Download

1 / 6

60 likes | 312 Views

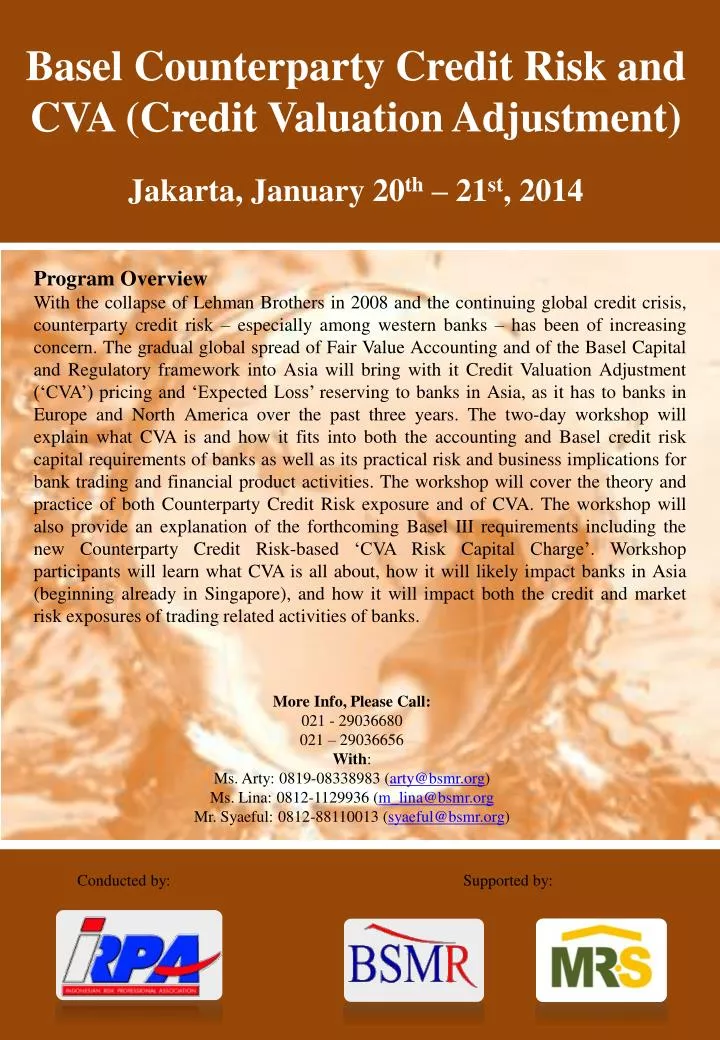

Basel Counterparty Credit Risk and CVA (Credit Valuation Adjustment) Jakarta, January 20 th – 21 st , 2014. Program Overview

E N D

Basel Counterparty Credit Risk and CVA (Credit Valuation Adjustment) Jakarta, January 20th – 21st, 2014 • Program Overview • With the collapse of Lehman Brothers in 2008 and the continuing global credit crisis, counterparty credit risk – especially among western banks – has been of increasing concern. The gradual global spread of Fair Value Accounting and of the Basel Capital and Regulatory framework into Asia will bring with it Credit Valuation Adjustment (‘CVA’) pricing and ‘Expected Loss’ reserving to banks in Asia, as it has to banks in Europe and North America over the past three years. The two-day workshop will explain what CVA is and how it fits into both the accounting and Basel credit risk capital requirements of banks as well as its practical risk and business implications for bank trading and financial product activities. The workshop will cover the theory and practice of both Counterparty Credit Risk exposure and of CVA. The workshop will also provide an explanation of the forthcoming Basel III requirements including the new Counterparty Credit Risk-based ‘CVA Risk Capital Charge’. Workshop participants will learn what CVA is all about, how it will likely impact banks in Asia (beginning already in Singapore), and how it will impact both the credit and market risk exposures of trading related activities of banks. More Info, Please Call: 021 - 29036680 021 – 29036656 With: Ms. Arty: 0819-08338983 (arty@bsmr.org) Ms. Lina: 0812-1129936 (m_lina@bsmr.org Mr. Syaeful: 0812-88110013 (syaeful@bsmr.org) Conducted by: Supported by:

What will participants learn? Participants should finish the two day workshop not only with an understanding of CVA and its challenges and complexity, but with an understanding of how to practically deal with it as it spreads into the ASEAN markets, beginning now with Singapore. Indonesian banks, because of Bank Indonesia’s role in the Basel Committee on Banking Supervision, will be impacted at some point in the future. Very few banks have the complex systems required to incorporate CVA valuation and risk management easily into their current infrastructure so a number or practical implementation ‘shortcuts’ or approximation techniques are generally required. The workshop will cover such methods as well as giving the participants a deeper understanding of both the underlying bank market risk and credit risk measurement frameworks which CVA in its various aspects overlaps. Workshop Results To provide the workshop participants with a good and detailed understanding of the theoretical and practical aspects of: • Pricing and managing CVA from a business perspective (including shortcuts used for come calculations); • Accounting & Basel Capital Framework aspects of CVA and recent developments / challenges in both areas for banks (such as ‘DVA’ in accounting, and the new Risk Capital Charge required beginning in 2013 under Basel lll); • The challenges posed by calculating the counterparty Exposure at Default (EAD) of CVA on a ‘Netting Set’ basis, and which Probability of Default (PD) should be applied ‘risk neutral’ or ‘actuarial’; • The asymmetrical nature of CVA risk when compared to other forms of market risk exposure (notably Trading Book VaR) and the risk management challenges posed by CVA • TargetGroup • The workshop is designed at an intermediate to advanced level, and intended to be of particular benefit to members of bank: • Risk Management Departments (both Market & Credit Risk professionals) responsible for assessing and managing both the credit and market risk exposures of CVA; • Treasury / Financial Markets Division – both Trading and Sales professionals who are, or will be, confronted with pricing and managing CVA on a daily basis; • Finance / Accounting / Middle Office professionals tasked with the re-valuing, reserving and reporting CVA; • Banking professionals and consultants involved in Basel III implementation, impact analysis and capital planning; • Present or Future ‘CVA Desk’ managers and bank managers and academics interested in emerging issues challenging the banking system.

Outline of the Workshop Program Day 1 – Morning Session: Counterparty Exposure Management Basics & Credit Valuation Adjustment’s (‘CVAs’) Role: • The Credit Crisis of 2007-2009 and Counterparty Exposure and Its Dramatic Impact on Counterparty Credit Risk. • What is CVA and How Will It Impact Banks in Asia? How does it it Into Counterparty Credit Exposure Measurement? • The Three Pillars of Counterparty Credit Risk (‘CCR’) Exposure Measurement & Management • Counterparty Exposure Limits (a form of Credit VaR calculation) • Counterparty Exposure Capital (Basel II / III coverage of Unexpected Loss) • Credit Valuation Adjustment (Basel II Expected Loss / Basel III credit migration risk surcharge / Accounting ‘fair value’ asset adjustment reserve) • CCR Exposure Measurement Tools and Concepts: • Credit Risk: Probability of Default (‘PD’) & Loss Given Default (‘LGD’) • Contingent Market Risk: Exposure-at-Default (‘EAD’) • Potential Future Exposure (‘PFE’) • Expected Exposure (‘EE’) & Expected Positive Exposure (‘EPE’ and ‘EEPE’) • Maturity Factor • CVA as Expected Loss – the Basic Calculation (PD * LGD * EAD * M) • Key CVA Issues: • Accounting – IAS & FASB Accounting Requirements (Fair Value Accounting) • CVA Pricing – Will it Become a Competitive Factor for Client Business? • CVA Reserves Management – P&L Volatility Based on Market and Credit Risk Factor Exposure (Interest Rates, FX Rates, Credit Spreads and Rating Migration Risk) • Correlation and Wrong-Way Risk Day 1 – Afternoon Session: CVA Pricing: Contingent Market Risk Component (‘EAD’ based on ‘EPE’) • Bilateral, OTC Derivatives as Asset & Liability – MTM Valuation + Future Exposure • CVA Market Risk Exposure Calculation – EAD = MTM + EPE Explained • Estimating the EPE Profile of an Interest Rate Swap and FX Forward / Option • Counterparty Exposure with Netting (ISDA Master Agreements) • Counterparty Exposure with Collateralisation (ISDA Credit Support Annexes) • Calculation of EPE on Complex Transactions and ‘Netting Set’ Exposure - Monte Carlo Simulation and Expected Exposure (EE) • EAD Calculation Methods Under Basel ll (Current Exposure Method, Standardised Method and Internal Model Method calculation of EAD)

Day 2 – Morning Session: CVA Pricing (Valuation) Challenges: • Probability of Default (‘PD’) • Actuarial / Objective PD (Historical, Ratings-based) vs. Risk-Neutral PD (‘CDS’-based) – What is the Difference and Why? • When to Use Actuarial vs. Risk-Neutral PDs • How to Derive Actual & Risk-Neutral PDs (Maturity PD vs. Marginal PD) • Pricing CVA on an Actuarial or Risk-Neutral PD Basis • Pricing the CVA on a New Transaction • Pricing CVA on a Single Transaction or Incremental (‘Netting Set’) Counterparty Exposure Basis • Expected Loss vs. Unexpected Loss • CVA versus DVA (or Bilateral CVA) • CVA as a Credit and Market Risk Sensitive Value • When and How to Recalculate the CVA on Existing Counterparty Transactions / Portfolios • Expected Loss vs. Unexpected Loss • Using Economic Capital or the Basel ll – IRB Alpha Granularity Adjustment • Pricing in CDS Hedging Transaction Costs • Why are transactions priced so differently? Is it CVA alone? Role of Funding Costs – Post 2007-2009 Credit Crisis Day 2 – Afternoon Session: Managing CVA Reserves Volatility & Risk Capital (CVA as an Important Component of both Credit and Market Risk) • Why CVA Needs to Be Managed – P&L versus Reserves & CVA Market & Credit Risk Sensitivity • Who will Own Counterparty Exposure Risk in the Bank and Who Should Manage CVA (Front Office / Risk / Finance)? Is CVA Pricing & Management a Profit Centre or Utility Function? Putting CVA Together With OTC Derivatives Portfolio Funding Pricing & Management? • Managing CVA – Banking / Insurance Approach and / or Market Trading / Hedging Approach • Managing CVA-based P&L Volatility Under the Banking / Insurance Approach (Credit Risk Default Premiums + Market Contingent Risk Profile Hedging) • Managing / Hedging CVA Under the Trading / Hedging Approach • Number of Participants • We require a minimum number of 10 participants for this Workshop. • Language • The Workshops will be conducted in English. Workshop material will be in English.

Location • Le Meridien Hotel Jakarta* • Jalan Jenderal Sudirman, Kav 18 - 20, Jakarta 10220 Workshop Fees The fee for the Workshop, including all material, drinks and lunches, during the Workshop days will be Rp. 9.500.000,- for each individual participant. Hotel and travel expenses are not included. Certificate All participants will receive a certificate from IRPA registered at BSMR. About the Workshop Leader Douglas Bongartz-Renaud is currently the director of Markets & Risk Solutions Pte. Ltd, and has over 30 years of experience in the Financial Markets and Services Industry. He used to be an Executive Director in the Markets Division with ABN AMRO in Amsterdam, with a focus in working on behalf of the front-office with other areas of the bank to improve the pricing of credit valuation adjustment (CVA) in transactions, and the management of CVA reserves, in connection with the Bank’s active OTC derivatives business. Douglas headed the Treasury, ALM and market risk team in ABN AMRO’s Risk Advisory Service business, which was engaged in projects with over 40 banking clients in Asia and the EMEA region. His client-based advisory and implementation work covered Treasury and Investment Banking; Market Risk Management; Asset and Liability Management. Before doing client-based project work in the Risk Advisory Unit, Douglas established and co-headed a new group within the bank’s Global Risk Management Department responsible for interfacing directly with the Financial Markets Division to expedite risk review and approval of complex derivative and new product related transactions. In that role he assisted Financial Markets in accelerating its business growth in several key areas, including exotic credit and correlation products, esoteric (inflation, insurance, weather, etc) and commodity derivatives, complex rate and hybrid derivatives, dynamic guarantees (CPPI transactions). Douglas had many other senior trading and product management positions in ABN AMRO’s Financial Markets and Treasury Department from 1985 through 2004, including, Global Head of Currency Derivatives Trading, Structuring & Distribution, Global Head of Structured Products Trading & Derivatives Product Development, Global Head of Swaps & Options Trading. Douglas is a member of the GARP (and holds the ‘FRM’ certification) and of the PRMIA risk associations, and served on the ISDA (International Swaps and Derivatives Association) Board of Directors from 1994 to 2008, (and was Secretary of the Association from 1998 to 2004). He is the Director of Markets & Risk Solutions Pte. Ltd. and provides Consultancy to banks in the areas of ALM, Treasury and Risk Management.

REGISTRATION FORM • Basel Counterparty Credit Risk and • CVA (Credit Valuation Adjustment) • Jakarta, January 20th – 21st, 2014 Workshop Fee: Rp. 9.500.000,- / participant Name : BSMR ID No. : Institution : Title : Office Add. : Phone No. : Contact Person: Email Add. : Date: signature Off: Cell: Name: Telp: • Group booking from thesame institution attending thisseminar will get discount. • 2 participants: 5% discount • 3 participants: 7,5% discount • > 3 participants: 10% discount • Cancellation Policy: • The fee is non-refundable • Please transfer the workshop fee to: • BadanSertifikasiManajemen Risiko • BRI Jakarta Pondok Indah Branch • Acct. No.: 0362-01-000647-303 • Please complete this registration form and fax to: 021-29036681 / 021-29036657 • Telp: 021 – 29036680 / 021-29036656