Download

1 / 24

240 likes | 386 Views

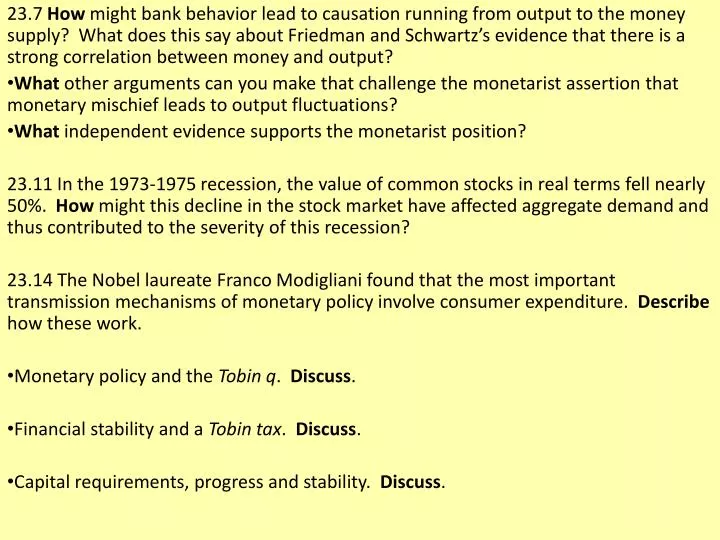

23.7 How might bank behavior lead to causation running from output to the money supply? What does this say about Friedman and Schwartz’s evidence that there is a strong correlation between money and output?

E N D

23.7 How might bank behavior lead to causation running from output to the money supply? What does this say about Friedman and Schwartz’s evidence that there is a strong correlation between money and output? What other arguments can you make that challenge the monetarist assertion that monetary mischief leads to output fluctuations? What independent evidence supports the monetarist position? 23.11 In the 1973-1975 recession, the value of common stocks in real terms fell nearly 50%. How might this decline in the stock market have affected aggregate demand and thus contributed to the severity of this recession? 23.14 The Nobel laureate Franco Modigliani found that the most important transmission mechanisms of monetary policy involve consumer expenditure. Describe how these work. Monetary policy and the Tobin q. Discuss. Financial stability and a Tobin tax. Discuss. Capital requirements, progress and stability. Discuss.

Inflation Rates and Inflation Targets for New Zealand, Canada, and the United Kingdom, 1980–2008 Source: Ben S. Bernanke, Thomas Laubach, Frederic S. Mishkin, and Adam S. Poson, Inflation Targeting: Lessons from the International Experience (Princeton: Princeton University Press, 1999), updates from the same sources, and www.rbnz.govt .nz/statistics/econind/a3/ha3.xls.

Tools, Policy Instruments, Intermediate Targets and Goals of Monetary Policy Criteria for Choosing the Policy Instrument • Ease of observing and measuring • Ability to control • Predictable effect on Goals

Market for Reserves Target Nonborrowed Reserves: FFRATE varies as reserve demand shifts Target Federal Funds Rate: Must vary NBRs to accommodate shifts in reserve demand

Taylor Rule for Federal Funds Rate:1970–2008Target fed funds rate = 2% + π + ½ (π – π*) + ½ ((Y-Yfe)/Yfe) Source: Federal Reserve: www.federalreserve.gov/releases and author’s calculations. Paul Volcker A l a n G r e e n s p a n McChesney Martin Ben Bernanke Wm. Miller Arthur F. Burns

Tools of Monetary Policy • Open market operations • Discount rate borrowed reserves • LENDER OF LAST RESORT • Reserve requirements • Affect the money multiplier…don’t touch/don’t matter • Federal funds rate—theinterest rate on overnight loans of reserves from one bank to another • Primary indicator of the stance of monetary policy Determined by Supply and Demand for reserves • FOMC Balance of Risks Statement Public’s expectations of Fed’s intent Behavior supportive of Fed’s intent

The Money Supply Model • Money = Currency plus checkable deposits: M1 M = C + D • The monetary base (MB)—the assets of the central bank— “backs” the money supply • The CB’s assets = MB =The CB’s liabilities = C + R MB = MBn + BR • The money supply (M) is a multiple m of the monetary base M = m x MB = m x (MBn + BR) m = ( 1 + c ) / ( c + r + e ) = 1 + ( 1 – r – e ) / ( c + r + e )

The Functions of a Modern Central Bank Functions of Federal Reserve District Banks • Clear checks • Issue new currency/withdraw damaged currency • Make discount loans to banks in district • Evaluate mergers/expansions of bank activities • Liaison between business community and the Fed • Examine bank holding companies and state-chartered member banks • Collect data on local business conditions • Research Money, Banking and the Financial System

Asymmetric Information and Bank Regulation(OCC, FDIC, Fed, OTS) Government safety net • Deposit insurance/FDIC: Short circuits bank failures and contagion effect • Payoff method/Purchase and assumption method • Fed as lender of last resort: Too BIG to Fail • Financial consolidation Exacerbates Too Big to Fail • Safety net extended to non-bank financial institutions Safety Net Moral Hazard Problems by Depositors and Banks Safety Net Adverse Selection Problems: Risk-loving bankers Attempted solutions: Constrain banks from taking too much risk • Promote diversification • Prohibit holdings of common stock • Set capital requirements … Capital as cushion Prompt corrective action: Close ‘em down when capital inadequate • Monitor … CAMELS: Capital adequacy/Asset quality/Mgt/Earnings/Liquidity/ Sensitivity to market risk • Disclosure requirements … mark-to-market issue • Restrictions on competition … make banking boring

Bank Management • Liquidity Management • Ample excess reserves • Borrow reserves • Discount loans • Federal funds market • Secondary reserves • Reduce loans • Asset Management • Return/Risk/Liquidity • Tradeoff/Balance • Liability Management • Deposits/CDs/Fed funds… • Capital Adequacy Management • Prevent failure • Regulatory requirement • Basel Accord: Risk-based reqmt • Leverage ratio • Performance Measures • Return on assets: ROA • Return on equity: ROE • Equity multiplier: EM • EM = Assets/Equity Capital • Credit Risk • Screening / Monitoring • Specialized lending • Restrictive covenants • Compensating balances • Credit rationing • COLLATERAL • Interest-rate Risk • Gap and Duration analysis • Off-balance-sheet Activities • Loan sales—Securitization • Fee income: SIVs/Underwriting • Trading income • Value at risk/Stress test/Hedges

Financial CrisesandAggregate Economic Activity • Crises can be caused by: Increases in interest rates/ Increases in uncertainty/Asset market effects on balance sheets/ Banking sector problems/Government fiscal imbalances Vicious spirals Financial crises we have known: 1819, 1837, 1857, 1873, 1884, 1893, 1907, 1930 - 33, 2008

Vicious Spirals Unleashed Demand – Jobs – Wages – Income – Spiral House Price – Foreclosure Spiral Deleveraging – Debt Deflation Spiral Government Revenue – Cutback Spiral Global Repercussion Spiral Macroeconomic Linkages and Feedbacks

Great Depression vs. Great Crisis • 1929 – 1939 • {Lead Up: BOOM Monetary Tightening} • Stock market crash, September 1929 • Fed injects liquidity • Bank panic (9/30) / Bank of US (12/30) • Passive Fed response • Defend gold! (October 1931) • Discount rate up 2% • Great Contraction of money supply • Tax increase, 1932 • Treasury Secretary Mellon: “… liquidate labor, liquidate stocks, liquidate the farmer, liquidate real estate…” • 1933 Bank holiday • Confidence in banks restored • 2008 – 2009 • {Lead Up: BOOM Monetary Tightening} • Housing Bubble Burst ~ Fall 2007 • Subprime meltdown MBS decline • Bear Stearns Bailout • Fannie/Freddie Bailout • Lehman collapse, September 2008 • “Swift and bold” policy responses • AIG nationalization • Innovative “facilities” • maintain credit flow • TARP • Fiscal Stimulus • 2% of GDP in 2009 • 2 ½ % of GDP in 2010 • 2009 Stress Tests • Confidence in banks restored

Administration Wish – List • Fed as czar? • Council of regulators • Evaluate systemic risks/Identify emerging financial innovations • Resolution authority • FDIC model … insurance premiums based on systemic risk? • Consumer financial protection agency Can the Fed do it? Has the Fed done it???? Other ideas in the air • Central clearinghouse for ALL derivatives • “Consumer protection” for sophisticated financial products • Deferred compensation / “clawbacks” • Toughened/countercyclical capital requirements • Tobin tax sand in the well-greased gears of speculation

Financing business: Adverse selection & moral hazard Eight Facts • Stocks are not most important source of external financing • Issuing marketable securities (debt and equity) not the main way businesses finance operations • Indirect finance is much more important than direct finance • Financial intermediaries the most important source of external funds • The financial system is heavily regulated • Only large, well-established corporations have (had) easy access to securities markets to finance their activities need reputation and net worth • Debt contracts: trust … but collateral • Debt contracts: trust … but restrictive covenants

Long-Term Bond Yields, 1919–2008 Sources: Board of Governors of the Federal Reserve System, Banking and Monetary Statistics, 1941–1970; Federal Reserve: www.federalreserve.gov/releases/h15/data.htm.

Movements over Time of Interest Rates on U.S. Government Bonds with Different Maturities Sources: Federal Reserve: www.federalreserve.gov/releases/h15/data.htm.

Expectations Theory of Term Structure Buy a two-year bond yielding i2tor buy a one year bond yielding i1t and turn it over next year at expected yield ie1t+1? But also need to account for preferred habitats (greater interest rate risk and lesser liquidity of long-term bonds add liquidity premium lnt.

Present Values and Interest Rates: i PV Price of a coupon bond summation of “discount bonds”