Download

1 / 21

210 likes | 430 Views

iBoxx CDX.NA.IG The New US Credit Default Swap Benchmark Index. October 2003. The US Benchmark - Themes. Standardization Globalization Flexibility Efficiency. Liquidity Diversification Transparency Innovation. Table of Contents. Setting the New Benchmark 4 Portfolio 7

E N D

iBoxx CDX.NA.IG The New US Credit Default Swap Benchmark Index October 2003

iBoxx CDX.NA.IG The US Benchmark - Themes Standardization Globalization Flexibility Efficiency Liquidity Diversification Transparency Innovation

iBoxx CDX.NA.IG Table of Contents Setting the New Benchmark 4 Portfolio 7 Examples of Trading and Credit Events 15 iBoxx CDX.NA.IG - Portfolio Rules of Construction 19 Contacts 21

iBoxx CDX.NA.IG Setting the US Benchmark • The iBoxx CDX.NA.IG is the New US Benchmark for tradable 5yr and 10yr index products • Liquidity • Proven liquidity track record from the market making group • Multiple market maker platform • Transparency • A transparent rules-based approach to portfolio construction • Standardization • Standardized documentation for unfunded contracts • Standardized documentation for future credit products, e.g. options, tranching • Globalization • The iBoxx CDX.NA.IG is a key pillar in the iBoxx platform • The iBoxx CDX.NA.IG will establish the iBoxx platform as the New Global Benchmark

Rolling Liquidity & Track Record Transparency • Track record in: • CDS flow market • Other credit indexes • iBoxx Notes in Europe • The largest platform of leading market makers • Inter dealer broker participation • Clear rules for portfolio construction* • Pricing via Bloomberg • Standardization and multi-market maker platform to ensure transparency • Active participation of iBoxx Ltd as Administrator • Every six months • One roll mechanism agreed across all market makers • Simple and clear roll mechanism, derived from successful mechanism in Europe iBoxx CDX.NA.IG Key Features Product Breadth Structure Globalization • Standardized documentation • 5 and 10 year maturities • No fees • Static portfolio of 125 diverse names • iBoxx CDX.NA.IG to be the New US Benchmark • iBoxx already established as the benchmark in Europe • Unfunded • Tradable sector swaps • Options** • Tranching** • * See Portfolio Rules of Construction • ** To be released by year end

Market Markers ABN AMRO Barclays Capital Bear Stearns Citigroup Credit Suisse First Boston Deutsche Bank Goldman Sachs Lehman Brothers Merrill Lynch UBS Brokers iBoxx CDX.NA.IG is expected to trade in the broker market Liquidity Ten market makers have already signed on to trade iBoxx CDX.NA.IG Indicative bid/offer spreads on sector swaps are expected to be no greater than [5]% of mid level Transparent pricing screens via Bloomberg Delivery Flexibility Standardized CDS contracts for unfunded trades Sector trading iBoxx CDX.NA.IG Benchmark Liquidity and Tradability • Financials • TMT • Energy • Industrials • Consumer • * For the most current series

Corporate Treasury • Easy access to diversified US risk iBoxx CDX.NA.IG iBoxx CDX.NA.IG • Static portfolio of equally weighted credit default swaps on 125 North American Reference Entities* • Rules based approach to construction • New series of iBoxx CDX.NA.IG issued every 6 months • Suits investors looking for a diversified North American credit portfolio Bank Prop Desks Asset Managers Hedge Funds Media • Quick credit exposure • Liquidity Management tool • Relative value trades • Efficient tool for directional trading • Relative value trades • Efficient tool for directional trading • Captures spread direction and performance of the benchmark index Insurance Bank Portfolio Managers Correlation Trading Desks • Proxy hedge against senior CDO credit portfolio • Suitable for portfolio balancing • Credit diversification tool • Suitable for portfolio hedging • Easy ramp-up • * See Portfolio Rules of Construction

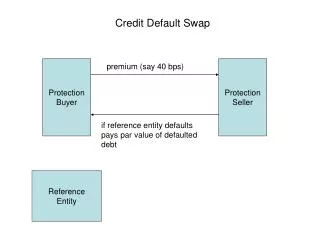

iBoxx CDX.NA.IG iBoxx CDX.NA.IG Indicative terms and conditions • Maturity: 20 March 2009 20 March 2014 • Fixed Rate: [70] basis points per annum. All swap contracts will trade with a Fixed Rate premium with an upfront payment, equal to the present value of the difference between the then current market rates and the Fixed Rate • Credit Events: Bankruptcy and Failure to Pay (2003 ISDA Credit Derivatives Definitions) • During the lifetime of the swap, for each Reference Entity where a Credit Event is deemed to have occurred, there will be Physical Settlement (except under XXmm size as specified in confirm) on that Reference Entity in accordance with the standard procedure for credit default swaps • Credit Event Settlement Method:

Moody's Rating Breakdown * 30% 25% 20% 15% 10% 5% 0% Aaa Aa1 Aa2 Aa3 A1 A2 A3 Baa1 Baa2 Baa3 iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Ratings and Sector Breakdown • * Source: Bloomberg

iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Reference Portfolio Each Reference Entity is equally weighted at 0.8%

iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Unfunded Sector Trading • Key Features * • Static portfolios of credit default swaps derived from the 125 reference entities in the iBoxx CDX.NA.IG providing exposure to the following sectors: • Unfunded / CDS format • Discreet trading for investors • Investors avoid executing large number of small trades • Investors avoid revealing trading strategies • Easy access to outright sector trading • Relative value • Trade one sector against another • Hedge out sectors against the iBoxx CDX.NA.IG • Financials • TMT • Energy • Industrials • Consumer • * See Portfolio Rules of Construction

iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Sector Trading Reference Portfolios (1) • * Weightings are rounded to two decimal places. See Portfolio Rules of Construction

iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Sector Trading Reference Portfolios (2) • * Weightings are rounded to two decimal places. See Portfolio Rules of Construction

The fixed rate of the iBoxx CDX.NA.IG is [70] basis points per annum quarterly After two months, the then current market rate of the iBoxx CDX.NA.IG is [55] bps and counterparty wants to buy $100m iBoxx CDX.NA.IG Exposure CDS is executed at the fixed rate. Market maker pays 70 basis points per annum quarterly to counterparty on notional amount of $100m Present value of difference between fixed rate and current market rate of the iBoxx CDX.NA.IG is settled through an upfront payment on T + [3] days Counterparty pays the present value of [15] basis points per annum on a notional of $100m to market maker iBoxx CDX.NA.IG Trading - Counterparty buys $100m iBoxx CDX.NA.IG Exposure in Unfunded / CDS Form

No Credit Event The fixed rate of the iBoxx CDX.NA.IG is [70] basis points per annum quarterly Market maker pays to counterparty [70] bps per annum quarterly on notional amount of $100m With no Credit Events, the counterparty will continue to receive premium on original notional amount until maturity Credit Event The fixed rate of the iBoxx CDX.NA.IG is [70] basis points per annum quarterly Market maker pays to counterparty [70] bps per annum quarterly on notional amount of $100m A Credit Event occurs on Reference Entity, for example, in year 3 Reference Entity weighting is 0.8% Counterparty pays to market maker (0.008 x 100,000,000)= $800,000, and market maker delivers to counterparty $800,000 principal amount of Deliverable Obligations of the Reference Entity Notional amount on which premium is paid reduces by 0.8% to $99,200,000 Post Credit Event, counterparty receives premium of [70] bps on $99.2m until maturity iBoxx CDX.NA.IG Credit Event - Counterparty buys $100m iBoxx CDX.NA.IG Exposure in Unfunded / CDS Form

Each market maker submitted a list of 150 entities, based on the following criteria: (i) investment grade entities (ii) entities with liquid outstanding debt (iii) entities with active trading in CDS Affiliates of an entity included in the Index that are already guaranteed by that entity are eliminated Non-guaranteed wholly-owned subsidiaries of an entity are eligible Those entities receiving the greatest number of votes are included in the Index until the Index totals 125 entities If on the final iteration there are, for example, 2 places to fill in the portfolio but 15 possible entities (with the same number of votes) to choose from, each market maker will give an order of preference for that list of entities to be included in the new Index. Those entities preferred by the greatest number of market makers are added to the Index until the new Index totals 125 This composition will be the same for the five year and ten year Indexes On the day of the launch, each market maker will submit to the Administrator the fixed rate for the five and ten year Index. The average of these spreads rounded up to the nearest 5 basis points will be the fixed rate iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Construction of the First Index

One week prior to the roll-date, each market maker will submit to the Administrator a list of entities from the current Index which in their judgement should no longer be included, based on the following criteria: (ii) entities downgraded below investment grade by either S&P or Moody’s (ii) entities for which a merger or corporate action has occurred, rendering it no longer suitable (iii) entities whose Credit Derivative Swaps has become materially less liquid. The Administrator will eliminate all entities submitted with respect to (i) all entities submitted with respect to (ii) which receive a majority of votes from the group of market makers all entities submitted with respect to (iii) which receive a majority of votes from the group of market makers Each market maker will then submit to the Administrator a list of entities which in their judgement should be added to the new Index. This list shall include twice the number of entities required Affiliates of entities guaranteed by entities already in the index are ineligible. Non-guaranteed affiliates are eligible The Administrator will add to the new Index those entities receiving the greatest number of votes until the new Index totals 125 entities If on the final iteration there are, for example, 2 places to fill in the portfolio but 15 possible entities (with the same number of votes) to choose from, the Administrator will request each market maker’s order of preference for that list of entities to be included in the new Index. The Administrator will add those entities preferred by the greatest number of market makers to the Index until the new Index totals 125 Three business days prior to the roll-date, the Administrator will publicise the composition of the new Index This composition will be the same for the five year and ten year Indexes Promptly after publication, each market maker will submit to the Administrator the fixed rate for the five and ten year Index. The average of these spreads rounded up to the nearest 5 basis points will be the fixed rate. iBoxx CDX.NA.IG iBoxx CDX.NA.IG - Subsequent Index Composition

iBoxx CDX.NA.IG • Deutsche Bank • Trading Brad Poprik • +1 212 250 2726 • Marketing John Lovisolo • +1 212 250 5672 • ABN AMRO • Trading Arthur Leiz • +1 212 409 7421 • Marketing Joe Duncan • +1 212 409 5358 • Barclays Capital • Trading James Parascandola • +1 212 412 2993 • Marketing xxx • +1 • Goldman Sachs • Trading Alan Gerstein • +1 212 902 0400 • Marketing xxx • +1 • Bear Stearns • Trading xxx • +1 • Marketing xxx • +1 • Lehman Brothers • Trading xxx • +1 • Marketing xxx • +1 • Merrill Lynch • Trading Philippe Hatstadt • +1 212 449 2410 • Marketing Doug Mallach • +1 212 449 6190 • Citigroup • Trading xxx • +1 • Marketing xxx • +1 • UBS • Trading xxx • +1 • Marketing xxx • +1 • Credit Suisse First Boston • Trading xxx • +1 • Marketing xxx • +1