Download

1 / 49

490 likes | 823 Views

Global Healthcare Trends Presentation to IBM Public Sector Leadership Forum. Friday, February 7, 2003 Presenter: Neil Stuart, IBM BCS Canada. Overview of Presentation. Purpose of presentation: to provoke thinking about the future needs of our clients/customers and opportunities for IBM

E N D

Global Healthcare TrendsPresentation to IBM Public Sector Leadership Forum Friday, February 7, 2003 Presenter: Neil Stuart, IBM BCS Canada

Overview of Presentation Purpose of presentation: to provoke thinking about the future needs of our clients/customers and opportunities for IBM • The big trends • Some potential surprises • Implications for our customers/clients • Developments in the market • Opportunities for IBM

Thought Leadership – Lots Done, More to Come • Futures analysis • PricewaterhouseCoopers’ HealthCast 2010, and HealthCast Tactics • E-Health Transformation – PWC Europe • IBM’s Healthcare 2012 • More in the works • Multi-client study on payor operations/performance in U.S. • Canadian POV – Health on demand

The Big Trends • More demanding, better informed consumers • Genomics • E-world • Demographic change • Financial sustainability of healthcare coverage • Human resources concerns • Evidence based-practice • Patient safety

Consumers will be a Continuing Story • Consumers are and will be transformed by • New attitudes – demanding and aging boomers, paying for a bigger part of their care • New expectations – a voice, choice, personalized care, partnerships with providers • New tools – report cards, patient charters, personal electronic health records • The Internet - information, new knowledge, much greater health literacy and new models of accessing services • Genetic foresight – knowledge of their own genetic futures • Demand driven healthcare • Consumer-inclusive solutions • Health organizations that do not get it will fall behind

Genomics, a Sleeping Giant • Accessible genetic testing • Individual awareness of our genetic futures • Longer disease life cycles and greater demand/costs • Demand for new kinds of preemptive services • Gene specific, designer drugs • Much more effective drug therapy • Huge cost escalation • Consumers anxious about their genetic futures • Greatly increased clinical precision and clinical complexity • Much greater density of clinical information • Costs pressures

E-world - Larger Markets, Extended reach for Healthcare • E-delivery of services • Remote diagnostics, specialist consultations, even remote surgery! • Remote monitoring of chronic conditions • Teletriage • E-mail primary care consults • Information, appointments, test results, prescriptions, referrals • Electronic health records • E-markets and e-purchasing • Increasing the reach of providers • Globalization and blurring of old health jurisdictions • Patient access to EHRs giving consumers one more lever to increase control • Scale challenges for suppliers

The Sustainability Question • Multiple pressures on the the cost and affordability of healthcare • Demanding consumers • Demographics – aging population • Expensive drugs that work even better • Costs of new technologies - IT, Dx, Rx • Costs of updating old infrastructure/facilities • Healthcare consuming ever larger part of government spend – ‘the healthcare monster’ • Opportunities for new players and the private sector • Increasing health inequities • Focusing resources on interventions that produce outcomes • Pressures in the U.S. for a national health plan

The “Healthcare Monster” – a headache for governments and payors that will not go away “The rising cost of healthcare has brought on a fiscal crisis in many (U.S.) states. Their combined budget deficit is estimated to worsen to $60 - $85B in 2004, which is equivalent to 13 – 18% of their total expenditure.” -- Kaiser Family Foundation, January 2003

Potential Surprises • Prolonged war in the Middle East leading to an economic downturn • Taking money from health budgets, particularly capital budgets • Massive bio-terrorism offensive against major ‘Western’ cities • Diversion of health resources • Globalization of infectious disease continues – West Nile, Mad Cow, etc. • Global health surveillance and collaboration • Increasing numbers/prevalence of drug resistant disease strains • Return of long inpatient stays, isolation care • Sooner than expected breakthroughs on gene therapy • New ball game • Surprises always reveal new needs/gaps (think of HIV, anthrax) • Look ahead, spot the customer need, respond smartly and quickly

Four BIG PICTURE business directions for our customers/clients • Managing demand for services • Measuring, managing and paying for performance • Providing ready access to health information • Making health care organizations employers of choice

1. Managing demand for services • Consumerism is changing the way clinical/service decisions are made – decisions no longer just with providers • Concerns about sustainability and overwhelming growth in demand • Strategies to manage demand and channel consumerism • Partnerships with patients/users • Matching providers and patients and team based care • Informing and educating patients • Tools for self-monitoring, self-care, self-service • Devices that offer/require choice, e.g. defined contribution plans, MSAs • Taking advantage of of opportunities for e-service • Disease management – focusing on chronic diseases (cancer, diabetes, asthma, cardiac, etc)

Employer-driven Insulated consumer Defined benefit/limited choices No decision making tools Full service health plans Antiquated business infrastructure Member-driven, with member more financially accountable Movement toward defined contribution Emergence of assisted decision making More specialized health plan focus Flexible technology infrastructure Emergence of non-traditional competitors For U.S. health plans, the need to address costs and consumer demands will fundamentally alter their role TODAY FUTURE Employer Employer The Pain Transplant $ Benefits Consultant/Broker Employee Banks/ Financial Institutions $ Employee Health Advisor/Broker Health Plan A Health Plan B Health BenefitPackage Health Plan C Insurance Network TPA Care Mgmt Other

1. Managing demand for services • Some relevant IBM offerings • CRM • Payor systems, including outsourced services (Empire-Blue Cross-U.S.) • Consumer surveys (HealthInsider-Canada)

2. Measuring, managing and paying for performance • To date there has been little financial reward for quality and service excellence • Escalating costs and concerns about sustainability highlight the importance of focusing resources for maximum impact • Research on preventable errors is underlining concern re patient safety • Some actions that will shift more attention to performance include: • Developing and implementing patient safety and quality indicators • Measuring and rewarding for patient satisfaction • Giving quality incentives to service providers • Informing stakeholders on what works and what is excellent • Transparent resource allocation • Payor concerns with efficiencies • Paying attention to system performance too

2. Measuring, managing and paying for performance • Some relevant IBM offerings • Data warehousing • Many BCS assignments on report cards (Canadian Institute for Health Information) • Program evaluation • Consumer surveys – e.g. IBM HealthInsider • Addressing payor performance

3. Providing ready access to information • Access to health information to support the patient care process is slow and fragmented • Inadequate access to information has been an impediment to evidence-based practices and linked to patient safety issues • Strategies to support ready access to useful information include: • Point-of-care computing • Ensuring privacy and security • Setting realistic timetables • Developing open, flexible architectures • Investing in data warehouses and performance monitoring metrics • Providing ongoing training • Patient access to and even control over their EMR • Consumer access to system/provider performance information

3. Providing ready access to information • IBM’s offerings • HIPAA work in U.S. • Vendor alliances e.g. Cerner • Healthcare integration e.g. Alberta we//net

4. Making health care organizations employers of choice • Health care organization used to be a prized place to work - - security, helping people, status • New entrants to the job market are looking for other features to their work - - flexibility, team-based, learning/development opportunities, state-of-the-art technology • Some strategies to make health care organizations a work place of choice • Flatter organizations – pushing decision making down the hierarchy • Career options/development/training • Team environments • B2E/employee portals • Flexible pay and benefits • Linking employee and patient satisfaction • Above all, respect for employees

4. Making health care organizations employers of choice • IBM’s offerings • BCS’s Human Capital Solutions, including Learning Solutions • Examples of assignments completed (hospitals as employers of choice, HR retention) • B2E portals

Some nearer-term market trends • Consumer driven health plans • Wireless/mobile solutions (mainly from established vendors) get traction • Growing use of web in healthcare supply chain • Convergence of electronic physician order entry and e-procurement • Outsourcing takes off – offered by vendors – an answer for customers’ lack of capital • Healthcare spending on outside IT services surpassing internal IT spend • Healthcare IT spend will have to a show strong business case • IT will be seen more as answer for human resource shortages

IT Opportunities for IBM* • Consumerism and demand management drive CRM • CRM opportunity will grow 25% from 2003 to 2006 • E-world drives SCM opportunity, e-markets and e-procurement • 20% plus growth rates projected in SCM and e-markets for IBM • Services are the biggest IT opportunity • Services are the largest and generally fastest growing segment of opportunity by geography and solution market * Source of projections: IBM Market Intelligence – Sales & Distribution

IT Opportunities for IBM (more…..) • Mobile computing • Implementation – application vendor alliances • Security issues • Hardware – product to compete with Compaq/HP, Microsoft, Palm? • Outsourcing • Payer systems, claims management, back office, PC/network support • Privacy and security • US market being driven by HIPAA, parallel interest in other jurisdictions • Healthcare integration • E-business integration, portals, B2E, B2B, B2C • Business on Demand, Information on Demand, Healthcare on Demand

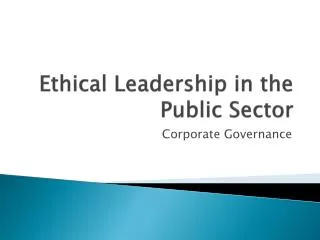

Healthcare Solutions by Geo and Solution: CRM and ERP are Largest Opportunities

Healthcare Solutions by Geo and Solution: CRM and ERP are Largest Opportunities

Total WW Healthcare Sols Opportunity 2003 (Large Enterprises) $6.8B

Total WW Healthcare Sols Opportunity 2003 (Large Enterprises) $6.8B

Total WW Healthcare Sols Opportunity 2003 (Large Enterprises) $6.8B

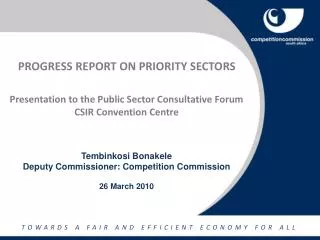

CRM Has Highest Growth Rates in Geos, While ERP Has Lowest Growth

CRM Has Highest Growth Rates in Geos, While ERP Has Lowest Growth

CRM Has Highest Growth Rates in Geos, While ERP Has Lowest Growth

Services is Largest Solutions Opportunity in Americas for CRM, ERP and SCM

Services is Largest Solutions Opportunity in Americas for CRM, ERP and SCM

Services is Largest Solutions Opportunity in Americas for CRM, ERP and SCM

Services is Largest Solutions Opportunity in Americas for CRM, ERP and SCM • Services (SI, IT Consulting, Bus. Consulting, Other Services) total 73.2% of Americas CRM oppty, 69.3% of ERP oppty, and 73.5% of SCM oppty • HW (Servers, Clients, Technology) is a relatively small portion of Americas solutions oppty (8.2% for CRM, 16.8% for ERP, 8.2% for SCM) • CRM, ERP and SCM Apps SW are relatively small portions of total Americas solutions oppty (15.2% to 18.1%), but will drag many Services purchases • SI is the largest segment of Americas SCM oppty (40.5%), more than double the percentage for CRM and ERP

Services is Top Opportunity for CRM, ERP, SCM in EMEA • Services (Bus. Consulting, IT Consulting, Other Services, SI) is largest part of all 3 EMEA solutions opportunities: 72% of CRM, 59% of ERP, 83% of SCM • HW is a small part of CRM, ERP, and SCM opportunities in EMEA: 14% of CRM, 16% of ERP, 6% of SCM • SI is much larger part of EMEA SCM oppty (50.9%) than for CRM (24.2%) and ERP (16.2%) • Application SW is a relatively small part of EMEA solutions opportunities (13.1% of CRM, 21% of ERP, 8.8% of SCM), but drags through many services dollars

Services is Top Opportunity for CRM, ERP, SCM in AP • SCM is largest solutions oppty in AP ($125M in 03), and SI is largest single segment of the AP SCM oppty (36.8%) • Services (Bus. Consulting, IT Consulting, Other Services, SI) are largest oppty for solutions in AP: 76.5% of CRM, 62.1% of ERP, 63.2% of SCM) • HW (Clients, Servers, Technology) is relatively small segment of AP solutions oppty: 12.1% of CRM, 13.5% of ERP, 20% of SCM • Applications SW is relatively small part of AP solutions oppty (10.4% of CRM, 18.9% of ERP, and 13.6% of SCM), but drags other IT dollars

Solutions Definitions: Customer Relationship Management (CRM) • Customer Business Goal: • Increase customer loyalty • Increase profitability • Increase productivity • Gain competitive edge through access in new sales, service and marketing channels • Business problems/functions addressed: Improve the analysis and understanding of the customer preference & purchasing behavior across the CRM value chain including the marketing, sales and service functions aimed at providing direct personalized customer sales, service and marketing activities through multiple channels or "touchpoints" • High level definition: CRM encompasses the business processes an enterprise performs to identify , select , acquire , develop and retain its customers through multiple communication channels. I/T functions involved: • * Focused Definition: Sales Force Automation, Customer Service & Support (including eService and contact center), Marketing automation (including analytical and content mgmt capabilities), Voice Interaction, Text Interaction and Multimedia Interaction • Exclusions: *Generic business intelligence *Telephony based hardware *Billing and payments *ATMs and ATM networks, * Reservation and ticketing systems *Internal help desks * Store operations • Inclusions: * Market information retrieval * Sales transaction initiation • Examples in products and players: Siebel, PeopleSoft, Oracle, SAP, Onyx, Pivotal, Nortel, Avaya, Accenture, PWC, CGE&G, Deloitte, KPMG, eLoyalty etc.

Supply Chain Management (SCM) • Customer Business Goal: The Supply Chain Management solutions allow customers to improve responsiveness, lower cost, reduce cycle time by optimizing internal logistics and by linking suppliers and trading partners to deliver the right products at the right time and price to the right place. • Business problems/functions addressed: Sourcing, distribution, warehousing and transportation, Production logistics, Customer order fulfillment and services, Forecast and demand planning High level definition: A. Focused definition -- Linking two or more I/T applications and functions supporting the supply and production of goods. B. General definition -- I/T applications and functions supporting the supply and production of goods. I/T functions involved: A. Supply Chain Planning: 1) Forecast and Demand Planning, 2) Distribution and Warehouse Planning, 3) Manufacturing Planning, 4) Transportation Planning, 5) Advanced Scheduling, 6) Order Promising, 7) Data Integration B. Supply Chain Execution: 1) Order Management, 2) Order Promising, 3) Inventory Management, 4) International Trade Logistics, 5) Transportation Management, 6) Warehouse Management Exclusions: Shop floor operations, Retail store operations, Retail electronic media distribution, Retail electronic order Inclusions: Supply Chain Automation (SCA), Electronic internal distribution, Content of Utilities (phone, water, electricity) Examples in products and competitors: A. ERP Vendors: SAP (Scope), Baan, Oracle, PeopleSoft B. Supply Chain Planning Vendors: i2, Manugistics, ILOG SA, Logility, Adexa C. Supply Chain Execution Vendors: IBS, EXE Technologies, IMI, Manhattan Associates, McHugh Software International D. Processware Vendors: CrossRoute, CrossWorlds. E. Consulting and System Integrators: Andersen Consulting, Arthur Andersen, E&Y

Definition: B2B-eProcurement • Customer Business Goal: B2B eProcurement enables ·buy-side, sell-side, and content management solutions allowing an entity to obtain information, create a request that can be routed for approval, issue a purchase order to a supplier, and fulfill the request with a receipt, receive notification of delivery or order status, together with electronic means to settle the payment. In addition eProcurement allows automation of the process of connecting to business buyers, and·the automation of the presentation layers of B2B sites, especially for displaying commerce-oriented information. • Business problems/functions addressed: Sourcing, distribution, warehousing and transportation, Production logistics, Customer order fulfillment and services, Forecast and demand planning High level definition: • eProcurement is the element of B2B functions that handles policy control, business workflow and rule compliance, B2B content management, and catalog conversion in buy-side and sell-side electronic purchases between businesses, their suppliers, and customers over the Internet. • I/T functions involved: • Policy control, • Business workflow and rule compliance, • B2B content management, • Catalogue conversion in buy-side and sell-side electronic purchases between businesses and their suppliers over the Internet • Exclusions: • Inclusions: Examples in products and competitors: • Ariba, Commerce One, Oracle, i2, Broadvision, SAP, Vignette, MRO Software, PurchasePro, WebMethods

B2B - eMarkets • Customer Business Goal: B2B are the business process solutions that enterprises use to identify, select, acquire, develop, interact, and retain its business customers through multiple communication channels. These business process solutions can be further defined by the solution areas, Supply Chain Management (SCM), e-Procurement, Partner Relationship Management, and Business Intelligence (BI), etc. These solutions can be implemented as inter-enterprise solutions, or as a part of a broader e-Marketplace in either Private or Public forms, allowing for one-to-one, one-to-many or many-to-many connections. • Business problems/functions addressed: Solutions that allow the creation of Web-based eMarketplaces, public and private, allowing for one-to-one, one-to-many, or many-to-many connections.. High level definition: • B2B eMarketplace solutions automate the creation of Web-based trading communities, public and private through specific attributes such as registration and authentication, auction, reverse auction, request for proposal (RFP) and request for quotation (RFQ) posting, dynamic matching of buyers and sellers, strategic sourcing, supplier selection, contract negotiation, compliance and management, demand planning and aggregation, and integration into legacy environments. I/T functions involved: • Sourcing & Procurement, Logistics, Finance & Accounting, Integration & Security, eHR • Exclusions: Electronic data interchange (EDI) services, • Inclusions: Examples in products and competitors: • eMarketplaces: Commerce One, Ariba, i2, Oracle, SAP, Broadvision, PurchasePro, WebMethods, Websphere commerce suite Marketplace; eMarketplace Services: IGS, PriceWaterhouseCoopers, Accenture, Cap Gemini Ernst & Young, CSC, Deloitte, KPMG, EDS, Oracle, C1; Collaboration: Agile Software, Exterprise (purchased by C1), PTC, MatrixOne, Tecnomatix Technologies, SDRC, Alventive, E3 Corp. and Agilera.

Core ERP Solution Definition • Customer Business Goal: Management of business processes to lower cost and improve operational efficiency • Business problems/functions addressed: Human resource, accounting, finance, manufacturing, logistics, procurement, customer service, internal manufacturing and logistics management, Business Intelligence, and e-Commerce • High level definition: An integrated set of applications that automates finance and human resources departments as well as handles jobs such as order processing, financial operations, corporate services, manufacturing and logistics management organized by industry verticals. I/T functions involved: • Core ERP • Financial Operations (Financing, Customer Payment, and Settlement (AR), Collaborative Financial Processing, Vendor Invoice Verification and Processing (AP),Bank processes and Relationship Management, Allocation of Shared Services), Accounting(Financial statements, General Ledger and Subledger, Revenue and Cost Accounting, Job and Product Accounting, Product and Service Costing ), Corporate Services (Real estate management, Travel management (TEAs), Treasury and finance management ) Human Resource Management (HR Strategy and Planning, Recruitment, Payroll, Compensation and Total Benefits, Employee Development ), Manufacturing and Logistics (Production planning, materials management, inventory management, order entry and processing, warehouse mgmt, transportation mgmt, project mgmt, plant maintenance, customer service mgmt) • Exclusions: point solutions that will not be considered as a function in the ERP solution • Inclusions: All software applications developed and/or sold by traditional ERP vendors. This includes Cash mgmt, payroll processing (e.g. ADP), piece part of traditional ERP, and industry unique applications (e.g. retail banking, airline reservation), payment mgmt, and manufacturing and logistics management • Examples in products and competitors: SAP, Oracle Apps, PeopleSoft, JD Edward, Baan, SSA, JBA, Intentia, QAD, Lawson, Symix, SCT.