publication 17 and Publication 590, Individual Retirement Arrangements. • See Publication 17 for more information on compensation. • To determine the traditional IRA deduction amount for taxpayers covered by an employer's retirement plan, refer to the traditional IRA deduction phaseout charts in the Adjustment section of the Volunteer Resource Guide (Tab E), • Enter the total contributions to traditional IRAs that were made (or will be made) for each spouse (on a joint return) by April 17, 2012. The deduction is reported on line 32 of Form 1040 • TABLE FOR PHASEOUT: http://apps.irs.gov/app/vita/content/17/17_05_105pop.jsp • TABLES FOR MAGI: http://apps.irs.gov/app/vita/content/17/17_05_065pop.jsp • Turn to the Volunteer Resource Guide (Tab 3) for more information about the IRA Deduction Worksheet. • Review the charts on the Effect of Modified AGI on Traditional IRA Deduction in Pub 4012 (Tab E) • • Link from Form 1040, line 32 to an IRA Worksheet to type any IRA contributions

Student Loan Interest • Interest paid on a student loan for qualified higher education expenses that were: • For the taxpayer, the taxpayer’s spouse (if MFJ) or a person who was the taxpayer’s dependent when the loan was obtained • Paid within a reasonable period • For an eligible student, An eligible student is one enrolled in and carrying at least one-half the normal load for a qualified program. The standard for what is half the normal full-time work load is determined by each eligible educational institution • An eligible program may include study abroad that is approved for credit by the institution where the student is enrolled. • A student loan interest deduction is generally the smaller of $2,500 or the interest paid that year on a qualified student loan.

Guidelines to Follow • Taxpayers cannot deduct as interest on a student loan any amount that is an allowable deduction under any other provision of the tax law (e.g., as home mortgage interest) this is a double deduction • This amount is gradually reduced (phased out) or eliminated, based on the taxpayer's filing status and MAGI.: Effect of MAGI on Student Loan Interest Deduction in the Adjustment section of the Volunteer Resource Guide (Tab E). • To qualify, a student loan: • Must be solely to pay qualified education expenses, and • Cannot be from a related person or made under a qualified employer plan

Reductions to Student Loan Interest • Before calculating qualified expenses on a tax return, the following tax-free income amounts must be subtracted: • Employer-provided educational assistance benefits • Tax-free withdrawals from a Coverdell ESA or from a qualified tuition program • U.S. savings bond interest excluded from income because it is used to pay qualified higher education expenses • Certain scholarships and fellowships • Veteran's educational assistance benefits • Any other nontaxable payments (other than gifts, bequests, or inheritances) received for educational expenses

Student Loan Interest • To claim the deduction, the taxpayer must have paid qualified student loan interest for an eligible student under all the following conditions: • The taxpayer cannot use Married Filing Separately status; married taxpayers must file a joint return with their spouse • The taxpayer cannot be claimed as a dependent on someone else's return • The taxpayer is legally obligated to pay interest on a qualified student loan • The taxpayer paid interest on a qualified student loan • The interest is on a loan used to pay tuition and other qualified higher education expenses for the taxpayer, the taxpayer's spouse, or someone whom the taxpayer claimed as a dependent, when the loan was taken out • The education expenses were paid or incurred within a reasonable period of time before or after the loan was taken out • The person for whom the expenses were paid or incurred was an eligible student

Where to Look • Line 33 on the 1040 • Form 1098, Box 1 • In case you need to verify if an institution is valid but they should have form 1098 with them: http://ope.ed.gov/accreditation/ • See Publication 970, Tax Benefits for Education, for more information on the student loan interest deduction.

Tuition and Fees Deduction • Can deduct up to 4,000 in qualified tuition and related expenses • If you claim this deduction you cannot claim the education tax credits (American Opportunity Credit or Lifetime Learning Credits) work with the client to figure out the best benefit • Rule: The amount of the deduction is determined by the taxpayer's filing status, MAGI, and other factors.

Tuition and Fees Deduction-Guidelines • The deduction can be claimed for the taxpayer, the taxpayer's spouse (if filing a joint return), and any dependent (for whom the taxpayer claims a dependency exemption) who attended an eligible educational institution during the tax year. • In order to claim a deduction for expenses paid for a dependent who is the eligible student, the taxpayer must have paid the qualified expenses and claim an exemption for the dependent. If students are eligible to be claimed as a dependent (even if not actually claimed) and paid their own expenses, no one can take the adjustment. However, students who do not qualify as a dependent can claim the deduction, even if tuition and fees were paid by someone else. In that case, the students can treat the amounts paid for tuition and fees as a gift.

Tuition and Fees Deduction-Guidelines • The deduction cannot be claimed by married taxpayers who file separately or by an individual who is claimed as a dependent on another taxpayer’s return. • The taxpayer must have paid for the qualified expenses for the dependent. • Qualified education expenses do not include payments for: • Insurance, room and board, medical expenses (including health fees), transportation, or similar personal, living, or family expenses • Course-related books, supplies, nonacademic activities and equipment unless it is paid as a condition of enrollment or attendance • Any course or other education involving sports, games, hobbies, and noncredit courses unless the course or other education is part of the student's degree program

Where to Look/Tips • To help you figure the tuition and fees deduction, the taxpayer should have received Form 1098-T, Tuition Statement. Generally, an eligible education institution must send Form 1098-T or a substitute to each enrolled student by January 31. However, the form only reports "amount billed" or "payments received." • Form 8917, Tuition and Fees Deduction, will help you compute the taxpayer's Modified AGI for this deduction. The tax software will complete this part of Form 8917 automatically.

Out of Scope • Out of Scope Situations for VITA/TCE • The following are out of scope for this lesson. While this list may not be all inclusive, it is provided for your awareness only. • Other adjustments to income on Form 1040, such as: • Self-employed health insurance deduction • Self-employed SEP, SIMPLE, and qualified plans • Domestic production activities deduction • Form 8606, Nondeductible IRAs