Download

1 / 49

560 likes | 802 Views

Locational Marginal Pricing and Financial Transmission Rights. DAM Working Group October 30, 2003 DRAFT - For Discussion Purposes Only. Overview and Summary. IMO Market Enhancements: What’s Missing?.

E N D

Locational Marginal Pricing and Financial Transmission Rights DAM Working Group October 30, 2003 DRAFT - For Discussion Purposes Only 1

IMO Market Enhancements: What’s Missing? • The IMO has undertaken several initiatives to enhance the IMO-administered markets, including: • Improvements in the dispatch, such as multi-interval optimization and better use of operating reserves • Enhanced demand-side initiatives • A day-ahead market for energy and operating reserves • A possible long-term resource adequacy mechanism • In theory, each of these enhancements is worthwhile, and if designed well, should produce benefits. But all of them will work much better if they are premised on efficient pricing in IMO markets. There’s a missing piece. 3

IMO Market Enhancements: What’s Missing? • Efficient spot market pricing includes both: • Improved spot pricing of energy and op.res. to reflect scarcity and • Using locational marginal pricing (LMP) to price congestion. • Together, these pricing improvements would significantly improve both system reliability and the performance of Ontario’s markets. • And efficient pricing with LMP will support and improve the other enhancements IMO is pursuing. • Equally important, without LMP, some of the enhancements will work poorly, and in the case of the day-ahead market, may not be worth doing. 4

This Presentation Will Explain How LMP Would Provide Benefits to Ontario Markets • LMP would improve real-time reliability. • LMP prices encourage generators to follow dispatch instructions. • LMP would fully support a DAM with reliability unit commitment. • LMP eliminates the gaming/incentive problems of uniform pricing. • LMP eliminates the need for constrained-on/off payments (CMSC). • And thus eliminates the bidding games driven by CMSC and uniform pricing. • LMP would fully support long-run resource adequacy. • It improves locational price signals about where (and where not) to build. • And can improve price signals about where (and where not) to conserve. • LMP would help solve the transmission investment problem. • LMP with financial property rights encourages economic grid upgrades. • An LMP-based Ontario market would mesh better with other LMP regions. 5

Common LMP Concerns, Issues, Solutions • Is LMP more complex than uniform pricing? • No. Experience has shown that problems with uniform pricing require an increasingly complex and non-transparent set of non-market fixes, none of which solves the underlying incentive problems. • Once the LMP mechanism is in place, it is simpler for the ISO. Market participants find it workable and transparent. • Does LMP require that loads all pay different prices? • No. Generators and dispatchable (or price-sensitive) loads would be settled at their respective LMPs. • But most loads could be settled at averages of LMP – the “average” could extend to the Province or any sub-region. • Will LMP automatically raise total prices over what they should be? • No. LMP reveals the marginal cost of serving load at each location. • This is the price needed to sustain adequacy at each location. • If current uniform pricing system does not reveal that, then resulting system is not sustainable and will eventually require subsidies. 6

Ontario’s Initial Decision to Wait On LMP • In 1998, the Ontario Market Design Committee recommended that the market begin with uniform pricing and consider LMP or zonal pricing later. There seemed legitimate reasons for this choice. • Some MDC members did not support LMP (e.g., Enron). • The Ministry was adamant about having a single Ontario price. • There was little experience with LMP in the US (PJM = April 1998) • To many, LMP seemed an unproven and complex concept. • Since 1999, the debate over LMP has been largely resolved. • Several years of experience have shown it works and is simpler. • LMP has been highly successful in PJM, New York, New England • Regions that started with something else are all moving to LMP – California (from zonal) and ERCOT (from zonal) • Regions that are just starting are choosing LMP – MISO, SeTrans • The debate at FERC is over: SMD is based on LMP. • All of these regions solved the “single price for loads” issue. 7

Threshold Issues All Support Each Other • A market works well if all the pieces are in place and all are designed to work together. Ontario faces several challenges: • It would help to solve the supply competition/market power issue. • A single dominant supplier will discourage 3rd party investments. • And government support for that supplier will exacerbate this. • Consumers would benefit by solving the “missing buyer” problem. • Creating LSEs to buy for default consumers could provide stable prices against spot market volatility and contracts for suppliers. • And active buyer LSEs would make the DAM work much better. • The market would perform much better with active demand side. • More price-responsive loads would limit and define scarcity prices (and let spot prices reflect scarcity) and mitigate market power. • Charging larger loads real-time LMP prices would encourage this. 8

Problems With Uniform Pricing in a DAM Highlight the Benefits of Moving to LMP • The recent draft “strawman” for a proposed day-ahead market (DAM) concludes that Ontario should not implement an IMO-administered DAM if Ontario continues to use uniform pricing. • Uniform pricing in a DAM would simply create too many problems. • All of the incentive problems that Ontario now experiences from using uniform pricing in its real-time markets (RTM) would be exacerbated when carried over into a DAM. • And it is not even clear that a sophisticated DAM with uniform pricing would be workable. 10

Problems With Uniform Pricing in a DAM • The continued use of uniform pricing in a DAM would simply create too many problems, including: • More side payments -- the requirement for constrained-on/off side payments to manage congestion would carry over into the DAM. • Complexity -- the interaction between DAM and RTM settlements would create substantial increased complexity. It would be: • Confusing, given likely deviations between DAM and RTM results. • Non-transparent, given the complexity of CMSC payments. • Probably a large opportunity for strategic bidding and market manipulation between the DAM and RTM (“gaming”). • A continuing source of concern for the Market Surveillance Panel. • Lack of convergence -- there would be no guarantee that the incentives from uniform pricing and CMSC side payments would allow the DAM and RTM to converge to consistent results. 11

Using LMP Would Solve These Problems • The DAM WG also examined DAM and RTM settlements using locational marginal pricing (LMP). • Nodal settlements for generators; aggregate settlements for most loads. • All of the problems associated with the use of uniform pricing in the DAM and RTM disappear with LMP. • Nodal pricing eliminates the need for CMSC side payments. • All the gaming incentives/opportunities created by CMSC disappear. • And the DAM would function better: • Simpler to administer settlements and monitor outcome/behavior. • More transparent and intuitive prices. • Consistent results with the RTM, making the DAM prices more useful references for other forward markets. 12

Characteristics of an LMP System • Nodal prices are consistent with a reliable dispatch. • Price signals to generators are consistent with what the system operator needs generators to do to relieve congestion and balance the system. • Nodal prices are consistent with an economically efficient dispatch. • The LMPs are derived from the system operator’s economic dispatch. • The LMP price at each node reflects the least-cost redispatch that would be needed to serve an increment of load at each location. • Nodal prices are consistent with the participants’ offers and bids. • The nodal prices make intuitive sense to MPs, given their offers or bids. • Settlements based on nodal prices are free of cross-subsidies. • Each MP is paid/charged the marginal costs/benefits of its transaction. • Nodal pricing allows total flexibility between spot and bilateral trading. 13

How Are LMP Prices Defined? • Under LMP, the price of spot energy at each location is defined as the incremental cost in the dispatch of serving another increment (1MW) of load at that location . . . • Given the actual dispatch arranged by the system operator; • Given the actual constraints (and contingencies) binding in that dispatch; • Given the offers/bids submitted by the participants for that dispatch. • After the dispatch schedules are arranged/implemented: • In the DAM, LMP prices are calculated for each hourly interval. • In the RTM, LMP prices are calculated for each five-minute dispatch interval. 14

How Are Participants Settled Under LMP? • Once the LMP prices are calculated for each node, settlements are then based on the nodal LMP prices: • Each generator is credited for its injections at the LMP for its location; • Each load is debited for its withdrawals at the LMP price for its location; • Nodal prices can be aggregated/averaged to get a “uniform” price. • Each transmission customer (bilateral) is charged for transmission use at the opportunity cost, defined as the difference between the LMP price at the withdrawal location and the LMP price at the injection location. Transmission Usage Charge = LMPB – LMPA Note: There would continue to be a transmission access fee to recover the fixed costs of the grid, as today. 15

Using LMP to Create a “Uniform Price” • Mathematically, prices from any group of LMP locations can be aggregated to create an average LMP for that group of locations. • So a settlement “location” need not be a single node; it may be a “location” defined as the aggregate of many nodes (or a“hub”). • If Ontario were treated as (e.g.) four load regions or zones, an average LMP load price for each zone would be the load-weighted average of all the LMP prices for each node in that zone. Prices might differ between zones, but loads within a zone would pay the same price. • If Ontario were treated as a single load zone, an average (“uniform”) LMP price for the province would be the load-weighted average of all the LMP prices for every node in the province. 16

LMP Settlement Systems Are Flexible • The flexibility in defining settlement “locations” for nodal pricing would allow Ontario to continue the current policy of having a single “uniform” price apply to all or most loads in the Province. • At a minimum, Ontario would settle all generators at their respective nodal prices. Dispatchable loads would also settle at their respective nodal prices. • This avoids CMSC payments and associated gaming incentives. • It encourages those participating in the dispatch to follow this dispatch. • But Ontario could settle most/all other loads at a single uniform price -- the load-weighted average of the nodal prices across the province. (Any averaging would result in some inefficiency.) 17

LMP Settlements and “Congestion Rents” • LMP recognizes that pricing congestion correctly will produce a settlement surplus, reflecting the marginal cost of congestion. • The Sum of all payments made to all generators at their respective locational prices will be less than . . . • The Sum of all payments made by all loads at their respective locational prices. • The difference between these two sums (ignoring losses) is the “congestion rent” and reflects the marginal cost of redispatching the system to relieve all constraints. • In LMP systems, this congestion rent, or settlement surplus, is used to fund financial transmission rights (FTRs). (It’s not kept by IMO.) 18

The Role of Financial Transmission Rights • FTRs serve several useful functions in an LMP market. • They provide hedges against congestion charges (LMP congestion price differences between generators and load locations). • This allows parties to lock in the delivered price of energy at any location, even though congestion causes locational prices to differ. • FTRs are a means of returning to loads (or whoever holds the FTRs) the congestion rents portion of the settlement surplus collected in the IMO spot markets. • And FTRs serve as property rights and provide forward price signals that can support market-driven investments in transmission expansions. 20

FTRs As LMP Congestion Hedges • FTRs entitle the holder to a portion of the settlement surplus. • The FTR holder receives the difference in congestion charges between two locations defined by the FTR. • If an FTR is defined from location A to location B, then . . . • The holder receives the difference between the LMP at B and the LMP at A. (More accurately, the difference in the congestion component of the LMPs at locations B and A) • So an FTR between two locations can hedge (rebate the cost of) the congestion charge between those same two locations. • Congestion charge = LMPB – LMPA • FTR rebate = LMPB – LMPA 21

FTR Allocations, Revenue Adequacy and the Settlement Surplus • ISOs that allocate (or auction) FTRs limit the number of FTRs they allocate (or auction) to match the expected transmission capacity of the grid. This is called a “simultaneous feasibility test” or SFT. • There are many combinations of FTRs that can meet this criterion. • If the set of allocated FTRs meets this test, then that set is also “revenue adequate.” • This means that absent loss of grid capacity, the ISO will collect in congestion rents (the settlement surplus) enough revenues to fully fund the payments to FTRs holders, even if the dispatch for a given settlement period is different from the one corresponding to the FTR allocation. 22

FTR Payments and Load Settlements • FTRs would allow loads paying LMP prices to recover the congestion rent portion of the difference between the aggregate prices they paid under LMP and the aggregate prices paid to the generators that served them. • Thus, it’s always important in comparing the final prices paid by loads under uniform pricing and LMP to remember that the FTRs payments will lower the net price paid by loads in an LMP system. Looking at the nodal prices alone is always misleading. 23

The Merits of Locational Marginal Pricing Transcend the Issue of a Day Ahead Market • The arguments for moving away from uniform pricing (and moving to LMP) also apply without a DAM. LMP would: • Improve the IMO’s real-time dispatch and thus better support reliable operations . . . • Even if the IMO only administers a real-time market. • And it would easily support adding a DAM with unit commitment, which would also improve IMO real-time reliability. • Provide better incentives for generation investments. • Provide better incentives for demand-side actions and investments. • Provide better support for any long-term resource adequacy mechanism. • Provide essential incentives for economic transmission expansions. 24

Viewing Resource Adequacy As A Whole • The LTRA “Strawman” argues that an effective, robust resource adequacy mechanism is not merely a device for requiring additional generating capacity. A more complete approach also includes: • Efficient spot price signals to both buyers and sellers. • Sufficient buyers actively engaged in the market that: • Provide a market/counter-parties for contracts with suppliers • Provide adequate contract hedges for consumers against spot price volatility. • Sufficient price-responsive demand to define shortage prices, limit price spikes to mitigate market power and avoid involuntary curtailments. • A foundation for meeting locational requirements for new capacity. • A structure that supports adequate/appropriate grid investments. 26

LMP Produces Efficient Spot Prices • Nodal pricing (LMP) uses market-clearing prices defined by marginal costs (as defined by offers/bids): • It prices the effects of congestion and losses, using marginal costs. The nodal price is the incremental cost of serving an increment of load at each location. • It defines spot energy prices at each location. Spot purchases and sales (or imbalances) are settled at the nodal spot prices without subsidies. • So LMP sends the correct locational price signals to suppliers and consumers about incremental changes in supply or consumption. • Nodal price differences define spot transmission prices. Parties pay for their transmission usage at the opportunity cost of that usage. • So grid users face the correct price signals about the costs of their usage. • Nodal pricing efficiently allocates use of the grid. Grid use is allocated based on parties’ willingness to pay the marginal redispatch costs for their transactions. 27

LMP Spot Prices Are the Foundation for Contracts • In general, forward prices, including those in term contracts, tend to reflect expected future spot prices. • If spot prices are defined efficiently by LMP, then forward/contract prices will also be efficient. • Parties have incentives to contract to achieve price certainty and to allocate risks for spot price volatility and congestion. • LMP-based contracts with FTRs provide a means to hedge against and allocate the risks of congestion costs. 28

LMP Provides Correct Incentives for Price-Responsive Demand • The current uniform pricing system sends incorrect price signals about the value of demand-side responses at different locations. • Of course, using a nodal aggregation to define a uniform price would continue this problem. • LMP could partly fix this problem for those loads likely to be active participants in the market, provided that nodal prices are used to settle the imbalances/spot purchases made by those participants. • Dispatchable loads • Other price-sensitive loads with appropriate meters • LSEs responsible for meeting their customers’ loads • If faced with nodal prices for their “imbalances,” they would have incentives to encourage/incent those customers at high price locations to undertake efficient demand-side responses. 29

LMP Provides the Correct Incentives for Generator Investment/Siting Decisions • LMP efficiently prices the effects of congestion and losses on the value of energy and operating reserves at each location. • LMP prices will tend to be higher and more profitable, and thus encourage investment, at locations where new entry will tend to reduce congestion and/or losses. • LMP prices will tend to be lower and less profitable, and thus discourage investment, at locations where new entry would tend to increase congestion and/or losses. • Without LMP, the region would need additional (and locationally different) incentives/penalties to encourage appropriate siting decisions and/or administrative restrictions on those decisions. 30

LMP Is the Foundation for A Locational RAR • An explicit Resource Adequacy Requirement (RAR) should pay resources for providing installed (or operating) reserves at prices that make up the “missing revenues” when energy/or prices are capped below competitive levels. • Any RAR mechanism has to account for locational factors – the grid constraints that limit the ability of some generators to deliver their capacity to loads, to provide the desired level of reliability. • To provide the right level of “missing revenues,” an effective RAR mechanism should be based on a set of energy/OR prices that are already as efficient as possible in reflecting grid constraints. • LMP provides the right foundation. 31

LMP/FTRs Will Encourage Grid Upgrades • Grid users faced with LMP differences and FTR forward prices will have incentives to fund economic upgrades to the grid. • Market-driven grid investments (as in PJM/NY) occur when all of the following are in place: • LMP settlements for generators and market-active loads • Forward prices for FTRs to define the value of relieving congestion • Rules that award the incremental FTRs to those who fund the upgrades. • Regulatory rules that allocate grid upgrade costs to beneficiaries. • A regulatory backstop (for market failure) that goes last, not first. 32

If Not LMP, Then What? • Each of the alternatives to nodal pricing has been tried in various forms in the US and found to be fundamentally flawed. • Uniform pricing has been tried and abandoned in favor of nodal: • In PJM – from April 1997 to April 1998 • In New England – from 2000 until March 2003 • Zonal pricing has been tried and is being replaced by nodal: • In California – by late 2004? • In ERCOT (Texas) – by 2005? • Nodal pricing has been successful everywhere it’s been tried: • In PJM (1998), New York (1999) and New England (2003); NZ (1996) • And endorsed for other emerging market regions: SeTrans, MISO 34

The Fundamental Flaw in Uniform Pricing • Uniform pricing does not accurately reflect the value of congestion and losses. The resulting prices send the wrong price signals, and these perverse signals inescapably lead to serious problems: • Problems in the dispatch and thus risks for reliability. • Poor locational signals for generation investments. • Even worse locational signals for demand-side investments and actions. • And virtually no signals to encourage appropriate grid investments. 35

Uniform Prices Alone Can’t Support a Reliable Dispatch • In the presence of congestion, paying all generators the same price is inconsistent with their offer prices. • To relieve congestion, the IMO must constrain off/down energy from units at some locations, even though their offer prices are lower than the uniform price. • The higher uniform price is a strong incentive to run (self-schedule) anyway so as to be paid the uniform price. • To balance the system the IMO must constrain on/up energy from units at other locations, even though their offer prices are higher than the uniform price. • Accepting the uniform price would force them to operate at a loss. 36

Uniform Pricing Alone Can’t Support a Reliable Dispatch (Cont.) • Without further side payments in addition to or in lieu of the uniform price, generators would not follow the system operator’s dispatch instructions. • So reliability would be at risk. • PJM demonstrated this in 1997, when the system almost collapsed from companies that self scheduled units that needed to be constrained off. • Without constrained-off payments, PJM almost lost control of its dispatch. • Ontario could face the same problem if it did not have de facto regulatory restrictions on or monitoring of generator behavior. This is not a market solution. 37

Can Side Payments “Fix” Uniform Pricing? • Side payments can be used to offset the perverse incentives not to follow the dispatch. • The IMO can pay constrained-off units their opportunity cost. • The IMO can pay constrained-on units their offer prices. • But these side payments are inherently subject to strategic bidding (games). • The games are predictable and were predicted. • The games are/were prominent features of the California and ERCOT markets, which also made side payments to constrained on/off generators. • Your market has proved this again, as your MSP recently noted. 38

Uniform Prices Provide Poor Investment Signals • Poor signals for generation investments. • Generators have incentives to locate at the wrong locations. • Eventually, you need added incentives/penalties to encourage new entrants to site at the right locations. • Plus worse signals for demand-side investments. • You get too little response where you need it, and too much response where you don’t. • No signals for appropriate grid investments. 39

Does Zonal Pricing Fix These Problems? • In general, zonal pricing tends to give better locational price signals than uniform pricing, but not as good as nodal pricing. • And all of the problems of uniform pricing still occur inside each zone, to the extent that congestion is not strictly “inter-zonal.” • But it never is, because zonal boundaries never capture all the congestion because . . . • Zones are often connected by loops, not single radial lines, and the loops can affect the extent of intra-zonal congestion. • But adding/redrawing new zones is politically difficult. • Contracts are based on expectations of stable zones. • Inter-zonal FTR allocations depend on stable zones. • Thus, many parties have an interest in not fixing the problems. 40

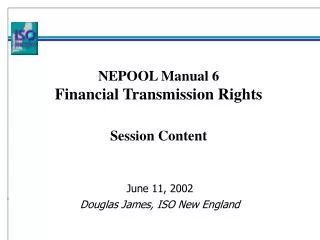

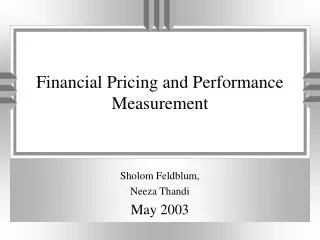

LMP Examples • The following two slides illustrate how LMP prices can differ between different locations on the grid when there is congestion. • These examples are drawn from much larger presentations given to the DAM and LTRA Working Groups, which provide more explanation. They are available on those IMO websites. • The examples reflect congestion, a security constrained dispatch in the contingency in which a major transmission line is assumed to be out, and the resulting nodal prices. • These examples don’t deal with marginal losses, but other presentations made to the WGs illustrate how locational prices can also differ because of losses. 42

290 MW 25 MW 5 MW 5 MW East LSE North LSE West LSE South LSE $32.50 $50.00 $20.00 $30.00 $35.00 East Coal West Gas West Nuke South Gen North IPP East Gas 90 MW Thermal 90 MW Thermal 50 MW Thermal 200 MW Thermal 80 MW Thermal 100 MW Thermal 25 MW $35.00 $35.00 $35.00 $50.00 $50.00 $50.00 $35.00 $32.50 $50.00 $37.50 $32.50 $32.50 $37.50 $50.00 $37.50 Southeast LSE DISPATCH IN D-X CONTINGENCY AND LOCATIONAL PRICES (bilateral) $0 K L 5 MW 25 MW W C M 60 MW 90 MW 290 MW` 25 MW A Y 25 MW 35 MW 100 MW OUT OF SERVICE IN CONTINGENCY Z 100 MW X D 50 MW 100 MW 25 MW 10 MW B V N 65 MW 5 MW P O SYSTEM LOAD = 350 MW 43 West Nuke 100 MW, West Gas 100 MW, North IPP 25 MW, South Gen. 90 MW, East Gas 50 MW, East Coal 100 MW

320 MW 25 MW 15 MW MW 5 MW 150 MW North LSE Central LSE East LSE West LSE South LSE $35.00 $20.00 $50.00 $32.50 $30.00 South Gen East Gas West Gas East Coal West Nuke North IPP 10 Thermal MW 80 Thermal MW 100 Thermal MW 200 Thermal MW 90 Thermal MW 90 Thermal MW 30 Thermal MW 25 MW $50.00 $67.50 $32.50 $32.50 $67.50 $35.00 $50.00 $35.00 $50.00 $-22.50 $50.00 $67.50 $35.00 Southeast LSE DISPATCH IN D-X CONTINGENCY AND LOCATIONAL PRICES (New Load at Q) (bilateral) $0 K L 150 MW 25 MW W C M 90 MW 320 MW` 10 MW 10 MW 25 MW A Y 190 MW 70 MW Q 100 MW OUT OF SERVICE IN CONTINGENCY Z 100 MW X D 45 MW 55 MW 25 MW B 25 MW V N 55 MW 5 MW P O SYSTEM LOAD = 525 MW 44 West Nuke 100 MW, West Gas 75 MW, North IPP 25 MW, South Gen. 100 MW, East Gas 200 MW, East Coal 100 MW

Enhancements to Nodal Settlement Options • Even better, Ontario could allow appropriately metered price-responsive loads (typically large customers) to opt-out of the average and be settled at their respective nodal or sub-regional aggregate price. • This would help stimulate demand-side responses by those most capable of responding to changes in spot prices. • Facilitating price-responsive demand would create many benefits: • It would dampen price spikes and make spot prices less volatile. • It could help define scarcity prices that would stimulate efficient investment levels. • It would encourage efficient demand-side investments and load-shifting, and at the right times and locations. • It would help mitigate market power. 46

LMP Settlements for Load-serving Entities • The DAM WG Strawman anticipates that Ontario solves the “market buyer” issue by creating a set of load-serving entities (LSEs) that will participate in the Ontario markets on behalf of default customers. • Default customers are those who don’t chose competitive retailers. • Ontario would need to decide how to select these LSEs. • Ontario could designate these entities (e.g., the LDCs). • Or LSEs could be selected through competitive auctions (some US states do this) that both choose the LSEs and set the retail default supply price for defined periods (e.g., every two years). • And Ontario would need to decide who/what an LSE represented: • A percentage of the total Ontario default load? • All the default load in some defined sub-region of Ontario? • Or some combination of both. 47

LMP Settlements for Load-serving Entities • No matter how the LSE load were defined, an LMP settlement system would fully support LSE efforts to serve their loads at the lowest cost. • LSEs would presumably choose portfolios of generation supplies that best matched their customers’ load profiles • LSEs would contract with generation suppliers for some portion of their expected total requirements. • LSEs could also purchase spot energy from the IMO-administered spot markets to support/back up their supply contracts. • LSEs could participate or not in an IMO DAM • Or purchase spot energy and/or imbalances in the IMO RTM. • LSE purchases from the spot market would be settled at the IMO LMP prices, based on whatever aggregation level was used. 48

LMP Settlements for Load-serving Entities • LMP settlements for LSEs would be based on whatever degree and type of nodal/LMP aggregation applied in Ontario. For example: • If a province-wide nodal aggregation (“uniform price”) applied to all default customers, and each LSE served a percentage of the Province’s default customers, the LSE purchases from the IMO spot markets would be at the province-wide uniform price = the load-weighted average of nodal prices for all default loads across the province. • That’s the same as the Ontario-wide average nodal price, after removing from the average those more active market loads who are settled at their respective nodal prices. • If Ontario split into distinct load regions or zones, the LSE in each region or zone would be settled at the zonal uniform price = the load-weighted average of nodal prices for all default loads across the zone. • Many combinations are possible. It’s just math. 49