Download

1 / 42

420 likes | 548 Views

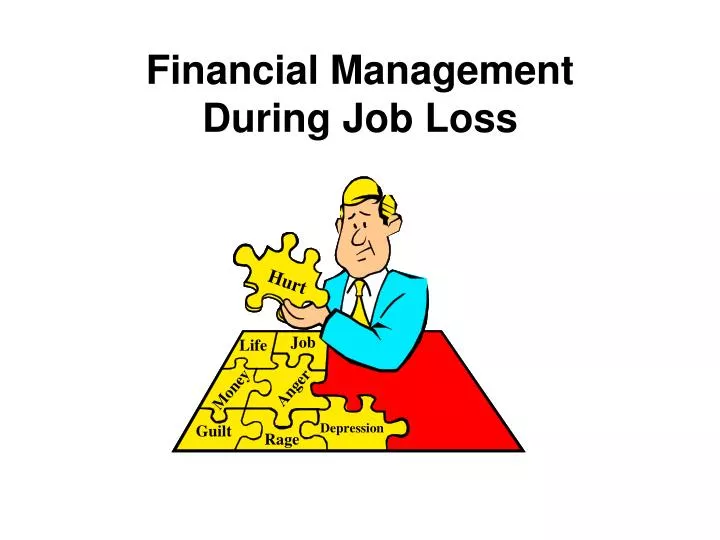

Financial Management During Job Loss. Issues To Be Resolved Regarding Your Job Search. CAREER. EMOTIONS. FINANCES. What Do You Feel?. Shock Anger Fear Resentment Depression Despair Resignation Acceptance Determination Action. Moving On

E N D

Issues To Be Resolved Regarding Your Job Search CAREER EMOTIONS FINANCES

What Do You Feel? • Shock • Anger • Fear • Resentment • Depression • Despair • Resignation • Acceptance • Determination • Action

Moving On (A Plan Of Action) Address Emotional Issues Address Career Issues Address Financial Issues Develop An Action Plan

Career Transition Workshop Northwest Bible Church 8505 Douglas (Northwest Highway & Tollway) Christian Life Center (Behind the main auditorium) FREE Mondays: 6:00 pm to 9:00 pm Call 972-763-2439 For more information www.careertransitionworkshop.org Learn how to find a job or a new career Network with volunteers and 200 plus jobseekers

Keep Records Make A Plan Take Inventory Set Goals Four Steps To Financial Success How are we going to survive this job loss? How are we going to pay the bills? What can we do to ensure the financial stability of the family and maintain a positive outlook? Discuss the situation with the entire family. Formulate a plan of action involving everyone. Consider various options Evaluate all recommendations.

Step One: Set Goals • Three types of goals: • 1. Short-term 2. Incremental 3. Long-term • Steps to Successful Goal Setting: • 1. Decide What you Want 6. Compare • *2. Commit To It (Write It Down) 7. Compromise • 3. Count The Cost 8. Reach Consensus • 4. Set Priorities 9. Develop A Time Line • 5. Communicate 10. Devise A Plan

Short Term Financial Objectives MONTHLY AMOUNT PRIORITY COST GOAL Start a savings account $ Training $ $ Improve wardrobe Gifts/Christmas fund $ Vacation $ Tires, auto repair $ Household repairs $ $ $

Long Term Financial Objectives MONTHLY AMOUNT GOAL PRIORITY COST $ Buy a house/improvements Education for children/self $ Comfortable/early retirement $ Replacement car $ Become debt-free $ Start retirement program $ Travel $ Start new business/career $ $

Step Two: Take Inventory Before You Can Devise A Plan To Get Where You Want To Go (GOAL), You Must First Determine Where You Are. Consider all: Assets Income Expenses

Assets Listing your assets will let you know exactly what resources you have to survive this transition. The effective use of existing assets helps the family face financial emergencies. Ideally, you will not have to dip into your retirement savings or sell your car during this time; however, it is good to know what assets you have to fall back on.

ASSET CASH VALUE Home $ 50,000 Other Real Estate $ -0- Rental Property $ -0- Household Goods $ 5,000 Jewelry $ 1,000 Vehicle 1 $ 6,000 Vehicle 2 $ 8,000 Vehicle 3 (RV) $ 17,000 Vehicle 4 (Boat) $ 15,000 Regular Savings $ 500 $ 55,000 CDs, IRAs, 401Ks, etc. $ 5,000 Art & Other Valuables $ $ $ 162,500 Step Two: Take InventoryAssets Net Worth

Step Two: Take InventoryMonthly Income List all income sources when you are unemployed Spouse’s Pay $ 1,500 Unemployment Benefits $ 1,000??? Interest/Dividends $ - 0 - $ - 0 - Worker’s Comp. Child Support $ - 0 - Other/Miscellaneous $ - 0 - Total Monthly Income: $ 2,500 +

Ask The Right Questions If there is not enough money to make ends meet: • Is the income sufficient to service at least the basic living expenses of the household? • If not, how much additional income will be needed to meet those needs? • How long can the family continue at the current level of spending? • What adjustments can be made to extend available funds?

Step Three: Make A Plan After setting goals and taking inventory you are now ready to devise a financial plan. That plan must include a workable budget and a plan for managing cash flow. But First: Decide to all non-essential spending immediately!!. Reduce living expenses

Making Wise Purchasing Decisions STOP All impulse buying. Most non-essential purchases THINK Do you need it? Must you have it now? Can you afford it? RESIST Door-to-door sales High-pressure sales All telephone sales & solicitations Television shopping clubs and Internet sales

Possible Housing Adjustments • Consider refinancing your home. • Consider selling your home and moving to a less expensive dwelling. • Re-negotiate your lease. • Consider moving to another apartment complex if you have difficulty moving within the current units or re-negotiating your existing lease agreement.

Be Prepared To MakeChanges And AdjustmentsIn Lifestyle. • Consider selling existing real estate holdings. • Any rental property or land may have to be sold. • Nothing should be held absolutely inviolate. • Sell a car, boat or recreational vehicle.

Be Prepared To MakeChanges And AdjustmentsIn Lifestyle. • Sell, or use as collateral, jewelry having high value. • Be careful with heirloom jewelry, it is at risk when used for collateral. • Have a garage sale, or place on consignment • exceptionally good clothing, electronic equipment, • musical instruments or other items.

Helpful Hints • Try these cost cutting tips: • Get into the habit of clipping coupons. • Use sale papers and flyers to search for the best deals. • Buy food in bulk sizes. Break it up and store it in smaller quantities. • Buy Store brands. • Shop with a list

Helpful Hints • Ways To Make Extra Money: • Have a garage sale to earn extra cash from things you no longer need. • Sell some valuable items you do not use. • Sell big-ticket items such as a boat or an extra car. This will generate emergency cash and perhaps save on insurance. • Don’t forget aluminum cans, newspapers and plastic. Call your nearest recycling center for details.

Variable Expenses Monthly $ Income Type Income Type Income Type Income Type Income Type Weekly ($ x 12) /12 Every other week ($ x 12) /26 Twice per month $/2 Once per month $ x 1 Commission Bonus Food Transportation Fuel Oil Public Transportation Medical/Pharmacy Charity/Gifts/Donations Miscellaneous Cable/Satellite/Internet/DSL Personal Care Expenses (Hair, nails, etc.) School Expenses: Supplies, Sports, Activities etc. Clothing Meals Out Dry Cleaning/Laundry Pets: Food, Supplies, Vet Entertainment: Video rentals, movies, etc. Gifts for Birthday, Anniversary, etc. Alcohol/Cigarettes Hobbies Pocket Money (Petty Cash) Monthly Spending PlanDate: _______________

Step Four: Keep Records It is important to make a plan, but it is also necessary to work the plan. You must keep good records in order to determine if you are staying on track with your plan.

Payday Time Frame Paydays Paydays Paydays each week. every 2 twice a One 4 months per weeks on a month on a paycheck year have 5 given DAY. given DATE. per month paydays. 26 paydays 24 paydays only. per year per year. DATES TO REMEMBER PAYDAY CALENDAR Monthly Weekly Bi-Weekly Semi-Monthly Payday #1 Payday #2 Misc. Misc.

Part Three Credit

The Credit Card Temptation~~~!!!! Resist the Temptation!!! • The temptation to live on credit cards during difficult times. • You may find it necessary to contact your creditors to arrange lower payments. • Never refuse to talk to your creditors. • Explain your circumstances. • Get any agreement in writing. • Keep your creditors informed of your situation.

The Credit Card Temptation~~~!!!! • Things to negotiate with your creditors: • Forbearance agreement on your mortgage—(An adjustment in your payments arrangements for a specified length of time.) • Moratorium on your credit card accounts—(reduced or suspended payments for a specified length of time.) • Interest only payments—(pay only the interest on loans for a specified length of time until you resume normal payments.) It is far wiser to reduce spending. Adjust the lifestyle to fit the finances.

YOUR FRIENDLY CREDIT CARD Company We Love You, U. S. A. 10000 DATE January 2, 2006 Mr. Iou Money ACCOUNT NUMBER 123-0000-5555 1234 Any Street Some Town, TX 70000 AMOUNT ENCLOSED $ PAYMENT DUE January 15, 2006 (PLEASE DETACH AND RETURN WITH YOUR REMITTANCE) CHARGES AND CREDITS DATE 36 85 12/02/05 Big Jim’s Restaurant 139 95 12/09/05 Biggest Retail Store 12/13/05 48 99 Spicy Gifts By Mail -27 95 12/14/05 Payment 101 75 Super Market Grocers 12/20/05 12/23/05 Biggest Retail Store ***Credit*** -20 51 16 30 1/1/06 Finance Charge MONTHLY INTEREST RATE NEW BALANCE PAYMENTS & CREDITS CHARGES MINIMUM REQUIRED PAYMENT PREVIOUS BALANCE FINANCE CHARGE SUBTOTAL APR $26.41 $16.30 $1320.67 2% $1025.29 $327.54 15% $1304.37 1.25% -$48.46 Sample Credit Account Statement

THE BIG THREE CREDIT REPOSITORIES EXPERIAN CREDIT DATAIf you have not been denied credit, but By Phone: would like to request a report: National 888-Experian (397-3742) Experian TDD (800) 972-0322 Attn.: NCAC PO Box 2104 To dispute a credit report, call the number Allen, TX 75013-2104 specified on your credit report. www.experian.com TRANS UNION PO Box 1000 By Phone: Chester, PA 19022 National (800) 916-8800 www.transunion.com To dispute a credit report, Call (800) 916-8800 EQUIFAX CSC Credit Services By Phone: P. O. Box 105873 National (800) 685-1111 Atlanta, GA 30348 Local (800) 392-7816 www.equifax.com Disputes accepted only by mail

THE CREDIT REPORTING PROCESS • BIG • 3 CREDIT • REPORTING • AGENCIES (CRA) • Receive and Store • credit data • Update data • Provide credit reports Provide Data CREDITORS (New/Updates) • FREE if: • Denied credit (past 60 days) • Unemployed – Seeking Employment • Receiving Public Assistance • Victim of Fraud Affecting Credit Credit Report Request CONSUMER NOTE: Under the 2003 Fair and Accurate Credit Transactions (FACT) Act you are allowed one free credit report each year from each of the 3 major CRA’s. The website to obtain your free credit report is www.annualcreditreport.com. 32

Step 2 You dispute incorrect information on your credit report online, by phone, or by mail OR Contact the creditor directly to dispute Step 3 Credit Bureau investigates your dispute with the Creditor Step 1 You receive a copy of your credit Report Step 4 Creditor investigates for accuracy and responds to the Credit Bureau. Any changes are reported to the Credit Bureau Credit Bureaus’ Dispute Process Step 6 Results are delivered to you within 30 days (45 if you dispute information in your free annual disclosure report) Step 5 Credit Bureau updates credit file on responses from creditor (no update if information verified) 33

Fair And Accurate Credit Transactions Act of 2003(FACT Act) • The Fair And Accurate Credit Transactions Act of 2003 amends the Fair Credit Reporting Act (FCRA). The FCRA regulates credit bureaus. • Facilitates the fight against credit fraud and identity theft. • The free reports became available in Texas in June, 2005. www.annualcreditreport.com

HOW LONG IS THE INFORMATION RETAINEDON THE CREDIT REPORT • Open Accounts in good standing Indefinitely • Closed accounts in good standing 10 years* • Late or missed payments 7 years** • Collection accounts 7 years** • Civil Judgments 7 years*** • Chapter 7 bankruptcy 10 years*** • Chapter 13 bankruptcy 7 years*** • Unpaid tax liens 15 years*** • Paid tax liens 7 years**** • Credit inquiries 2 years * Time measured from date closed *** Time measured from filing date ** Time measured from original delinquency date **** Time measure from paid date

The driving force in loan approval is your credit score. Credit scoring formalized and computerized the decision making process and, upon the surface of it, levels the playing field for all borrowers. The process for credit scoring is a mathematical one based upon values placed on predetermined criteria. Criteria for a credit scoring: Payment History - approx 35% of FICO Score Amount Owed - approx 30% of FICO Score Length of Credit History - approx 15% of FICO Score New Credit - approx 10% of FICO Score Type of Credit - approx 10% of FICO Score

Photocopying or electronic scanning of any and all parts of this presentation is unlawful and prohibited without the express written consent of Consumer Credit Counseling Service of Greater Dallas, Inc. All rights reserved. • 1-888-995-HOPE (4673) • www.995hope.org