Download

1 / 66

670 likes | 836 Views

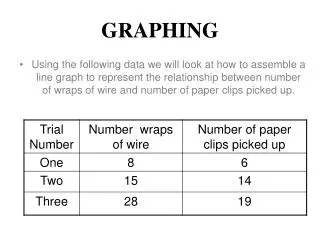

Graphing Guide. Production Possibilities. How does the PPG graphically demonstrates scarcity, trade-offs, opportunity costs, and efficiency?. 14 12 10 8 6 4 2 0. Impossible/Unattainable (given current resources). A. B. G. C. Bikes. Efficient. D. Bowed-Out shape of curve

E N D

Production Possibilities How does the PPG graphically demonstrates scarcity, trade-offs, opportunity costs, and efficiency? 14 12 10 8 6 4 2 0 Impossible/Unattainable (given current resources) A B G C Bikes Efficient D Bowed-Out shape of curve Indicates increasing opportunity cost Inefficient/ Unemployment E 0 2 4 6 8 10 Computers

The Demand Curve • A demand curve is a graphical model of demand. • The demand curve is downward sloping (Double D) showing the inverse relationship between price (on the y-axis) and quantity demanded (on the x-axis) • When reading a demand curve, assume all outside factors, such as income, are held constant.

Change in Demand Demand Schedule Price of Cereal $5 4 3 2 1 Demand o Q 10 20 30 40 50 60 70 80 Quantity of Cereal 5

Change in Demand Demand Schedule Price of Cereal Increase in Demand Prices didn’t change but people want MORE cereal $5 4 3 2 1 D1 Demand o Q 10 20 30 40 50 60 70 80 Quantity of Cereal 6

Demand Shifters • 1) Number of Consumers • 2) Income of Consumers (Normal and inferior goods) • 3) Price of related goods (Substitutes and Complements) • 4) Change in taste and preferences • 5) Change in expectations

Supply Defined What is the Law of Supply? There is a DIRECT (or positive) relationship between price and quantity supplied. • As price increases, the quantity producers make increases • As price falls, the quantity producers make falls. Why? Because, at higher prices profit-seeking firms have an incentive to produce more.

GRAPHING SUPPLY Supply Schedule Price of Cereal Supply $5 4 3 2 1 o Q 10 20 30 40 50 60 70 80 Quantity of Cereal 10

Change in Supply Supply Schedule Price of Cereal Supply S2 $5 4 3 2 1 Increase in Supply Prices didn’t change but there is MORE cereal produced o Q 10 20 30 40 50 60 70 80 Quantity of Cereal 11

6 Shifters (Determinants) of Supply • Prices/Availability of inputs (resources) • Number of Sellers • Technology • Government Action: Taxes & Subsidies 5. Opportunity Cost of Alternative Production 6. Expectations of Future Profit Changes in PRICE don’t shift the curve. It only causes movement along the curve.

Supply and Demand are put together to determine equilibrium price and equilibrium quantity P Supply Schedule Demand Schedule S $5 4 3 2 1 Equilibrium Price = $3 (Qd=Qs) D o Q 10 20 30 40 50 60 70 80 Equilibrium Quantity is 30 14

Surplus Maximized P S CS Pc PS D Qe Q

Shifts and Double Shifts • Determine what will always happen to the equilibrium price and quantity when… • 1) Demand increases (P-Increase, Q-Increase) • 2) Demand decreases (P-Decrease, Q- Decrease) • 3)Supply increases (P-Decrease, Q- Increase) • 4) Supply decreases (P-Increase Q-Decrease) • 5) Supply and demand both increase (P-Indeterminant, Q-Increase • 6) Supply and demand both decrease (P- Indeterminant,- Q-Decrease • 7) Supply increases and demand decreases (P-Decrease, Q-Indeterminant • 8) Supply decreases and demand increases (P- Increase, Q-Indeterminant

Supply and Demand Analysis Easy as 1, 2, 3 • Before the change: • Draw supply and demand • Label original equilibrium price and quantity • The change: • Did it affect supply or demand first? • Which determinant caused the shift? • Draw increase or decrease • After change: • Label new equilibrium? • What happens to Price? (increase or decrease) • What happens to Quantity?(increase or decrease)

Price Floor Minimum legal price a seller can sell a product. Goal: Keep price high by keeping price from falling to Eq. P Corn S Surplus (Qd<Qs) Price Floor Does this policy help corn producers? D o Q 10 20 30 40 50 60 70 80 20

Are Price Controls Good or Bad? To be “efficient” a market must maximize consumers and producers surplus P S CS Price FLOOR DEADWEIGHT LOSS The Lost CS and PS. INEFFICIENT! Pc PS D Qfloor Qe Q

Price Ceiling Maximum legal price a seller can charge for a product. Goal: Make affordable by keeping price from reaching Eq. P Gasoline S $5 4 3 2 1 Does this policy help consumers? Result: BLACK MARKETS Price Ceiling Shortage (Qd>Qs) D o Q 10 20 30 40 50 60 70 80 22

Are Price Controls Good or Bad? To be “efficient” a market must maximize consumers and producers surplus P S DEADWEIGHT LOSS The Lost CS and PS. INEFFICIENT! CS Pc Price CEILING PS D Qceiling Qe Q

Excise Taxes STax Supply Schedule P S $5 4 3 2 1 Tax is the vertical distance between supply curves D o Q 24 40 60 80 100 120 140

Gold Gasoline

Perfect Competition P S P MC ATC MR=D $15 $15 AVC D Q Q 8 5000 Firm (price taker) Industry 30

The Competitive Firm is a Price Taker Price is set by the Industry What is the additional revenue for selling an additional unit? 1st unit earns $15 2nd unit earns $15 Marginal revenue is constant at $15 Notice: • Total revenue increases at a constant rate • MR equal Average Revenue P Demand $15 MR=D=AR=P Q Firm (price taker) 31 31

When Is Production Profitable? • If TR > TC, the firm is profitable. • If TR = TC, the firm breaks even. • If TR < TC, the firm incurs a loss.

How much output should be produced? • How much is Total Revenue? How much is Total Cost? • Is there profit or loss? How much? P MC $9 8 7 6 5 4 3 2 1 Chicken Market MR=D=AR=P ATC Profit = $18 AVC Don’t forget that averages show PER UNIT COSTS Total Cost=$45 Total Revenue =$63 Q 1 2 3 4 5 6 7 8 9 10

How much output should be produced? • How much is Total Revenue? How much is Total Cost? • Is there profit or loss? How much? MC Chicken Market $9 8 7 6 5 4 3 2 1 ATC Cost and Revenue AVC Loss =$7 MR=D=AR=P Total Cost = $42 Total Revenue=$35 Q 1 2 3 4 5 6 7 8 9 10

Profit Maximizing Rule MR = MC Three Characteristics of MR=MC Rule: • Rule applies to ALL markets structures (PC, Monopolies, etc.) • The rule applies only if price is above AVC • Rule can be restated P = MC for perfectly competitive firms (because MR = P)

MC above AVC is the supply curve Marginal Cost and Supply When price increases, quantity increases When price decrease, quantity decreases $50 45 40 35 30 25 20 15 10 5 0 MC = Supply ATC Cost and Revenue AVC Q 1 2 3 4 5 6 7 9 36

Is this the short or the long run? Why? • What will firms do in the long run? • What happens to P and Q in the industry? • What happens to P and Q in the firm? P S P MC ATC MR=D $15 $15 D Q Q 8 5000 6000 Industry Firm 38

Firms enter to earn profit so supply increases in the industry Price decreases and quantity increases P S P MC S1 ATC MR=D $15 $15 $10 D Q Q 8 5000 6000 Industry Firm 39

Price falls for the firm because they are price takers. Price decreases and quantity decreases P S P MC S1 ATC MR=D $15 $15 $10 MR1=D1 $10 D Q Q 8 5000 6000 5 Industry Firm 40

New Long Run Equilibrium at $10 Price Zero Economic Profit P P MC S1 ATC $10 MR1=D1 $10 D Q Q 5000 6000 5 Industry Firm 41

Is this the short or the long run? Why? • What will firms do in the long run? • What happens to P and Q in the industry? • What happens to P and Q in the firm? P S P MC ATC MR=D $15 $15 D Q Q 8 5000 4000 Industry Firm 42

Firms leave to avoid losses so supply decreases in the industry Price increases and quantity decreases S1 P S P MC ATC $20 MR=D $15 $15 D Q Q 8 5000 4000 Industry Firm 43

Price increase for the firm because they are price takers. Price increases and quantity increases S1 P S P MC ATC $20 $20 MR1=D1 MR=D $15 $15 D Q 9 Q 8 5000 4000 Industry Firm 44

New Long Run Equilibrium at $20 Price Zero Economic Profit S1 P P MC ATC $20 $20 MR1=D1 D Q 9 Q 4000 Industry Firm 45

Good news… • Only one graph because the firm IS the industry. • The cost curves are the same • The MR= MC rule still applies • Shut down rule still applies 47

What output should this monopoly produce? MR = MC How much is the TR, TC and Profit or Loss? $9 8 7 6 5 4 3 2 P MC ATC Profit =$5 D MR Q 1 2 3 4 5 6 7 8 9 10 48

Monopolies vs. Perfect Competition Where is CS and PS for a monopoly? S = MC P CS Total surplus falls. Now there is DEADWEIGHT LOSS Pm PS Monopolies underproduce and over charge, decreasing CS and increasing PS. D MR Q Qm 49

Regulating Monopolies Unregulated Socially Optimal Allocative Efficiency P MC Fair Return Pm ATC Pso Pfr D MR Q Qm Qso Qfr 50