Download

1 / 31

310 likes | 487 Views

Risk Based Supervision under Basel II Jeffrey Carmichael. Cartagena February 16-18, 2004. Outline. What is the risk based approach? How does it apply to banks? How does it apply to regulation? How does it apply to supervision? Challenges arising from Basel II.

E N D

Risk Based Supervision under Basel IIJeffrey Carmichael Cartagena February 16-18, 2004

Outline • What is the risk based approach? • How does it apply to banks? • How does it apply to regulation? • How does it apply to supervision? • Challenges arising from Basel II Presentation: Jeff Carmichael

What is the Risk-Based Approach? • No universally-accepted definition • Meaning depends on the situation • Most widely accepted proposition would be that a risk-based approach requires that you: • Identify risks and apply resources where the risks are greatest Presentation: Jeff Carmichael

1. How Does this Apply to Banking? • Major sources of banking risk: • Credit Risk • Market Risk • Liquidity Risk • Operational Risk • Question: Which is the greatest risk? Presentation: Jeff Carmichael

Experience Late 80s & Early 90s • Widely agreed that credit risk is dominant - experience in the 80s/90s was good reminder • Developed markets - worst loan losses for 50 years • Common characteristics: • excessive exposures to individual borrowers • excessive exposures to sectors • excessive reliance on collateral • poor credit evaluation • All arose primarily from credit risk Presentation: Jeff Carmichael

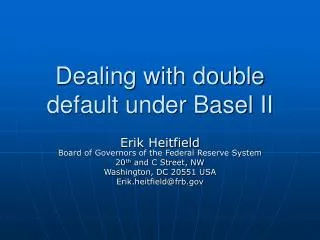

RMA & FMCG Survey Better Credit Mgt. = Higher & More Stable Returns Presentation: Jeff Carmichael

Also Found ... Payback to better risk management goes beyond protecting share price • helped better serve customer needs • enabled better business decisions Returns to investing in risk management are very high • compared losses under best practice with cost of improvements - suggested return of 1,000% over 10 years Presentation: Jeff Carmichael

Main Advances Since Then • Improved data management • Improved credit grading from one-dimensional to two dimensional (PD and LGD) • Shift to portfolio risk assessment • Credit risk modelling • Risk-based pricing, provisioning and reward structures • Integrated risk management • Risk-based capital allocation Presentation: Jeff Carmichael

Motivation for Advances • Bankers remember the pain • Shareholders react to differential losses • Competition is increasing • The tools are available • There is more to lose (rewards are tied to performance) Presentation: Jeff Carmichael

2. “Risk-Based” Regulation • The central Pillar of banking regulation is capital adequacy • Starting with the first Capital Accord in 1988 banking regulators began imposing risk-weighted capital adequacy requirement • The philosophy is straightforward - greater risk requires greater capital Presentation: Jeff Carmichael

Interaction Between Regulation and Banking Practice • As noted - banks now allocate capital internally to activities and areas according to the risks taken • Not widespread before the first Basel Accord in 1988 • Accord encouraged banks to think in terms of risk-based capital allocation • Since then, banks have generally gone well beyond the 1988 Accord - hence one of the primary motivations for Basel II … • Case for change is in the divergence between regulatory capital and banks’ assessments of economic capital required for risk - illustration …. Presentation: Jeff Carmichael

Economic Vs Regulatory Capital Economic Basel I 8% Presentation: Jeff Carmichael

The Challenge for Basel II • Need for greater risk sensitivity than Basel 1 and its “one size fits all” Approach • Need for a framework that is credible, sound and reflective of industry practices • Need to be more incentive compatible with desire of regulators to promote and enhance good credit risk management • Problem - there is no standardized approach agreed by industry for the measurement and management of credit risk (unlike market risk) Presentation: Jeff Carmichael

The Outcome • A “menu” approach: • Standardized (modified from Basel I); • IRB Foundation • IRB Advanced • Standardized is still “blunt” like Basel I • IRB approaches are an attempt to “approximate” what the industry is doing • It stops short of allowing banks to use their own models entirely for assessing capital adequacy • It allows banks to use some of the critical inputs to their models (PD, LGD, EAD) but constrains the way they are combined to assess capital adequacy Presentation: Jeff Carmichael

3. “Risk-Based” Supervision • Again the idea of a risk-based approach = apply resources where the risks are greatest • Thus a supervisor following a risk-based approach will attempt to: • Identify those banks in which risks are greatest • Identify within each bank those areas in which risks are greatest • Apply scarce supervisory resources so as to minimizing the overall “regulatory” risk Presentation: Jeff Carmichael

Risk Rating Banks • Most regulators use some form of rating system (e.g. CAMELS) for banks • Following the experience of banks many have moved to a two-dimensional grading scale; e.g. • PF - probability of failure • CGF - (systemic) consequences given failure Presentation: Jeff Carmichael

Example - PAIRS • APRA Reviewed developments in US, UK and Canada • Developed PAIRS system (Probability and Impact Rating System) • As in banking - risk grading system should not eliminate subjectivity but the discipline imposed by a structured approach should increase objectivity • Back up with peer review and quality control Presentation: Jeff Carmichael

Conceptual Framework for PF Inherent Risk _ Management & Control Risk of FailurePF _ Capital Support Presentation: Jeff Carmichael

The Structured Approach • The Impact rating is based largely on size - with some management over-ride if needed • PF x Impact (CGF) = index of supervisory attention • The Index of Supervisory Attention is exponential from 1 to 56,000 • The Index is grouped into: • Normal • Oversight • Mandated Improvement • Restructure Presentation: Jeff Carmichael

Supervisory Attention Grid Presentation: Jeff Carmichael

Beyond Risk Grading • Risk-based supervision requires better risk grading to identify the institutions posing the greatest risks • It also requires targeted inspections and investigations • It requires judgement and graduated supervisory responses • This is where Basel II has focused its attention through Pillar 2 Presentation: Jeff Carmichael

Pillar 2 - Supervisory Review • Philosophy: • Pillar 1 Capital Framework is only an approximation - it is not entirely comprehensive • Capital is critical in mitigating risk but it is not the only relevant factor - a bank should have sound processes and procedures for measuring, monitoring and managing risk Presentation: Jeff Carmichael

Supervisory Review Process • Use tools available to assess how accurately Pillar 1 matches minimum capital with risks taken by the bank • Use tools available to understand how strong a bank’s processes & procedures are and how well they are implemented • Use supervisory judgement to impose additional supervisory requirements (including capital) where residual risk is excessive Presentation: Jeff Carmichael

Assessing the Adequacy of a Bank’s Capital • Principle 1: Banks should have a process for assessing capital relative to risks and a strategy for maintaining it • Supervisors: • Review the risk assessment processes for relevance and comprehensiveness - does the bank recognise other risks such as interest rate risk? • Identify inconsistencies • Check that management is engaged • Assess application and controls - are processes followed? • Require stress tests Presentation: Jeff Carmichael

Specific Guidance • Interest Rate Risk in the banking book • Operational Risk • Definition of default • Risk mitigation • Concentration Risk • Securitization Presentation: Jeff Carmichael

Demands Related to IRB • Banks that choose IRB need to meet a series of demanding qualifying and validation criteria • These have been set out in detail by the Basel Committee - along with guidance about what and how to check • The on-going monitoring of the appropriateness and application of these model-based risk management processes is a fundamental part of Pillar 2 supervisory review - especially stress testing Presentation: Jeff Carmichael

Responding to Assessed Risks • Principle 2: Supervisors should take enforcement action if not satisfied with a bank’s approach to risk management • Principle 3: Supervisors should expect banks to hold above the minimum and should be able to require them to do so • Principle 4: Supervisors should intervene early to prevent capital falling through the minimum Presentation: Jeff Carmichael

Is Pillar 2 Really Anything New? • To the extent that Pillar 2 emphasises: • Assessment of risks • Supervisory judgement & discretion • Active enforcement • It is just an extension of the already growing risk-based approach to supervision • It does provide detailed guidance - but many countries already exercised this type of approach • Problem was - not all countries could! • Pillar 2 formalises the central role of flexibility • Without that flexibility Basel II is a waste of time Presentation: Jeff Carmichael

Summary • The “risk-based” approach is about identifying risks and devoting resources to where they will be most effective in reducing risks • This approach is as critical in banking as it is in regulation and supervision • In regulation it requires that capital requirements are greater where risks are greater • In supervision it requires supervisors to: • Assess where the risks are greatest • Intervene and enforce standards flexibly where the risks are greatest • Pillar 2 of Basel II provides a framework for the assessment and intervention process • Pillar 2 is a fundamental component of Basel II Presentation: Jeff Carmichael

Thank You Presentation: Jeff Carmichael

Risk-Based Supervision: Challenges under Basel II ARMICHAEL ONSULTING Pty Ltd