Download

1 / 40

400 likes | 571 Views

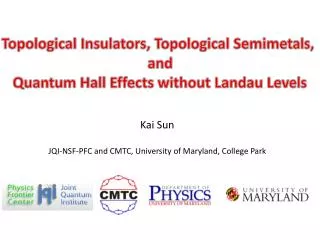

“ MARYLAND RESPONDS” Maryland Cooperative Extension. December 2, 2008 University of Maryland College Park. National. National. National. Sub-Prime Share of All Mortgage Loans: Maryland and the US. ’07Q2 MD: 12.8% US: 14.0%. ‘03Q4 MD:3.2% US: 4.2%. ’08Q2 MD: 11.1%

E N D

“MARYLAND RESPONDS”Maryland Cooperative Extension December 2, 2008 University of Maryland College Park

Sub-Prime Share of All Mortgage Loans: Maryland and the US ’07Q2 MD: 12.8% US: 14.0% ‘03Q4 MD:3.2% US: 4.2% ’08Q2 MD: 11.1% US: 12.2%

Sub-Prime Delinquency and Foreclosure Rates in Maryland Del: 20.9% For: 9.1% Del: 7.6% For: 1.7%

Home Price Inflation in Maryland Jan ’00-Jun ’07 +128.4% Jun ’07-Aug ’08 -6.5%

Economic Costs of Foreclosuresper Foreclosed Property • Includes administrative and legal fees, loss of equity, tax losses. From Anne Moreno’s study in Minneapolis. • Includes opportunity costs of principal and interest not yet received; and servicing, legal, maintenance and property disposition costs. From Craig Focardi’s 2002 study. • From Anthony Pennington-Cross’ 2004 study for the Federal Reserve Bank of St. Luis. • From Immergluck and Smith’s 2006 study of the Chicago area foreclosures.

Property Foreclosure Costs in Maryland, Millions of 2007 Dollars Source: RealtyTrac and DHCD, Office of Research

Extent of Problem in Maryland • Number of foreclosure events continue to increase dramatically: • Foreclosure activity in Maryland has continued to decrease from 9,453 foreclosures in the 2nd quarter of 2008 to 7,974 in the 3rd quarter. • Compared with the 3rd quarter of 2007, foreclosure events in the 3rdquarter of 2008 increased by 13.9. • Prince George’s County continues to be most severely afflicted by the foreclosure crisis, with 2,789 events this quarter (35% of the State’s total). Other jurisdictions follow: • Montgomery County – 14.1% • Baltimore City – 11.0% • Baltimore County– 9.5%

Extent of Problem in Maryland • Foreclosure activity in Maryland decreased by 15.6% from 2nd quarter 2008 to 3rd quarter. • Compared to 2007, foreclosures have increased in all jurisdictions except Caroline and Dorchester counties. • The highest percentage increases were in Queen Anne’s (↑637.5%), Worcester (↑ 535.3%), Garrett (↑ 500%) and Kent (↑366.7%) counties. • Prince George’s County, with 2,789 events, continues to be the most affected. • Some counties have noticed a slight drop in foreclosure rates from the 1st quarter of 2008 to 2nd quarter, due to the new State law (effective 4/4/08) that effectively increased the foreclosure period from an average of two weeks to 135 days.

Losses • It was recently reported that the number of vacant homes nationally is the highest it has been since 1954. (2.2%). • Everyone loses in foreclosure: the homeowner, the lender ($50,000- $80,000), and the neighborhood, where property values can decrease and vacant, boarded-up houses are seen. • There has been a loss of $1.7 trillion dollars in the U.S. economy in the first quarter of 2008.

Mortgage Conditions 2007 Maryland • ALT A • 28.3 loans per 1,000 households • 31.1% low or no documentation • 41.8% resetting in 12 months • 50.5% late payments in last 12 months • Sub-Prime • 19.5 loans per 1,000 households • 69.1% low or no documentation • 4.7% ARMS resetting in 12 months • 20.6% late payments in last 12 months Federal Reserve Bank of New York January 2008

Subprime Loans and Race in Maryland • Data shows that minority homeowners are more likely to have subprime loans: • 54% of African Americans have subprime loans * • 47% of Hispanics have subprime loans * • 18% of Whites have subprime loans* • 70% of loans in Maryland were originated by Brokers • Of 90 Banks in Maryland Reviewed for CRA only 1 has an unsatisfactory rating. *Data Source: Presentation by the Department of Labor, Licensing and Regulation, January 3, 2008

Mortgage Loans in Maryland (Data Source: McDash)

Mortgage Delinquencies in Maryland (Data Source: McDash)

Mortgage Foreclosures in Maryland (Data Source: McDash)

Property Foreclosure Rate • The property foreclosure rate represents the intensity of foreclosures in a community. • Measures the number of home owner households per foreclosure event. • For the first quarter of 2008 there was one foreclosure per 129 households statewide. • Prince George’s County has a rate of one foreclosure per 58 households. • Baltimore City and Charles County are second (78) and third (99).

Cost of Foreclosure • 652,461 properties in 2007 were within a 1/8 mile radius of the 13,460 properties reporting foreclosure events, leading to a decline in property values of neighboring homes. • Total direct loss in housing wealth in Maryland for 2007 was more than $3 billion: • $902.3 million lost directly in housing wealth, • $2.2 billion lost in reduced home values for area surrounding foreclosed properties. • Other foreclosure-related losses in 2007: • $32.3 million lost in unpaid taxes, $22.9 million for neighboring properties. • Additional $96 million lost in administrative costs. • $790 million in losses to banks that have led to repercussions in financial institutions and overall economy.

Maryland’s Response HOPE Hotline • Over 10,000 people have been referred to Servicers, Counseling agencies, Lenders, National HOPE Hotline for intervention Refinance products: $27,000,000 • Lifeline • HomeSaver • Bridge to Hope Counseling • 9,800 people have been served; 40% secured positive outcomes • $2,900,000 from DHCD-- now funding 32 organizations

Maryland’s Response • Governor’s Servicing Initiative • Efficient, transparent response by Servicers • Bankers Consortium/Maryland Housing Fund • Legislative Changes • Some of the most progressive laws in the country • Outreach • 680,000 letters to most heavily affected • PSE announcements, MTA bus advertising, billboards • Hope Website • 53,000 visits in the last year • Pro-Bono Attorney Initiative • Over 600 attorneys throughout the State volunteer to assist

The Lifeline Refinance Program • The Lifeline Refinance mortgage program allows CDA to offer refinancing options to Marylanders who may be facing financial difficulties after purchasing a home with an “exotic” mortgage. (An exotic mortgage is defined as any type of adjustable rate mortgage (ARM), balloon payment loan, negative amortization loan or other unsuitable loan type.)

The Homesaver Refinance Program • The Homesaver Refinance Mortgage Program allows CDA to offer another refinance option to Marylanders who have sub-prime or exotic mortgages and are experiencing difficulties as a result of: • mortgage default, • low credit scores and/or, • a mortgage greater than the current value of their home.

Bridge to HOPE • A loan mitigation strategy approved by the existing lender where housing payment and monthly debt does not exceed 45% of the borrower’s gross income. • B2H can provide a non-interest, non-amortizing loan of up to $15,000. • Can include both a lump sum payment and monthly subsidy with pay outs up to 24 months. • Borrower must continue contact with the counseling agency.

MHF Homesaver Mortgage Insurance • 105% max LTV; (MHF’s 2.75% upfront mortgage insurance premium may be financed) • 110% max CLTV with all 2nd mortgages, including forgivable grants • DTI not to exceed 50% • Minimum credit score 550 • Mortgage(s) may not be more than two months past due at time of loan application

Governor O'Malley's Servicer Initiative • Governor’s initiative calls together mortgage services for loss mitigation collaboration: • Goal: To establish a model framework for streamlined, transparent and timely loss mitigation process. • Maryland has created and will expand its foreclosure prevention assistance network to integrate housing counselors and others into the loss mitigation process with servicers. • Each servicing company will dedicate staff to work with housing counselors and staff from Maryland.

Governor O'Malley's Servicer Initiative • Create a uniform, transparent set of guidelines for loss mitigation. • Agree to accept HOPE Housing Counseling agencies as partners in solving this problem. • Identify a representative from each servicer who is assigned to Maryland to help solve each case. • Agree to a quick and efficient process to make a decision and bring relief. • Create a process to evaluate those cases that do not fit in a set of standard guidelines.

Governor O'Malley's Servicer Initiative • First meeting held on Tuesday February 26, 2008; Second meeting on March 20, 2008. • One on One meetings with participants ongoing. • Servicers are participating in teleconference training sessions with counselors. • GMAC, Countrywide, CitiFinancial, Ocwen, Option 1, Mortgage Bankers Association, PHH Mortgage, E-WIZ Mortgage, Wells Fargo, EMC, Litton Servicing, • Wilton, Litton Chase, FNMA, and FHLMC.

Maryland Department of Labor, Licensing and Regulation: Recent Legislation

Legislative and Regulatory Reforms • SB 217/HB 360 -Real Property - Maryland Mortgage Fraud Protection Act - Creating a comprehensive mortgage fraud statute with criminal penalties and giving prosecutors a robust tool to prohibit mortgage fraud schemes. Expands authorization to include Attorney General, State's Attorney, and the Commissioner of Financial Regulation. Allows victims to bring private action against violators. • SB 216/HB365 -Real Property - Recordation of Instruments Securing Mortgage Loans and Foreclosure of Mortgages and Deeds of Trust on Residential Property – Improving the foreclosure process to provide greater opportunities for homeowners to avoid foreclosure and preserve their home; will lengthen the time before a foreclosure sale, which was as short as 15 days, and after change will increase to 135 to 150 days. Offers other protections to homeowners including personal service at least 45 days prior to action, and the right to Cure up to the day before foreclosure. • SB 218/HB 361 - Protection of Homeowners in Foreclosure - Prohibition on Foreclosure Rescue Transactions - Enforcement - Preventing foreclosure rescue scams by banning conveyance of real property in the foreclosure rescue context.

Legislative and Regulatory Reforms • SB 270/HB 363 - Credit Regulation - Mortgage Lending and Other Extensions of Credit – Correcting questionable underwriting practices and defective mortgage products. The Act creates meaningful licensing and increased regulatory oversight. Reforms include a ban on pre-payment penalties for sub-prime loans, requires verification of ability to repay and ensure clearer standards and accountability for all players in the mortgage industry. • SB 533/1242– Task Force to Sturdy Improvement of Financial Literacy in the State Creates the Financial Literacy Task Force to explore the issue of financial concepts and literacy education in public schools.

Governor O’Malley’s Quote: “We are not here to fix blame. We are here to fix the problem!”

Website www.mdhope.org Product information on: Lifeline Refinance Program Homesaver Refinance Program Bridge to Hope Program HOPE HOTLINE: 1-877-462-7555 DLLR: 1-888-784-0136

What is MDHousingSearch.org? • Statewide service helping landlords and potential tenants to find each other. • Increases access to affordable housing information – FREE to search and list. • Available online 24-7 and supported by a toll-free, bilingual call center, M-F 9 a.m. to 8 p.m.