Download

1 / 17

E N D

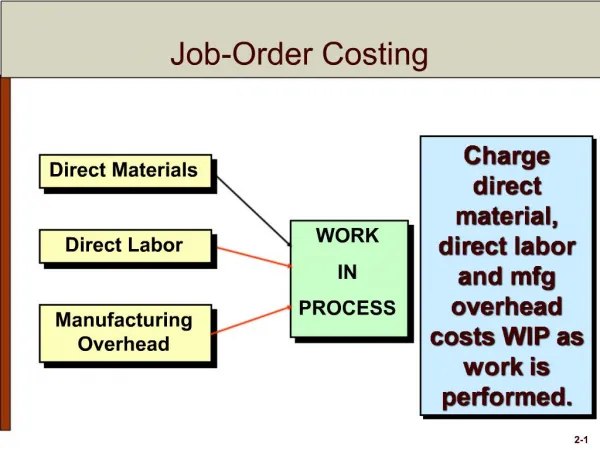

Job Order Costing Job Order Costing Job order costing assigns costs to each job. A job can be an order, a contract or a unit of production. e.g. If we want to accumulate the cost of repair of a machine this is done by collecting the cost of parts, direct labor and overhead costs (applied by using an overhead rate).

Therefore job order accounting system is a product system used in making one-of –a-kind or special order products. In such system direct materials, direct labor and overhead costs are assigned to specific jobs . In computing unit costs the total manufacturing costs for each job order are divided by the number of units produced for that order.

Accordingly Job order costing characteristics • 1. Collect manufacturing costs • 2. Measure costs of completed jobs • 3. Has ONE work in process account for all unfinished jobs

Accounting for material in job order system • Materials if they form an identifiable part of the end product they are classified as direct materials and if they are used in the manufacturing process; they are classified as indirect. Once material are there a material requisition form is made to record the material flow.

This is the basic source of document informing the cost accounting department that materials have been issued. (Internal control) other documents include material purchase request, purchase orders and receiving reports.

Material requisitions facilitate assigning the cost to a job or a department. • This source document allows for the transfer costs from direct materials inventory to work in process inventory.

Labor Accounting in job order costing • Accurate and understandable methods for calculating payroll are necessary because no other area in accounting has more impact on the morale of employees than their wages or benefit policies.

Labor systems • Wages are hourly or piece-rate payment and they are variable costs. • Salaries are fixed periodic payments such as weekly or monthly payments. If tax is withheld then it has to appear in the books.

Labor related costs • These include bonuses, vacation pay, free uniform and hospitalization insurance. Cost accountants account for these costs by job or department. To account for all costs we need timekeeping records. These include

Timecard or clock card: this show the time each employee arrives and leaves. It provides evidence of when the employee was on the work site. • Date Time • 1/1 8:00 • 1/1 3:00

Job time ticket: as time cards indicate the total time worked companies needed an indicator of the time spent on each job during the day. A job time ticket shows where an employee worked during the day, the time he started and the time he stopped and the rate of pay. • Date Employee name • Time started Job No. • Time Stopped Department • Hours worked Pieces completed • Rate Amount

Daily time ticket: this summarizes all the jobs performed during the day. This form shows where an employee worked during the day, the time he started and the time he stopped. • Date Employee name Started Stopped Hours Job No. Department • Total Hours worked • Regular Overtime

Factory overhead Accounting • Because factory overhead for are linked to certain products they are debited to a factory overhead control account. They are accounted for by the techniques discussed earlier.

Example • ABC company had following operations for the month of November. • Material requisition and factory labor used • Materials Labor • Job1 2340 1090 • Job 2 3390 1990 • Job 3 2980 1440 • Job 4 4765 2890 • Job 5 2240 940 • Job 6 1940 1090 • For general factory use 515 690

2. Factory overhead is applied at 60% of direct labor cost. • 3. Jobs completed no. 1, 2, 4, and 5 • 4. Jobs no. 1, 2, and 4 were shipped and costumers were billed $ 5690, $ 9490, and $ 13290 • Required • calculate the cost of finished jobs • calculate the cost of jobs sold

Solution • 1. Cost of finished jobs • Job D.M D.L O. head Total • 1 $2340 $1090 $654 $4084 • 2 3390 1990 1194 6574 • 4 4765 2890 1734 9389 • 5 2240 940 564 3744 Total 23791

2. Cost of jobs sold • job 1 $4084 • job 2 6574 • job 4 9389 • $20047