Download

1 / 20

200 likes | 202 Views

This presentation provides an analysis of key macroeconomic indicators in South Africa, including the recent developments in the economy. It explores the implications for fiscal policy and discusses the risks and challenges faced by the country.

E N D

Select Committee on Finance Sector Analysis 09 July 2019 Content Adviser: Esther Mohube

Structure of the presentation Sector analysis • Global economic outlook • Key macroeconomic indicators in South Africa • Latest developments in the SA economy • Key fiscal trends • What are the Implications for fiscal policy? • The Committee’s fiscal oversight role • Conclusion

Global economic developments (2) Key messages: • The global economy has recovered from the 2008/09 recession & its forecast to continue growing positively over the medium term. • IMFexpects world GDP to grow by 3.6 % over the medium term. Driven by ongoing buildup of policy stimulus in China, recent improvements in global financial market sentiment& gradual stabilization of conditions in stressed emerging market economies. • Growth in the BRICs countries projected to be faster at 4.9 %, led by China and India. • In SSA, growth will average 4% in 2023, up from 3.5 % in 2019. Growth affected by commodity prices outlook, exposure to weather conditions & level of economic development. • SA has not been performing well since the recession, GDP expected to average 2.4% in 2023 due to continued policy uncertainty and structural challenges.

Key macroeconomic indicators in SA (2) Key highlights: Before and after the recession • Economic environment has deteriorated steadily since recession • GDP growth averaged 4.76 % during the economic upturn. After the recession in 2008/09, economic growth remained subdued registering 2.04 % and 1.32 %, respectively. • In 2018, the SA economy grew at 0.7 %, expected to improve moderately to 1.5 % in 2019 & 2.1% in 2021 (February 2019 Budget Review). Global economy not supportive of growth; slow recovery in employment & investment and confidence • NT expects gradual improvement in confidence; effective public infrastructure spending to drive GDP growth over the medium term; • Identified risks to the outlook, failure to fully reconfigure ESKOM • GDFI & exports continued to grow, albeit at a constant rate. Headline CPI remained within the target range for most of the time, while the number of people employed increased steadily from 12 to 15 million. • Social grants reduced no. of people living below lower bound poverty levels from 51% to 40%. • Persistently higher rates of unemployment and inequality remain • Over the last 10 years, measured above 24 per cent, on average. In Q1 2019, measured 27.6 %. • SA remains one of most unequal societies in the world, with Gini coefficient measuring 0.69

Latest developments in the SA economy (1) South African economy contracted by 3.2 % in Q1 of 2019 • Compared to 1.4 increase in Q4 of 2018. Key negative contributors are mining (-10.8 %) & manufacturing (-8.8 %) contributed and trade (-3.5 %). Electricity supply constraints & protracted strike in a major gold mine contributed to a weak first quarter performance(StatsSA). • Business & consumer confidence continued to weigh on the near-term growth forecast. • On 23 May 2019, SARB revised down growth forecasts to 1.0 % in 2019, while forecast for 2020 & 2021 is unchanged at 1.8% and 2.0%, respectively. Weak business confidence, possible electricity supply constraints & high debt levels in certain state-owned enterprises will continue to limit investment prospects. Real fixed investment is now forecast to contract by 0.3% in 2019 • Moody’srevised GDP growth forecast to 1.0 % in May 2019, down from 1.3%, previously • National Treasury likely to also revise growth forecasts downwards in October 2019 MTBPS • SA’s growth outlook is dependent on the pace of implementation of structural reforms such as strengthening governance, encouraging competition, increasing labour market flexibility and reducing the cost of doing business (IMF, May 2019).

Latest developments in the SA economy (2) Rate of unemployment remain persistently high at 27.6 % • Increased from 27.1 % in Q4 2018 • Provincially, WC (19.1 %) and LP (19.7 %) have lowest rates, while EC (35.6%), FS (32.8 %) and MP (32.4 %) have the highest rates • Rate is relatively higher for women, youth, less than matric • No. of employed people decreased from 16.529 million to 16.378 million in Q1 of 2019 Inflation targeting framework continues • SARB kept the repo rate unchanged at 6.75 % in May 2019 • Headline CPI expected to remain within the 3-6 % target rage, averaging 4.5 % in 2019, 5.2% in 2020 & 4.6 % in 2021. Inflation expectations appear to be well anchored over the medium term What does that mean for the fiscal framework? • Identified economic & fiscal outlook risks likely to materialise • Other implications on fiscal indicators (higher debt level, wider budget deficit, increased government expenditure, revenue collection shortfalls • Possible further sovereign credit rating downgrades

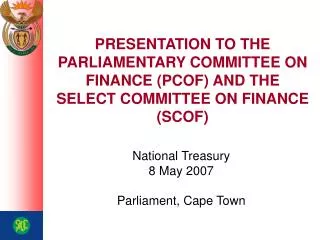

Key fiscal trends between 2001 and 2019 (2) Key highlights: Fiscal framework indicators • Domestic GDP growth expected to remain below 2% over the medium term. • Total government revenue continued to increase despite the recession, averaging 28.7 % of GDP in the last five years ending 2017/18. • Total government expenditure also increased proportionally from 26.5% during the economic boom to 32.5 % in the last five years. Similar pattern expected over the medium term. • The budget deficit widened significantly in 2009 (-6.5 % of GDP), recovered to 3.8%, on average. • Gross loan debt as a % of GDP increased from 31.3 % to 48.7 % in five years ending 2017/18 & projected to reach 55.5% over the 2019 medium term.

Actual net debt level against forecasts between 2001 and 2018

Fiscal policy developments Key Messages: • Poorly performing economic growth does not bode well for fiscal policy. Possible recession? • South Africa’s fiscal deficit is set to worsen primarily due to South Africa’s growth outlook, which will put additional pressure on debt levels. • Very tight fiscal space, leaving limited room to absorb shocks in case of unforeseen circumstances. • Continuously escalating debt levels, with higher interest rates crowding out service delivery, and creating a wider budget deficit. • Likelihood of revenue shortfalls (cut expenditure? Increase taxes?), tough balancing act required. • Possible credit rating downgrades and implications thereof on interest rates. Fitch Ratings and S&P Global downgraded SA's credit rating to sub-investment grade, or junk, in 2017. Moody’s might follow suite in November 2019. • A major risk to South Africa’s growth is the weak finances and operations of state owned enterprises, especially Eskom (IMF May 2019).

The Committee’s fiscal oversight role Some institutional arrangements: Measures to facilitate fiscal oversight and improve governance across the three spheres of government • Budget structures, reforms, legislation, Chapter 9 institutions (e.g. AGSA, FFC) • Continuous assessment of AGSA reports (provinces, LG & public entities) • PFMAintroduced in 1999, to improve financial management in the public sector. • In 2003, the MFMA was introduced to “ensure sound and sustainable management of the financial affairs of municipalities and other institutions in the local sphere of government”. • In 2009, the “Money Bills Act”was introduced, to give effect to Section 77 of the Constitution. The Act saw an establishment of the Committees on Finance and Appropriations and the Parliamentary Budget Office. • In 2018, Public Audit Bill was amended, given evident lack of compliance with financial management laws; a disregard for audit recommendations; a continuing rise of unauthorised, irregular, fruitless and wasteful expenditure and a need to restore prudent financial management (AGSA) • Financial management has improved over time, Committee need to ensure efficiency, effectiveness and value for money in service delivery. • Committee ensure compliance with this legislation and improve good governance, consequences for financial misconduct.

Conclusion • The Committee should: • Note the deteriorating economic environment and the impact this has on the national fiscus. • Note the tighter fiscal space and vulnerability of SA to external shocks. • Strengthen its fiscal oversight role over provinces, municipalities and their respective public entities. • Improve implementation of the Money Bills Act • More details are in the Legacy report.