Download

1 / 16

E N D

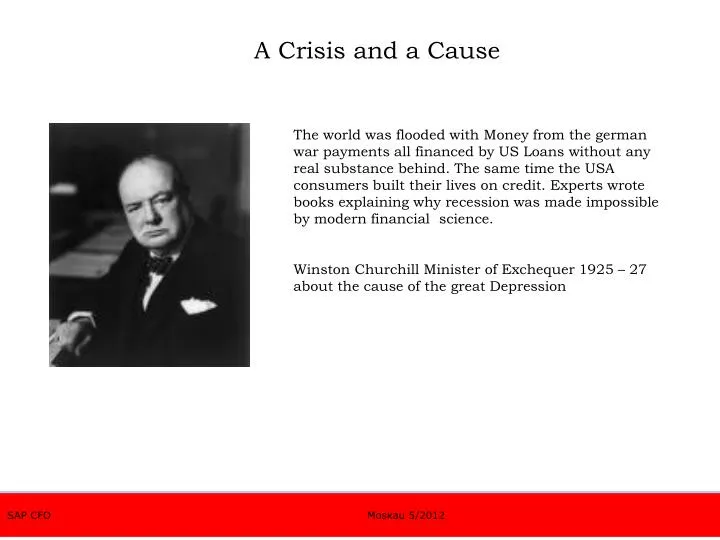

A Crisis and a Cause The world was flooded with Money from the german war payments all financed by US Loans without any real substance behind. The same time the USA consumers built their lives on credit. Experts wrote books explaining why recession was made impossible by modern financial science. Winston Churchill Minister of Exchequer 1925 – 27 about the cause of the great Depression SAP CFO Moskau 5/2012

A different Krisis and a Cause Extreme Amounts of Liquidity due to huge credits. This credits became possible due to mathematical constructs which made risk disappear. The very foundations of these constructs where wrong and everybody involved knew that. These constructs show chaotic behavior under certain (actual) circumstances. Thus it became impossible to calculate their real value. The Reason for the crisis is a Riskmanagement which tried to eliminate risk SAP CFO Moskau 5/2012

Eine andere Krise und ihre Ursache Normal Distribution was used zu describe riskprofiles that were not caused by stochastik events.(neglecting the Thick Tails) Mathematic manageable Coupling between the Risks was neglected SAP CFO Moskau 5/2012

CEE Vienna Middle East • 2 Billion Turnover • 6000 MA • 100% Lufthansa Daughter • Connects East EU, CEE and Middle East with West EU and Long Range • High Frequencies • Very short Connecting times • In Short: • Uses geopolitical Advantages of Vienna SAP CFO Moskau 5/2012

CEE Vienna Middle East AustrianAirlinesRisk Management Til 2006 Riskomanagement Classic Documentationofrisksandhowtoavoidthem Since 11/2006 Riskmanagement New QuantificationofOpportunitiesandtheRisksattached Since 08 - 10 Department RiskandOpportunities Management Betterdecisionmaking (1 yearrange) Since 2010 RiskQuantificationusedas a standardmethodof Controlling ( 1 yearrange) From 2012 Broadband Planning (5 yearrange) SAP CFO Moskau 5/2012

What is Riskmanagement? • Classic methodstoobtainandbolsterstrategical und taticalplansreducetheworldtothemostassuredcase. • ROI • Long Term Plan • Budget • Projectbudget • The mostassuredcaseisalwaysatrisk. • Result: Gut feelingmakesthedecision. Riskmanagementmakes gut -feeling transparent SAP CFO Moskau 5/2012

Opportunity and Risk Management Key Words • Managing risks enhances AUSTRIAN´s opportunities • We moderate risk evaluation and quantification • We make gut feeling transparent and comparable • There is no such thing as a non-quantitative Chance (albeit you may need a lot of work) SAP CFO Moskau 5/2012

Direct quantification of thick tails defeats gut-feelings SAP CFO Moskau 5/2012

Add theThickTailswith Monte Carlo Customer lossworlwide15% EW 5% once in 20 years Customer lossworldwide 5% EW 20% once in 5 years SAP CFO Moskau 5/2012

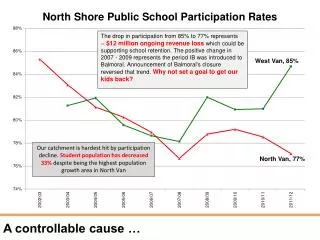

50% Percentile vs Financial Forcast Risk 50% Percentile -16mio€ Controlling Forcast end of Q1: -8mio€ SAP CFO Moskau 5/2012

Shift of the most likely caseThick tails are not the only consequence 50% shift SAP CFO Moskau 5/2012

Decouple first – then compare Risk 50% Percentile -9mio€ Risk 50% Percentile -16mio€ Controlling Forcast end of Q1: -8mio€ SAP CFO Moskau 5/2012

Risikcoupling Price of crude with economy Many risk minimising strategies have a big inherent downside Risk SAP CFO Moskau 5/2012

AF Crude Hedging withCollar AF is covered against rise of crude with a call option worth 400mio€ Brent USD AF acts as insurer. They sell Put Options for 400mio€, thus financing the call option 2007 2008 SAP CFO Moskau 5/2012

Coupling 9/11 or 1973 with price for crude SAP CFO Moskau 5/2012

Insuringtheresultsof a companyis a paradox • No positiv results due to extrem costs for insurance, or in exchange a new and possible letal risk. • Only live insurance makes sense. • The actual survival of a company does not depend on revenue - it depends on liquidity. SAP CFO Moskau 5/2012