Download

1 / 3

30 likes | 231 Views

After graduating, the struggle to repay loans stress students. Many students pay hundreds of dollars each month for repayment of loan. In fact many end up paying more money to repay college debts than they pay for daily expenses.

E N D

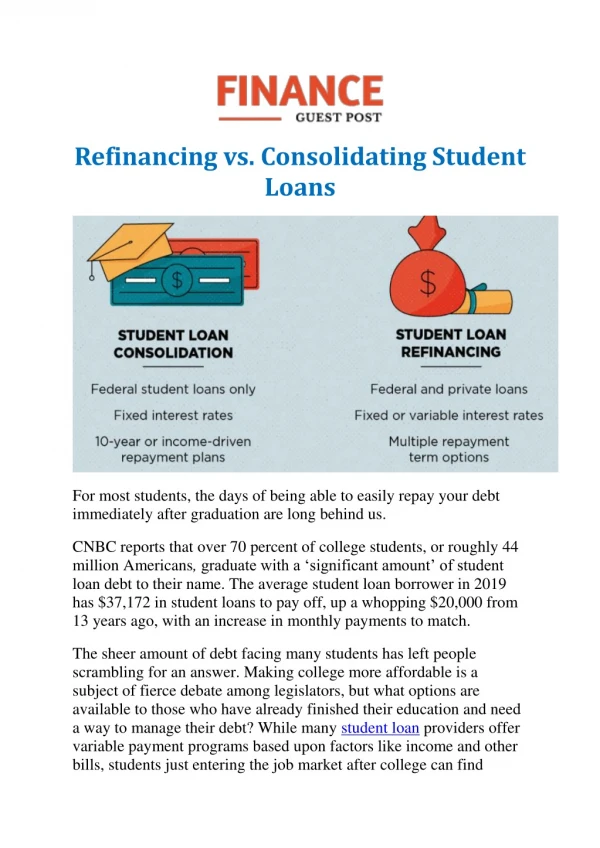

Consolidating student loan often confused with refinancing. After graduating, the struggle to repay loans stress students. Many students pay hundreds of dollars each month for repayment of loan. In fact many end up paying more money to repay college debts than they pay for daily expenses. If you are liable to pay more than one student loan, consider consolidating your student loans. Consolidation is one of the best ways to ease financial pressure. Consolidating student’s loan is the process where multiple loans are clubbed into single loan. You then are liable to pay the one larger loan. However consolidation is often confused with refinancing, the terms are definitely going to leave you confused. You may have been wondering, “Should I consolidate mystudent loans?” before that know the myths of student loan consolidation. Myth 1: It’s considered that loan refinancing and consolidation is one and the same. (Truth: Both terms are similar, but there are differences that are important to know.) “Consolidation” and “refinancing” are often confused as same, but they are two different repayment options. Consolidation generally clubs your multiple federal loans into one. It is done through federal government. Consolidating loan makes your monthly payment simpler and you can also get access to more favorable repayment plans or forgiveness programs. Refinancing student loan means you take a totally new loan, one with lower interest rate to repay the debts of existing loans. Refinancing and consolidation goes hand in hand for private loans and that the very reason for people’s confusion. For federal loans that’s not the case. If you decide to refinance your federal loans through private lenders, be prepared to lose all federal loan benefits. Myth 2: private loan and federal loan has same consolidation process. (Truth: Both the loans consolidation process is different from each other)

Government processes federal student loan consolidation whereas private loans are consolidated through private lenders. You might have taken both private loan and federal loan and you may also consider of consolidating federal and private loans together, but to consolidate them into one loan is a rare advice anyone will give. You can consolidate your federal student loans by applying for federal direct consolidation loan on the website Federal Student Aid. Consolidation do not lower your interest rate, no doubt interest rates are fixed. They are calculated by taking a weighted average of the interest rates of the all the loans you’re consolidating. Private loan consolidation is very different from federal loan consolidation. For consolidating private loan you need to apply for a new loan that will help you pay your existing loans. Your potential lenders will evaluate you on the basis of your credit history and, if you qualify, they will make an offer. Myth 3: People believe that consolidating student loans involves very little mental effort. (Truth: Student loan consolidationisn’t appropriate for every person.) If you owe multiple federal student loans, one of the best options is federal loan consolidation. You can organize your multiple interest rates, terms and loan servicers into one monthly payment. But consolidation isn’t for everyone, There are benefits of federal student loan consolidation; you can have access to repayment option. Federal loan consolidation can be beneficial if you need to do it to access a repayment option and forgiveness programs. To avail these benefits the borrowers should have federal direct loan. Consolidating your loans means paying more interest over time, as the loan term lengths from 10 to 30 years, depending on your loan balance. The term will be longer if your loan amount is larger. No doubt the longer term will reduce your monthly payment but will increase the amount of interest you will pay. Even though you have long term consolidation loan, you can pay off early and there is no penalty charged. The aim should be always to pay off loans as early as possible to save the most in interest.

Myth 4: Refinancing of federal student loan can be done through federal government. (Truth: refinancing of student loan is offered by private lenders only.) Refinancing of both federal and private student loans can be done only by private lenders. Though federal government offer student loan, but refinancing of student loan is not offered by them. Refinancing is always done through private lenders No matter which way you go, refinancing of federal student loan will ultimately become a private loan. That will make you lose the benefits of federal loan like income-driven repayment plans, forgiveness programs, and deferment and forbearance. Myth 5: Consolidating of federal student loans, costs money. (Truth: federal student loan consolidation is free; you shouldn’t pay third party Company to do it for you) Federal government consolidates your federal student loan for free. But there are companies that try to charge you for consolidation process. To avoid getting involved with a crooked student loan consolidationcompany, don’t give out your Federal Student Aid (FSA) ID, and don’t send your loan payments to a third-party company. These are some of the myths of consolidating, which always tend to confuse people with refinancing. Contact Bruce mesnekoff for any further assistance