Download

1 / 3

30 likes | 38 Views

Generally, water claims are covered by insurance but such damage is not paid easily by insurers. Your insurer will investigate whether or not you had the heat on if the loss occurred in the winter. No heat - no payment.

E N D

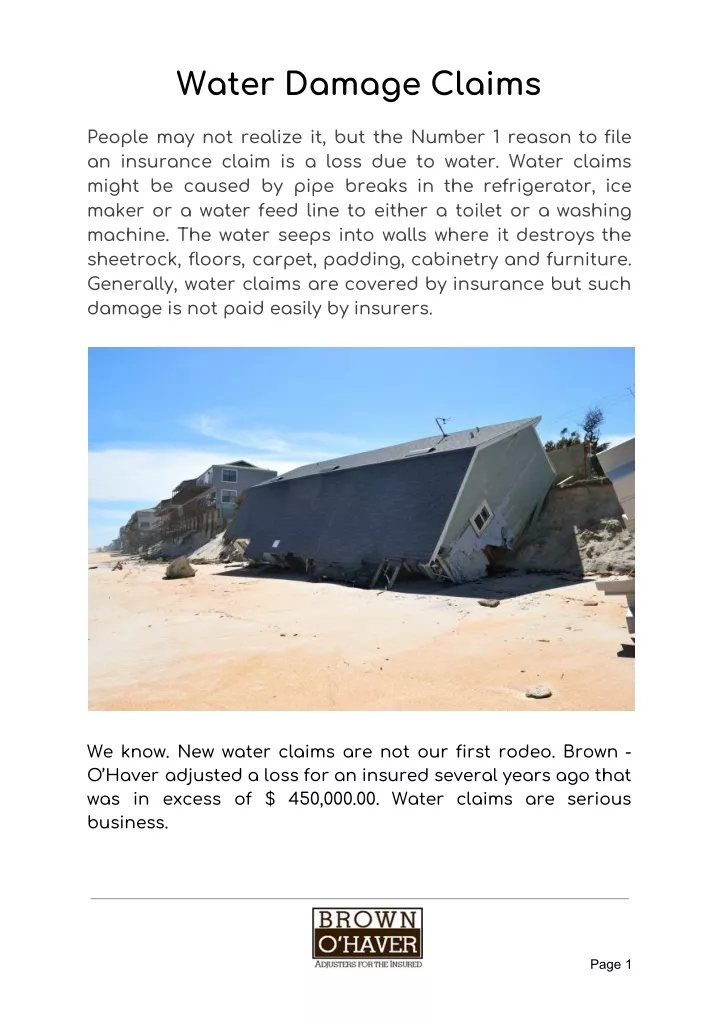

Water Damage Claims People may not realize it, but the Number 1 reason to file an insurance claim is a loss due to water. Water claims might be caused by pipe breaks in the refrigerator, ice maker or a water feed line to either a toilet or a washing machine. The water seeps into walls where it destroys the sheetrock, floors, carpet, padding, cabinetry and furniture. Generally, water claims are covered by insurance but such damage is not paid easily by insurers. We know. New water claims are not our first rodeo. Brown - O’Haver adjusted a loss for an insured several years ago that was in excess of $ 450,000.00. Water claims are serious business. Page 1

Suppose your water pipe breaks and floods your home. Your insurer will investigate whether or not you had the heat on if the loss occurred in the winter. No heat - no payment. Another hassle in presenting a water claim deals with an event caused by a pipe break while you are away. The insurer will look to see if the damage is “long term” since long term damage and maintenance insurance policies. If a water loss occurs when you are on vacation and your home is vacant, that loss should be covered. However, we have seen a new development in the insurance adjusting business where insurers are challenging insureds over the length of the insured’s absence. The reason for this is because the policy of insurance generally denies coverage for those maintenance issues and “long term” damage. When did the loss actually occur? At Brown - O’haver we have developed several methods in dealing with water losses and we are generally successful in presenting an insured’s claim. In asking when the loss occurred, we check to see when a water bill might have increased or use other forensic methods. At the beginning of the year we adjusted a claim for a “snow bird” who lived away from his Arizona winter home and returned to Arizona only when his home state was frozen over. The insurer in that case concluded that the damage to his Arizona home was caused by vandalism. Someone, the insurer concluded, had opened the water pipes allowing water to destroy the home. And, I mean “destroy”. The Park Model Trailer was a total loss. The insurer denied the claim because vandalism was not covered under the conditions of are issues not covered by Page 2

the policy and the facts surrounding the loss. The insured contacted Brown - O’Haver. We stood back and asked, so what if the home was vandalized? The pipes in the home would still hold any water intrusion. We arranged for a plumbing expert (paid for by the insurer, of course) who found interior pipe breakage. The seventy-five year old insured is now a fervent supporter of Brown - O’Haver. Our work for him literally saved his way of life. And that brings us to whether or not mold is covered. Mold often occurs as a result of a water loss. Some insurers, such as State Farm, will not cover any type of mold. Other insurers might offer relatively small coverage on mold claims but give you the option of purchasing additional coverage. All policies are different but Brown - O’Haver will review your policy with you at no cost to see what coverage is provided. Given that water damage claims are the number one cause of insurance claims, independent insurance claim private adjuster would be our recommendation that you contact your agent BEFORE a loss to make certain that you have an adequate amount of water and mold insurance. it Page 3