Download

1 / 11

210 likes | 485 Views

STRATEGIC MANAGEMENT ACCOUNTING Product Profitability. Product costing has been a mainstay of cost and management accounting for many years. Very sophisticated cost apportionment systems have been developed.

E N D

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Product costing has been a mainstay of cost and management accounting for many years. Very sophisticated cost apportionment systems have been developed. However, decision making based on relative product profitabilities is still new and often proving difficult to come in terms with. In the “not so competitive past” contribution margins were high enough to cover all other costs of the business and leave acceptable profit.

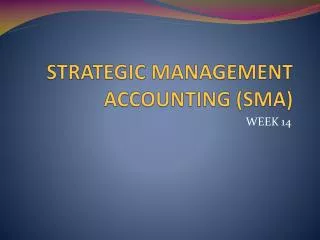

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Through a rough overheads’ apportionment, often some highly profitable products are used to subsidize the less successful. Cross-subsidization may be a very successful long-term strategy, but it should be a conscious management decision. However, in many companies profit/ volume relationship is still considered a key determinant of financial success. It requires strict classification of costs into “fixed” and “variable”.

STRATEGIC MANAGEMENT ACCOUNTINGProduct ProfitabilityProfit/Volume Graph

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Profit/volume approach may often be too simplistic. Absence of detailed product profitability analysis cannot assess the impact of various marketing actions, changing the marketing mix, launching of new products, product withdrawal. Historically, the “cost plus pricing” was widely used. Recently, “fixed price contracting” is gaining momentum. Thus all cost overruns are turned back to the contractor. Many industries (IT, defense etc) operate on this basis.

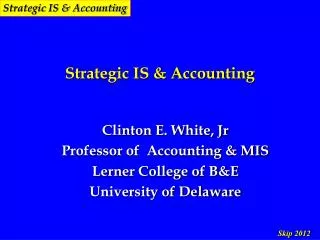

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Direct Product Profitability (DPP)

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Direct Product Profitability (DPP) Above analysis indicates that an apparently low contribution product has actually a higher relative contribution, in view of its ease of sale and space occupied. The technique has been adopted by most retailers and consultants, as well as a valid marketing tool for manufacturers selling through intermediaries. Highlighting the relative profit contribution gives an important competitive advantage to the product.

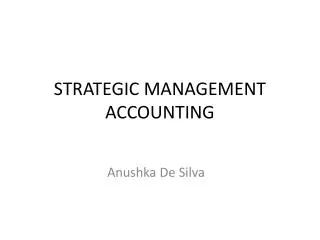

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Product Attributes Same product may be sold in different formats, which may vary in: • Size of packaging • Sellingbrand • Channel of distribution What should then be considered as an individual product? How should overheads be apportioned and product cost be determined? See following chart:

STRATEGIC MANAGEMENT ACCOUNTINGProduct ProfitabilityProduct Attributes

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Cross-subsidizing products Often products are linked more by common customers, than by internally shared resources. It is quite common, competitive strategy to use one “loss leader” in order to sell other profitable products to the same or related customers. This creates severe complications for any product profitability analysis, yet it is vital that this competitive strategy is carefully financially evaluated and monitored.

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Cross-subsidizing products Cross subsidizing within the computer industry

STRATEGIC MANAGEMENT ACCOUNTINGProduct Profitability Cross-subsidizing products It will be easier for a company to maintain its overall market share and increase profitability if it maximizes its selling price of any monopolistic products. This will attract competitors. Entry barriers and externally focused competitor accounting should provide early warning signs. In such industries, companies may choose to focus on very limited elements, with the large companies, offering complete ranges, declining.