Download

1 / 26

580 likes | 1.5k Views

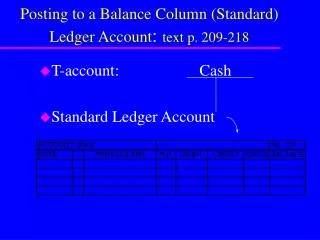

Chapter 7. Posting to the Ledger. The Balance Column Account. The most commonly used ledger account is the balance column account . It has three money columns: one for debit amounts; one for credit amounts; and a third that shows the account balance. Opening an Account.

E N D

Chapter 7 Posting to the Ledger

The Balance Column Account • The most commonly used ledger account is the balance column account. • It has three money columns: one for debit amounts; one for credit amounts; and a third that shows the account balance.

Opening an Account To open an account you must: • Obtain an unused account page • Write the name for the new account at the top of the page. The account name is known as the account title and will be written on the back of the page as well. • Write the account number (from the chart of accounts). • Insert new account in its proper place in the ledger.

Each entry is recorded by date … identical to the date conventions used in the General Journal. Each entry has its own line. 2007 Comparison of Ledger Accounts T-Account The Balance Column Account

Particulars column is used for additional explanations. Not often used as particulars can be obtained from the General Journal. The posting reference (PR) Records the page number of the journal (where the transaction was journalized). Write the letter “J” and the page number. The debit and credit columns form the core of the account. Record the debit/credit from the journalized transaction in the appropriate column. The balance is calculated and shown after each entry. The “DR./CR.” column indicates the type of balance. This may change from entry to entry. The account name and number are recorded at the top of every ledger account. This information is available from the chart of accounts. 2007 Comparison of Ledger Accounts

Formal Posting • In Chapter 6, you learned that each accounting entry is first recorded in the journal (a.k.a. journalizing). • These entries are then transferred, or posted, to the ledger. • Posting is the process of transferring information from the journal to the ledger. • Every individual amount recorded in the journal must be posted separately.

Six Steps in Posting Entries • For each individual amount entered in the journal, you must follow six steps. • Five of the steps are performed in the ledger; one is performed in the journal.

2007 110 Step 1: Select proper account Step 3: Record the journal page #. Step 2: Record the date. Step 4: Record $’s in proper col. Step 5: Record new balance and indicate if it is DR or CR. Step 6: Record account number in journal. 2007 14 J14 4 2 5 -- DR 1 3 0 2 06 Aug. Posting Entries - Example 110 Aug. 14 J14 4 2 5 -- DR 1 3 0 2 06

2007 110 101 Step 3: Record the journal page #. Step 1: Select proper account Step 2: Record the date. Step 5: Record new balance and indicate if it is DR or CR. Step 6: Record account number in journal. Step 4: Record $’s in proper col. 2007 14 J14 1 5 0 -- DR 1 0 5 6 15 Posting Entries - Example 101 14 J14 1 5 0 -- DR 1 0 5 6 15

2007 110 101 212 Step 2: Record the date. Step 6: Record account number in journal. Step 5: Record new balance and indicate if it is DR or CR. Step 3: Record the journal page #. Step 4: Record $’s in proper col. Step 1: Select proper account 2007 14 J14 2 7 5 -- CR 2 7 5 -- Aug. Posting Entries - Example 212 Aug.14 J14 2 7 5 -- CR 2 7 5 --

2007 Cross-Reference:A posting reference confirms that the entry has been posted to the ledger. No posting reference in the journal indicates that the entry has not yet been posted. Posting Cross-Referencing 110 101 212

Posting Cross-Referencing • Cross-Referencing: • Makes it easy to trace back to the General Journal. • Entries in the journal can be followed through to the ledger. • If the posting process is interrupted, it is easy to see what still needs to be posted.

Six Steps in Posting Entries • Turn to the proper account in the ledger. • Record the date. Use the next unused line in the account. • Record the page number of the journal in the posting reference (PR) column of the account. • Record the amount in the appropriate debit or credit column.

Six Steps in Posting Entries • Calculate and enter the new account balance in the balance column. Indicate whether it is a debit (DR) or credit (CR) balance. 6. In the journal, record the account number to which the posting was made. Enter this in the posting reference (PR) column on the same line as the amount being posted.

Correcting Errors in the Ledger • As a rule, accountants do not erase mistakes. • Errors found immediately are neatly stroked through and the correction is written above. • Errors found later can be corrected by means of an accounting entry.

Forwarding Procedure • Forwardingis the process of continuing an account, or a journal, on a new page by carrying forward the date and the balance from the previous page.

Class work • Pull out a General Journal that you have done in the past. 2. Using the Ledger Accounts provided, post the entries.

9. Prepare post-closing trial balance 8. Journalize and post closing entries 5. Journalize and post adjusting entries 7. Prepare financial statements 6. Prepare adjusted trial balance The Accounting Cycle 1. Analyse transactions 2. Journalize the transactions 3. Post to ledger accounts 4. Prepare a trial balance

Quick Tests for Detecting a Single Error The initial step in any of the quick tests is to calculate the trial balance difference – the amount by which the trial balance is out. • If the trial balance difference is a multiple of 10, such as 10 cents, 1 dollar, etc. An error in addition has likely been made. • Re-add the trial balance columns. • Re-calculate the balance of each account.

Quick Tests for Detecting a Single Error • Check both the ledger and the journal to see if the trial balance difference is equal to an amount entered in the ledger or the journal. • Whenever you find such an amount, verify it to make sure that it has been handled correctly.

Quick Tests for Detecting a Single Error • Divide the trial balance difference by two. • Then search (1) the trial balance and (2) the ledger accounts for this divided amount. • If an equivalent amount is found, check it carefully. In particular, look so see if a debit amount has been posted or transferred as a credit, or vice versa.

Quick Tests for Detecting a Single Error • If the trial balance difference is a multiple of 9, it is likely that a transposition error or a decimal point error has occurred. • A transposition error is a mistake caused by changing the order of digits when transferring figure from one place to another (i.e. $35.60 is posted as $36.50). • A decimal point error is a mistake caused by misplacing the decimal (i.e. $1.19 entered as $119.00)

Balancing the General Ledger • Sequence of Balancing Steps • Re-add trial balance columns. • Check transfer of account balances from ledger to T/B. • Re-add accounts from point of previous balance. Double-check account indicator (i.e. DR or CR). • Check postings from point of previous balance. Watch for: • Incorrect amounts. • Amounts not posted. • Amounts posted twice. • Amounts posted in wrong column. • Check to see that each individual journal entry balances (from point of previous balance). Does Trial Balance balance? Yes Yes No No File Trial Balance for future reference Apply the four “Quick Tests” End Does Trial Balance balance? Perform next Steps. Make corrections and recalculate Trial Balance. Any errors found? Yes No Take off a Trial Balance

Class / Homework • Exercise 1, p. 223 (need handout from workbook) • Exercise 2, p. 223