Download

1 / 13

130 likes | 136 Views

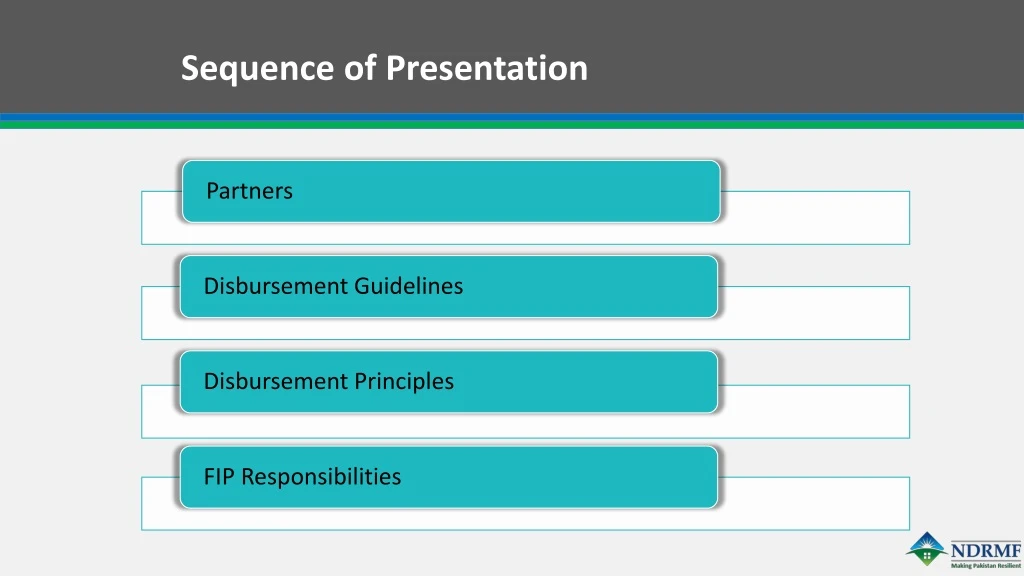

Sequence of Presentation. PARTNERS. The Fund Implementation Partners (FIPs) are those entities that shall be provided grant financing by the Fund and with which a valid Grant Implementation Agreement has been entered into by the Fund .

E N D

PARTNERS • The Fund Implementation Partners (FIPs) are those entities that shall be provided grant financing by the Fund and with which a valid Grant Implementation Agreement has been entered into by the Fund. • The term Fund Implementation Partner includes both, the government and non-government (including UN Agencies) entities. • For the utilization of funds, the non-government entities are restricted to not-for-profit entities and no funding shall be provided to entities that are registered as profit making entities.

DISBURSEMENT GUIDELINES • Disbursements to Fund Implementing Partner (FIP) shall be principally based on “Advance Fund Procedures”. • Financial Projects havingbreakup of cost components and activities related to the shares to be financed by the Fund & FIP (such as 70% and 30%) alongwith“Implementation Plan” shall be prepared and made part of the Grant Financing Agreement. • First withdrawal application shall be submitted upon signing of the agreement based on the agreed Financial Projections. • Subsequently, an FIP shall submit withdrawal applications on quarterly basis, however, if execution of anticipated project’s activities against which the advance funds were released, is achieved before completion of a quarter, FIP shall be eligible to raise a withdrawal application with the Fund earlier.

DISBURSEMENT GUIDELINES (Cont’d) • Financial projections on the prescribed format shall be submitted with the withdrawal application besides submitting a progress review report of the implemented activities. • Statement of Expenditures (SOEs) against the funds that were provided as advance financing, on quarterly basis, shall be presented with the following withdrawal application as per prescribed format(s). • SOEs of FIP’s own share of financing, shall also be submitted with the withdrawal application, invariably. • Withdrawal applications shall be processed by the Fund within seven (07) working days and funds shall be released accordingly. • The advance funds shall be liquidated against SOEs in at least thirty (30) days by the Fund.

DISBURSEMENT GUIDELINES (Cont’d) • Upon disbursement of ninety percent (90%) share of the total Grant Financing by the Fund through withdrawal applications, the remaining ten percent (10%) of the total Grant Financing by the Fund, shall be withheld until submission and approval of the Project Completion Report. • A withdrawal application for making direct payment to the vendor/contractor/consultant, can also be submitted to the Fund in case of establishment of LC for the importation of the goods and/or payment of advance against an irrevocable and unconditional bank guarantee of equivalent amount from a scheduled bank with long term rating of AA from PACRA / JCR-VIS on the date of issuance of guarantee. • For LC or advance payments, original related documents shall remain with the FIP, however, copies of supporting documents shall be furnished with the Withdrawal Application to the Fund with all the necessary account details of the vendor/contractor/consultant.

DISBURSEMENT GUIDELINES (Cont’d) • In case, a specific contract with the vendor/contractor/consultant entails certain retentions from any respective/prospective payments, all such retentions shall be made by the FIP and while claiming a withdrawal application, details of all such retentions either made or to be made, shall invariably be provided with the Withdrawal Application.

DISBURSEMENT PRINCIPLES • A dedicated separate Bank Account for the Grant Financing by the Fund, shall be opened and managed by an FIP throughout the implementation. • For Private Sector Entities, the Bank Account shall be a “Current Account” opened with a scheduled bank having long term rating of AA as assigned by PACRA & JCR-VIS on the date of opening of an account by FIP. • For Public Sector Entities, either an Assignment or Special Drawing Account shall be opened. • All the funds to public sector entities shall be routed through consolidated (non-food) account of respective provincial government and Finance Department shall authorize the releases. • All the funds to be provided by the Fund as Grant Financing, shall be deposited in the dedicated separate account and shall be operated therefrom as per the authorizations.

DISBURSEMENT PRINCIPLES (Cont’d) • No funds from another source shall be deposited in the dedicated account to be maintained for grant financing of the Fund. • Annual audited accounts along with the Management Letter from its external auditors and responses thereof shall be submitted to the Fund within six (6) months from the date of closure of a financial year. • Misallocation and/or misuse of funds provided by the Fund, shall render an FIP ineligible for further disbursements, replenishment and/or future assistance. • Overhead cost of the project should not exceed 15% of the total project cost and shall be completely borne by the FIP from its 30% share. • If an FIP over spends beyond the budgeted amount under any head, FIP itself, shall make up for the over spent amount and the Fund shall not, in any case, be held liable for the payment.

DISBURSEMENT PRINCIPLES (Cont’d) • An FIP shall have no authority, at its own initiative, to reallocate funds between budget lines. • Any reallocation of the budgeted amount must be requested with plausible justifications and accepted in writing by the Fund. • Fund shall not incur any cost associated with the “Disbursement of Grant Financing” to FIPs as all the transaction charges shall be borne by FIP, itself. • No retroactive disbursement authorization shall be allowed in any case and accordingly, the Grant Implementation Agreement shall have no such provision to authorize any such authorization.

FIP’s RESPONSIBILITIES • Shall confirm that it shall make available its agreed share/contribution from the Total Project Cost during the currency of Grant Implementation Agreement. • Shall be responsible for the payment of all taxes and duties from their respective share of contribution for the project. • Furnish certified details of deduction & payment of withholding & all applicable taxes from the respective invoice(s) of the vendor/contractor/consultant as per the prevalent taxation laws of the country, shall be submitted with the Withdrawal Application. • Shall release the payments to contractors and suppliers within 07 days from the date of acceptance of invoice. • Supporting documentation of any disbursement claims i.e. bills/invoices against the expenditures made by the FIP, shall be retained with FIP which shall be inspected & audited by the Fund or any of its designated representatives, regularly during the project implementation phase.

FIP’s RESPONSIBILITIES • Allow and facilitate the visit of Fund’s deputed internal auditor or any person/committee duly authorized by the Fund, to the premises of FIP or the project site, to conduct audit at such intervals as Fund may determine. FIP shall make available all the records, files, papers and documents to such internal auditor/representative(s) of the Fund. • Shall be fully responsible for proper use and administration of all the funding provided by the Fund by exercising due diligence. An affidavit in this regard shall be obtained from the FIP at the time of signing of Grant Implementation Agreement. • A Private Sector entity shall have an obligation to carry out third party audit of all the expenditures and their records, accounts, procedures etc. by a CA Firm which should be in State Bank of Pakistan’s Panel of Auditors under Category ‘A’ and having ‘Satisfactory’ rating under the Quality Control Review Programme managed by the Institute of Chartered Accountants of Pakistan. • In respect of public sector entities, their audit shall be carried out by the Office of Auditor General.

FIP’s RESPONSIBILITIES (Cont’d) • Ensure that the Withdrawal Application and activity completion report(s) of corresponding payment claims, are submitted as per approved formats and prepared in accordance with the contractual provisions including approved specifications of goods/Bill of Quantity (BOQ) for works or TORs of Consultancy Services • In case of Civil Works’ contracts, ensure that all the measurements have been recorded in the Measurement Book correctly that includes (i) Original and Revised Cost (ii) amount of approved variation order (VO), in case of VO’s, and (iii) Date of Measurement. • All payments by an FIP to their vendors/contractors/consultants or any individual shall be made from the designated bank account through crossed cheques. • Ensure that no payment is made to those vendors/contractors/consultants or any individual which are not registered with relevant taxation authority (i.e. Income & Sales Tax).

FIP’s RESPONSIBILITIES (Cont’d) • Establish an effective Anti-Money Laundering (AML)/ Counter Financing of Terrorism (CFT) system to deter criminals from using, project’s fund, especially Grant Financing of the Fund for Money Laundering or Terrorist Financing purposes. • Onus of following actions shall invariably and exclusively rest with the respective implementing partner and FIP shall indemnify the Fund in all the such aspects: • Execution of activities, • Complying with the standard accounting protocols, • Verification of the documents & deliverables, ex ante and post ante performance and account’s audit of entire project’s cost i.e. both FIP and Fund’s Shares, by any third party entity including the Fund or its authorized representatives.