Download

1 / 14

170 likes | 378 Views

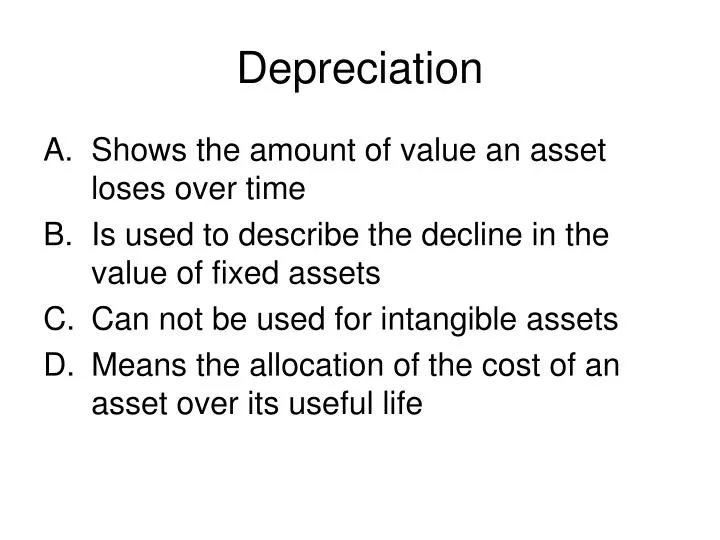

Depreciation. Shows the amount of value an asset loses over time Is used to describe the decline in the value of fixed assets Can not be used for intangible assets Means the allocation of the cost of an asset over its useful life.

E N D

Depreciation • Shows the amount of value an asset loses over time • Is used to describe the decline in the value of fixed assets • Can not be used for intangible assets • Means the allocation of the cost of an asset over its useful life

E 11-4 using straight line, depreciation expense for year two would be • $30,000 • $31,500 • $31,800 • $31,875

E 11-4 using units of output, depreciation expense for year two would be • $30,000 • $31,500 • $31,800 • $31,875

E 11-4 using hours, depreciation expense for year two would be • $30,000 • $31,500 • $31,800 • $31,875

Indications of Asset Impairment (FAS 144) • Decrease in market value of equivalent assets • Decrease in expected future cash flows from asset • Legal/regulatory problems • Increased operating costs • Decline in demand for output (or decline in price of output) • Significant increase in construction costs • Decrease in stock price (after merger)

Evaluation of Asset Impairment Compare expected UNDISCOUNTED net cash flows (NCF) from asset with book value (BV): • NCF > BV = No impairment • NCF < BV = Impairment

Evaluation of Asset Impairment II If impairment: Compare DISCOUNTED present value of expected net cash flows with market value. • PV of NCF > MV = write down to PV, continue to use/depreciate • PV of NCF < MV = write down to MV – evaluate for disposal

Evaluation of Asset Impairment II PV of NCF < MV = write down to MV – • evaluate for disposal: Asset is would be worth more if sold. If decision is made to sell: • Stop depreciation, report asset at net realizable value (MV) in separate section of Balance sheet: “Assets to be disposed off” Note: This is a business, NOT and accounting decision!

Recovery of Asset Value after Impairment • If asset is being used recovery of value is ignored. No write –up permitted, once asset has been written down. • If asset is being held for sale, shown at net realizable value (NRV) asset MAY be written up, up to original carrying value before impairment was recognized.

Problem 11-9 • What is the amount of asset impairment?

Problem 11-9: The entry to write down the asset includes • A debit to equipment for $1.6 mil • A credit to equipment for $1.6 mil • A debit to accumulated depreciation for $1.6 mil • A credit to accumulated depreciation for $1.6 mil

Problem 11-9 What is the new depreciation expense?

Oil and Gas Exploration • FAS 19 – suspended • No definitive standard • Political issue – may become interesting again given current gasoline price situation

(slide 2) A (Slide 3) D (Slide 4) C (Slide 10) $1,600,000 (slide 11) D (slide 12) $1,100,000 Answers