Download

1 / 6

60 likes | 225 Views

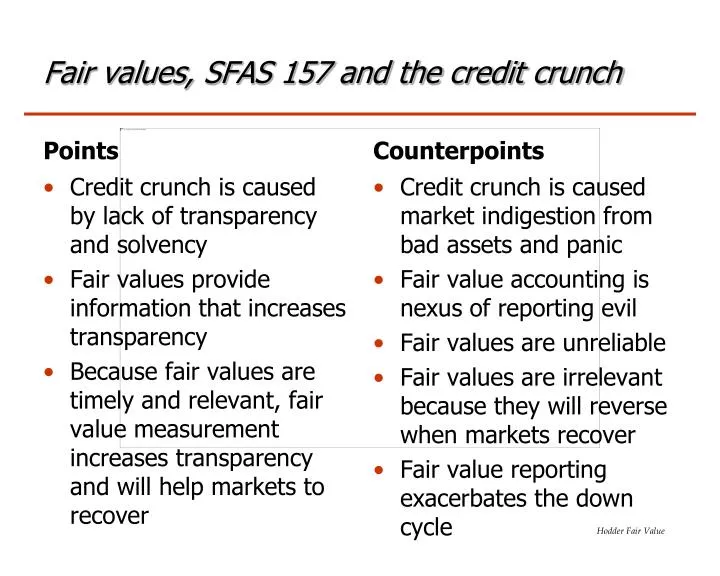

Fair values, SFAS 157 and the credit crunch. Points. Counterpoints. Credit crunch is caused market indigestion from bad assets and panic Fair value accounting is nexus of reporting evil Fair values are unreliable Fair values are irrelevant because they will reverse when markets recover

E N D

Fair values, SFAS 157 and the credit crunch Points Counterpoints Credit crunch is caused market indigestion from bad assets and panic Fair value accounting is nexus of reporting evil Fair values are unreliable Fair values are irrelevant because they will reverse when markets recover Fair value reporting exacerbates the down cycle • Credit crunch is caused by lack of transparency and solvency • Fair values provide information that increases transparency • Because fair values are timely and relevant, fair value measurement increases transparency and will help markets to recover

Potential research areas • Does fair value accounting provide relevant and reliable (useful) information? • Is disclosure of fair values equivalent to recognition? • Are some fair values more reliable than others? • Can fair value changes be disaggregated in a meaningful way? • Can contextual disclosures make fair values more useful? • Does fair value accounting contribute to procyclicality?

New FV Standards and Data • SFAS 159 gives firm the option of using fair value for certain financial assets and liabilities • SFAS 157 greatly increases the quantity of fair value disclosures • Level 123 data for assets and liabilities measured at FV on a recurring basis (note that this excludes many SFAS 107 fair value disclosures) • Personal experience: Income statement effects are still difficult to quantify. • Electronic data availability: 123 data now available on Compustat; SFAS 159 data available from bank call reports.

Examples of Recent Research • Song Thomas and Yi (2009) • Incremental value relevance of SFAS 157 levels • Relative value relevance of levels • Cross sectional variation in value relevance due to corporate governance • Goh, Ng and Yong (2009) • Pricing (relative value relevance of SFAS 157 levels) • Time series trend in relative value relevance of SFAS 157 levels • Cross sectional variation in value relevance due to audit quality and capital adequacy • Khan (2009) • Procyclical effects of fair value accounting • Bhat (2009) • Risk relevance of fair value accounting • Cross sectional variation in risk relevance due to disclosure quality

Research Challenges • What comprises “fair value accounting” anyway? • loans held for sale? • “in market” assets? • impairments? • disclosure vs. recognition, • OCI vs. net income • Noisy, inefficient markets make detection and interpretation of results difficult • what are implications if disclosure is correlated with values deemed irrational or unrepresentative?

Research Challenges • Value-relevance regressions are not very good at quantifying the relative value-relevance of individual income statement or balance sheet components • measurement error in all other independent variablesaffects coefficient bias of any single variable • omitted variables affect coefficient bias • misspecification of functional form affects coefficient bias. • Income statement effects of fair value measurements are still hard to come by • Studies of procyclicality need to distinguish real effects from accounting effects