Download

1 / 13

160 likes | 410 Views

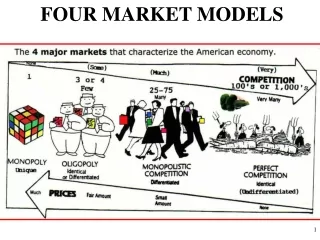

The Four Market Models. How do businesses decide what price to charge and how much to produce? It depends on the character of its industry . Classroom Concerns. Attendance Issues* 15 Limit Tardiness Uniform Assignment Completion. Four Market Models. Pure Competition Pure Monopoly

E N D

The Four Market Models How do businesses decide what price to charge and how much to produce? It depends on the character of its industry.

Classroom Concerns • Attendance Issues* 15 Limit • Tardiness • Uniform • Assignment Completion

Four Market Models • Pure Competition • Pure Monopoly • Monopolistic Competition • Oligopoly They differ in the # of firms in the industry, whether those firms produce a standard product, how difficult it is to enter the industry.

Characteristics of Pure Competition • Large Number of Firms competing(shares on the stock market, farm products) • Standardized Products (consumers are indifferent if price is the same) • Price-Takers (at the mercy of the market price, they make up a fraction of total production) • Free Entry and Exit from Industry (no significant legal, tech, or financial obstacles)

Demand for a Purely Competitive Firm • Perfectly Elastic Demand: The firm is a price-taker, therefore, Marginal Revenue = Demand. • It cannot obtain a higher price by restricting output and it does not need to lower its price to sell more, it just has to produce it. • Figure 9-1 (217) shows the D, MR, and TR for a perfectly elastic firm. (This is not for the whole industry).

Average, Total, and Marginal Revenue • Average Revenue: TR / Quantity Sold • Total Revenue: Total dollars received from the quantity sold • Marginal Revenue: Change in total revenue from selling one additional unit. Test Question (Key Question # 3, Page 243)

Profit Maximization in Short-Run • Since the Purely Competitive firm is a price-taker, it can only adjust output to increase profit. • In the short-run, only variable resources can be adjusted (labour and materials). • To find the profit maximizing point, we must compare TR and TC, or MR and MC.

Profit Maximization (TR-TC) • The firm’s profit is maximized where Total Revenue (TR) exceeds Total Cost (TC) by the maximum amount. • In Figure 9-2 (220) this is displayed in two ways. One is utilizing both TR and TC curves (note the two Break-Even Points). The other is utilizing a total economic profit curve.

Profit Maximization (MR=MC) • The firm can also compare Marginal Revenue and Marginal Cost to maximize profit. • The firm will keep producing more units until Marginal Revenue is equal to Marginal Cost. • For a purely competitive firm, Price = Marginal Revenue, so P = MC for profit maximization. • You cannot produce a fraction of a product.

Calculating Profit • In Table 9-4 (222) Marginal Cost is still less than Marginal Revenue at the 9th unit of output. So that is where we stop producing. • Total Cost = (ATC x 9) • Total Revenue = (MR x 9) • Profit = TR – TC • Therefore: Profit = ($1179 - $880) or $299

Minimizing Losses • If a firm is losing money, it should still produce as long as it is cheaper than them paying the fixed costs with 0 production. • If MR exceeds Marginal Cost at a higher unit of output, it should keep producing, but at a smaller loss… As long as MR > Minimum AVC. • If production adds more to revenue than it does to cost, the firm is saving money.

Perfect Competition Handout • Allocative Efficiency and Perfect Competition • Complete the reading and the associated questions. • Be sure to pay attention to the supplementary graphs. • Hand-in the associated questions tomorrow.