Download

1 / 34

520 likes | 941 Views

Decentralization, Responsibility Centers, and Transfer Pricing. Centralization and Decentralization Spectrum. High degree of delegation of duties, power, and authority to lower levels of the organization. High degree of retention of duties, power, and authority by top management. Centralized.

E N D

Decentralization, Responsibility Centers, and Transfer Pricing

Centralization and Decentralization Spectrum High degree of delegation of duties, power, and authority to lower levels of the organization High degree of retention of duties, power, and authority by top management Centralized Decentralized Neither centralization nor decentralization is necessarily a desirable organizational goal!

Decentralization in Organizations Benefits of Decentralization Top management freed to concentrate on strategy. Lower-level managers gain experience in decision-making. Decision-making authority leads to job satisfaction. Lower-level decision often based on better information. Improves ability to evaluate managers.

Decentralization in Organizations May be a lack of coordination among autonomous managers. Lower-level managers may make decisions without seeing the “big picture.” Disadvantages of Decentralization Lower-level manager’s objectives may not be those of the organization. May be difficult to spread innovative ideas in the organization.

Decentralization and Segments An Individual Store A segment is any part or activity of an organization about which a manager seeks cost, revenue, or profit data. A segment can be . . . Quick Mart A Sales Territory A Service Center

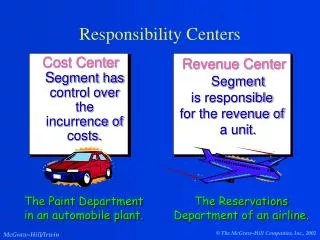

Cost, Profit, and Investments Centers Cost Center A segment whose manager has control over costs, but not over revenues or investment funds. Cost Cost Cost

Cost, Profit, and Investments Centers Profit Center A segment whose manager has control over bothcosts and revenues, but no control over investment funds. Revenues Sales Interest Other Costs Mfg. costs Commissions Salaries Other

Cost, Profit, and Investments Centers Investment Center A segment whose manager has control over costs, revenues, and investments in operating assets. Corporate Headquarters

Cost, Profit, and Investments Centers Cost Center Profit Center Investment Center Cost, profit, and investment centers are all known as responsibility centers. Responsibility Center

Net operating income Average operating assets ROI = Return on Investment (ROI) Formula Income before interest and taxes (EBIT) Cash, accounts receivable, inventory, plant and equipment, and other productive assets.

$30,000 $200,000 =15% ROI = Return on Investment (ROI) Formula Regal Company reports the following: Net operating income $ 30,000 Average operating assets $ 200,000 Sales $ 500,000

Controlling the Rate of Return Three ways to improve ROI . . . • Reduce • Expenses • Increase • Sales • Reduce • Assets

Controlling the Rate of Return • Regal’s manager was able to increase sales to $600,000 which increased net operating income to $42,000. • There was no change in the average operating assets of the segment. Let’s calculate the new ROI.

Return on Investment (ROI) Formula We can modify our original formula slightly: Margin Turnover × Net operating income Sales Salesaaaaaaaaa Average operating assets ROI = × $42,000 $600,000 $600,000 $200,000 ROI = × ROI = 21% We increased ROI from 15% to 21%

Criticisms of ROI In the absence of the balanced scorecard, management may not know how to increase ROI. Managers often inherit many committed costs over which they have no control. Managers evaluated on ROI may reject profitable investment opportunities.

The Balanced Scorecard Management translates its strategy into performance measures that employees understand and accept. Customers Financial Performancemeasures Learningand growth Internalbusinessprocesses

Criticisms of ROI • As division manager at Winston, Inc., your compensation package includes a salary plus bonus based on your division’s ROI -- the higher your ROI, the bigger your bonus. • The company requires an ROI of 15% on all new investments -- your division has been producing an ROI of 30%. • You have an opportunity to invest in a new project that will produce an ROI of 25%. As division manager would you invest in this project?

Criticisms of ROI As division manager, I wouldn’t invest in that project because it would lower my pay!

Criticisms of ROI Gee . . . I thought we were supposed to do what was best for the company!

Residual Income - Another Measure of Performance Net operating income above some minimum return on operating assets

Residual Income • A division of Zepher, Inc. has average operating assets of $100,000 and is required to earn a return of 20% on these assets. • In the current period the division earns $30,000. Let’s calculate residual income.

Motivation and Residual Income Residual income encourages managers to make profitable investments that would be rejected by managers using ROI.

The following information is available on Company A: Sales $900,000 Net operating income 36,000 Stockholders' equity 100,000 Average operating assets 180,000 Minimum required rate of return 15% Company A's return on investment (ROI) is: A) 36%. B) 20%. C) 15%. D) 4%.

The following data are available for the South Division of Redride Products, Inc. and the single product it makes: Unit selling price $20 Variable cost per unit $12 Annual fixed costs $280,000 Average operating assets $1,500,000 How many units must South sell each year to have an ROI of 16%? A) 240,000. B) 1,300,000. C) 65,000. D) 52,000.

All other things equal, a company's return on investment (ROI) would generally increase when: A) sales decrease. B) average operating assets increase. C) operating expenses increase. D) operating expenses decrease.

TRANSFER PRICING A transfer price is the price charged when one segment (for example, a division) provides goods or services to another segment of the same company.

TRANSFER PRICING – Some Points • Transfer prices are necessary to calculate costs in a cost, profit, or investment center. • The purchasing division will naturally want a low transfer price and selling division will want a high transfer price. • From the standpoint of the firm as a whole, transfer prices involve “taking money out of one pocket and putting it into the other.” • An optimal transfer price is one that leads division managers to make decisions that are in the best interests of the firm as a whole.

EXAMPLE: The Battery Division of Barker Company makes a standard 12-volt battery. Production capacity (number of batteries) 300,000 Selling price per battery to outsiders $ 40 Variable costs per battery $ 18 Fixed costs per battery (based on capacity) $ 7 Barker Company has a Vehicle Division that could use this battery in its forklift trucks. The Vehicle Division would like to buy 50,000 batteries per year. It is presently buying these batteries from an outside supplier for $39 per battery.

Suppose the Battery Division is operating at capacity. What is the lowest acceptable transfer price from the viewpoint of the selling division? But, the purchasing division will not pay more than $39, the cost from buying the batteries from the outside. So the two managers will not be able to agree to a transfer price and no transfer will voluntarily take place. From the standpoint of the entire company, no transfer should take place since the company gives up $40 in revenues, but saves only $39 in costs.

Assume again that the Battery Division is operating at capacity, but suppose that the division can avoid $4 in variable costs, such as selling commissions, on intracompany sales. What is the lowest acceptable transfer price from the viewpoint of the selling division? Once again, the purchasing division will not pay more than $39, the cost from buying the batteries from the outside. In this case an agreement is possible. Any transfer price within the range $36 Transfer price $39 From the standpoint of the entire company, this transfer should take place since the cost of the transfer is $36 and the company saves $39, for a net gain of $3.

COST-BASED TRANSFER PRICES • Transfer prices based on cost are easily understood and convenient to use and do not require negotiation. • Unfortunately, cost-based transfer prices have several disadvantages: • Cost-based transfer prices can lead to bad decisions. (For example, they don’t include opportunity costs from lost sales.) • The only division that will show any profit on the transaction is the one that makes the final sale to an outside party. • Cost-based transfer prices provide no incentive for control of costs unless transfers are made at standard cost.

MARKET-BASED TRANSFER PRICES • When there is an active market for the item being transferred, the market price may be a suitable transfer price. • However, when there is idle capacity, the market price will overstate the real cost to the company of the transfer and may lead the purchasing division manager to make bad decisions.