Download

1 / 17

170 likes | 352 Views

Actuarial Present Value and Sensitivity Analysis. What does an Actuary do?. Areas of Actuarial Work. Life Insurance Property and Casualty Insurance (P&C) Health Insurance Pension Consulting. Life Insurance. Life companies principally serve two functions

E N D

Areas of Actuarial Work • Life Insurance • Property and Casualty Insurance (P&C) • Health Insurance • Pension • Consulting

Life Insurance • Life companies principally serve two functions • to insure against financial loss in result of death • to save and invest money for retirement • Less exposed to risk than P&C companies • Invested in longer term assets

Types of Products • Term Life, Whole Life, Universal and Variable Universal • Fixed, Deferred, and Variable Annuities • Asset Management, Mutual Funds

Why do companies use life tables? • To help predict the amount that will be paid out in claims (known as liabilities) • Example: • Tom, aged 22, buys a one year, $250,000 term policy • Expected claims equals total amount at risk times the probability of claim • Expected claims = $250,000*0.000987=$246.75 • Note that $246.75 is the average amount of claims expected by the insurance company • Actual claims may differ substantially

The Collective Risk Pool • The basis of insurance • A large number of people buy an insurance product • Only some of them will be affected – The risk is shared among the group • The company is able to predict total claim amounts of the entire risk pool accurately

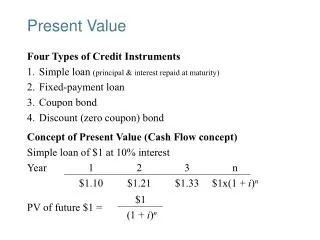

The Time Value of Money • A dollar today is worth more than a dollar one year from now • At 7 % interest, $1.00 becomes $1.07 one year from now, but $1 received one year from now is worth: $1.00/1.07=$0.93 • PV = FV/ (1+i)^t

Whole Life Example • Suppose Tom, aged 22, buys a $250,000 whole life policy. • His expected number of years left is 56.5 • That means on average, the company will pay out $250,000 in 56.5 years. • PV = FV/ (1+i)^t • The present value of this liability is thus: • $250,000/(1.07)^(56.5)=$5,467.09

Limitations of these examples • The probabilities I used were taken from data representing ALL of the U. S. population • Mortality rates are known to differ according to certain socioeconomic, demographic, gender, and health factors • Companies must draw up their own life tables based on their own customer base • The actual modeling process of these life policies is much more complex than indicated

Where does the Actuary come in all of this? • I worked in an area of the company known as Corporate Actuarial • Statutory income statements and balance sheets

Actuarial Present Value • 3 basic components of valuing an insurance policy • Expected present value of premiums (known as assets) • Expected claims (liabilities) • Cost of selling the contract by insurance salesmen (called “financial representatives”) • Total Value=Expected value of assets – Expected value of liabilities – acquisition costs

My First Project: Sensitivity Analysis • The value of a contract changes over time • PV = FV/ (1+i)^t • Assumptions that can change the value of an insurance contract • Mortality Rates: causes change in present value of liabilities due to when claims are paid out • Interest Rates: causes change in how much future dollars are worth – generally affects assets more, but not always • Managing interest rate risk is known as duration analysis

Sensitivities to be tested: • Mortality/Morbidity: Mortality/Morbidity rates were scaled up and down by 10% in the ALFA model • Interest/Discount rates: Up and down 1% from 7% • Equity Rate: Increased/Decreased rates premiums grew at up and down 1% • Lapse/Termination rates: Up and down by10% • Rates chosen to provide input for an upcoming audit of the firm’s financial statements

Appendix • Bellis, Claire et al., Understanding Actuarial Management: The Actuarial Control Cycle • Black, Kenneth Jr. and Harold Skipper Jr., Life Insurance • Easton, Albert E. and Timothy F. Harris, Actuarial Aspects of Individual Life Insurance and Annuity Contracts • Hull, John C., Options, Futures, and Other Derivatives

Conclusion • Thanks for coming • Any Questions?