Download

1 / 38

380 likes | 530 Views

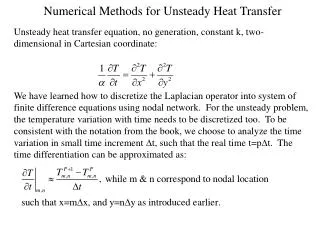

Methods of Asset Transfer. Sale Gift Estate (Die) Combination of two or three There are differences in tax implications. Basis Example. Current Land Value $4,500 / acre Purchase Price $ 1,000 $4,500 $ 6,000 Die $ 4,500 $ 4,500 $4,500 Gift $1,000 $ 4,500 $4,500*

E N D

Methods of Asset Transfer • Sale • Gift • Estate (Die) • Combination of two or three • There are differences in tax implications

Basis Example Current Land Value $4,500 / acre Purchase Price $1,000 $4,500 $6,000 Die $4,500 $4,500 $4,500 Gift $1,000 $4,500 $4,500* Sell $1,000 $4,500 $6,000* * gifting or selling to family, 2 year rule

Gifts Elements of a gift. Must have a donor. Must have a donee (recipient) of the gift. Must have actual or constructive receipt of the gift. • Gifts must be given free of any restrictions. • Gifts in any amount are not income to the recipient. • Gifts in excess of $13,000 ( 2011) per year to any one recipient will effect the gift tax credit.

Why do we have Estate Settlement? a). Determine who gets what b). Clear title to real estate c). Pay taxes

Intestate Succession Procedural aspects • Petition filed with probate court • Court appoints an administrator to “manage” the estate • Pay decedent’s debts • Pay administrative costs • Pay claims

Dying Testate (with a will)The Probate Process • Hearing held to admit will & appoint executor • Un-probated wills have no legal standing • Executor must file “acceptance of appointment” and file bond unless waived by will or heirs • Court issues “letters testamentary” or “letters of administration” • Probate process now begins

The Probate Process • Objectives of probate • Inventory assets • Settle disagreements • Obtain good title • Pay necessary debts and taxes • Distribute property

The Probate Process • Duties of the personal representative • Identify and take control of estate assets • File an inventory of the assets with the probate court • Pay all allowable creditor claims • Determine tax liability • Keep beneficiaries informed • Distribute assets

Intestate Succession • Distribution of Property at Death • The law of the decedent’s domicile (permanent residence) at death governs the succession of personal property (movables) • The law of the situs of property governs succession of real estate (immovables)

Intestate Succession • In General • The entire probate estate except: • Life insurance policies • Property held in joint tenancy with the right of survivorship • Payable on death accounts • Death benefits from pension plans

Intestate Succession • Distribution of Property at Death • Real and personal property typically descends to heirs immediately • A surviving spouse generally receives at least half of the estate • If children also survive, the spouse generally receives one-third and the balance passes to the children in equal shares • Uniform Probate Code – adopted (at least in part) by 22 states

Iowa Intestacy StatuteSec. 633.210 et. seq. • Only spouse survives (or spouse survives with issue all of whom are issue of surviving spouse) • Spouse gets all

Iowa Intestacy Statute • Spouse and issue (some of whom are not issue of surviving spouse) survive • Spouse receives ½ of real estate • Spouse receives all personal property that is exempt from execution • Spouse receives ½ of all other personal property • Any other property such that the sum of all property passing to surviving spouse is $50,000

Iowa Intestacy Statute • No spouse, but issue survive • To issue equally

Iowa Intestacy Statute • No spouse, no issue • To parents • Joint deaths?

Iowa Intestacy Statute • No spouse, no issue, no parents • To issue of parents

Iowa Intestacy Statute • No spouse, no issue, no parents, no issue of parents • To grandparents

Iowa Intestacy Statute • No spouse, no issue, no parents, no issue of parents, no grandparents • To issue of grandparents

Iowa Intestacy Statute • No spouse, no issue, no parents, no issue of parents, no grandparents, no issue of grandparents • To great-grandparents and then issue of great-grandparents • If none, then to issue of deceased spouse (or deceased spouses) • If none, to the state (escheat)

Intestate Succession • Disadvantages of intestacy • Inflexible distribution scheme • Continuity of farm business may be jeopardized • Conservatorship for minors and impaired heirs • Additional costs, taxes and delays

DISTRIBUTION by Will (Iowa) • Competency required to make a will Know the nature and extent of your estate Be able to formulate a plan of distribution Know the natural objects of your bounty Understand the relationship of the above • Must be witnessed by two witnesses in the presence of the testator and each other. • Must be revoked with the same formality with which they are made. • Amendments must be made with the same formality as a will. • Handwritten modifications to a will are of no effect.

Testate – with a will a). Sound mind, of age, not coerced b). Disinherit a spouse? c). Antenuptial d). Children e). Pets f). The will names the executor/trix and nominates the guardians… g). Special bequests list attached

Validity of Wills • General rule • Governed by law of domicile as to movables and law of situs as to real estate and other immovable's • If valid where executed, generally valid in other states • Watch attempted testamentary dispositions

Testate Succession Will contents - suggested provisions • Identification of the parties • Statement revoking prior wills • Provision nominating a guardian for minors • Statement directing payment of debts and taxes • Specific dispositions of property • Residuary clause • Statement appointing an executor and trustee • Testator’s signature • Witnesses signatures • Date

Other Issues a). Basis – step up, step down b). Gifting c). Income in respect of decedent d). Sale of residence e). Installment sales and private annuities f). Special use valuation

Federal Gift Tax a). Annual exclusion b). Marital deduction c). Charitable deduction d). Unified credit e). Below market interest rate loans f). Gifts to minors – Iowa Uniform Transfers to minors or trusts

Valuing Property a). Date of death or six months later b). Special Use Valuation based on a capitalization rate, often reduces value at least 25 percent capped at a limit of $1,020,000 reduction for 2011 c). Other discounts for minority shareholders

Federal Estate Taxation Alternate valuation date - requirements: • Available by election • Value of gross estate must decline by making election • Estate’s federal estate tax liability must decline by making election • Gross estate must exceed $ 5,000,000 (for 2011 & 2012)

Gross Estate • Tenants in Common – usually include one-half of the value • Joint Tenants – “consider furnished rule” for non-husbands/wives. “Fractional interest” for husbands/wives

Gross Estate (cont.) 3 year look back rule: a). Life estate b). Transfer was to occur at death c). Revocable transfer d). Transfer of life insurance

Gross Estate (cont.) Retirement Benefits Taxable Gifts after 1976

Gross Estate Deductions a). Debts b). Attorney fees c). Executor fees d). Court costs e). Burial expenses f). Marital deductions g). Charitable deductions h). Iowa inheritance tax i). Part of Federal tax paid in previous 10 years

Estate Planning Zones or the Size of your Pie An estate with a taxable value of less than $5,000,000 An estate with a taxable value between $5,000,000 and $10,000,000 An estate with a taxable value of greater than $10,000,000

Potential Tax Savings • If the “pie” is a small pie (less than • $5 million in 2011) look at impact of inflation and legal costs. • Don’t worry about Federal Estate Tax, focus on income tax issues, possible Iowa inheritance tax, asset protection.

Potential Tax Savings If total “pie” for husband and wife is between $5,000,000 and $10,000,000 consider dividing equally and using life estate or trust.

Potential Tax Savings If you have a “Big Pie” seek specialized help and wait a few years to die. No NONO !!!!! This is your big opportunity Look at special tools to reduce valuation, consider a gifting program, charitable donations, Special Use, minority discounts and other tools estate planners would suggest.