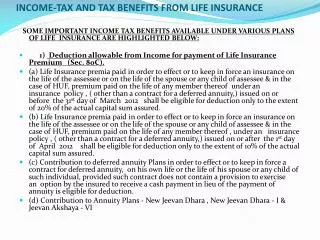

Download

1 / 9

90 likes | 267 Views

Chapter 17. LIFE, HEALTH AND INCOME INSURANCE. How the policies work… How Much Protection Do You Need?… Finding the Right Professionals to Help You. A. Understand Risk and Coping With It B. Why Life Insurance? C. The Basic Elements of Life Insurance

E N D

Chapter 17. LIFE, HEALTH AND INCOME INSURANCE How the policies work… How Much Protection Do You Need?… Finding the Right Professionals to Help You A. Understand Risk and Coping With It B. Why Life Insurance? C. The Basic Elements of Life Insurance 1. Kinds of companies - stock and mutual 2. Par and non-par policies 3. How is life insurance acquired? a. Group plans b. Private plans c. Credit plans Slide 1 of 9

4. Types of life insurance a. Permanent life insurance (whole life, ordinary, endowment) b. Term life insurance c. Universal life insurance d. Annuities 5. The Parties to a Life Insurance Policy a. The insured b. The owner c. The beneficiary d. The contingent beneficiary e. The company Slide 2 of 9

6. The Life Insurance Contract (Policy) and its Clauses a. The application b. Face amount (face value) c. Double indemnity (accidental death) d. Incontestable clause e. Guaranteed insurability f. Premium (payments) and how they are made g. Lapse, grace period and reinstatement h. Waiver of premium i. Conversion values: cashing in, borrowing, extended term, paid-up j. Conversion tables k. Dividend options l. Settlement options Slide 3 of 9

7. Buying Life Insurance: Who Needs It, and How Much? a. Premature death b. Normal life expectancy c. Tax and business purposes d. How much insurance is needed? i. A case history e. What to buy (See Personal Action Worksheet, Text page 510) 8. The Insurance Agent a. Evaluating credentials Slide 4 of 9

D. Insurance When the Risk Might NOT occur E. Health Insurance… A perspective on the vast changes in the health care industry 1. Health Care checklists a. Private insurance b. Managed care - groups, HMOs, etc c. Other forms of protection i. Workers Compensation ii. Coverage in dwelling and auto policies iii. Liability of another person iv. Social Security F. Medicare Slide 5 of 9

G. Income Insurance 1. Existing programs a. Sick pay plans b. Worker’s Compensation c. Social Security d. Unemployment Insurance e. Waiver of premium clauses f. Credit insurance 2. Evaluating your needs for disability income insurance Slide 6 of 9

G. Income Insurance, continued 3. Private disability policies and how they work a. The waiting period b. Total vs. partial disability c. How much protection? 4. Long-term-care insurance a. The waiting period b. Policy limits c. Inflation protection d. Return of premium e. Discounts f. Health Condition H. Medical Savings Accounts (MSAs) I. Health Insurance Portability Slide 7 of 9

You had a health plan at work that covered just about everything. Now the employer wants to switch to an HMO. You can opt for a private plan, and the company will reimburse you for what it costs them to have you enrolled in the HMO. It will cost you well over $1,000 per year more to retain your comprehensive “fee for service” private-type plan. How would you react, in word and deed, to the following information? 1. The HMO is notorious for keeping patients waiting for a very long time. 2. The HMO does not cover all the pharmaceuticals that your private plan did. 3. The HMO will cover you only partially for services and treatments given by providers who are not part of the HMO group. 4. If your HMO family doctor, or “gatekeeper” leaves the scene, another one will take over the job right away. If you private doctor departs, you’d have to start looking for one from scratch. 5. The HMO does have a good reputation regarding its network of specialists, but it often takes a long time to get appointments with them. TALKING POINTS… Chapter Seventeen, Number One Slide 8 of 9

You’re concerned about your parents’ health. They’re not aging gracefully. They are comfortable financially, but would be hard-pressed if serious illness and/or the need for nursing facilities were to strike. Both are still working, but looking forward to retirement. How would you react, in word and deed, to the following possible scenarios? 1. Mother needs to go into a nursing home indefinitely. Dad would have to delay retirement to afford it, and to keep himself in good circumstances. 2. Dad will need full time nursing care at home for a year, perhaps longer. Dad’s income will stop in another month. Mother can only do so much - physically and emotionally - and she can’t afford to go without her paycheck. 3. Mother and Dad can afford long-term-care insurance, which will cover them for the problems of Scenarios 1 and 2 above, but only if they sell their home and move into a small apartment, which would be very stressful to them. 4. You can help them with the long-term-care insurance costs, but it would take a huge bite out of your savings. TALKING POINTS… Chapter Seventeen, Number Two Slide 9 of 9