Download

1 / 50

540 likes | 981 Views

Lesson 2 Business Transactions and Accounting Equation. Task Team of FUNDAMENTAL ACCOUNTING School of Business, Sun Yat-sen University. Outline. Enterprises Accounting Transactions, Accounting Events, and Accounting Circumstances Economic Activities and Accounting Elements

E N D

Lesson 2 Business Transactions and Accounting Equation Task Team of FUNDAMENTAL ACCOUNTING School of Business, Sun Yat-sen University

Outline • Enterprises • Accounting Transactions, Accounting Events, and Accounting Circumstances • Economic Activities and Accounting Elements • Accounting Equation

Opening Story • Funding and Spending at College • Assets of a college student • Cash • CD player • Computer • Funding these assets • Sponsored by parents • Sponsored by relatives • Borrowed from relatives and acquaintance

Opening Story (continued) • We could deal with the above-mentioned financial issues from the following perspectives: • How do we fund our daily expenditures and possessions? • How do we spend the “funds” which we have sourced? • What about the relationship between the “funds” which we have sourced and our daily expenditures and possessions?

Enterprises • Concept of Enterprise • Definition of “enterprise” • Functions of an enterprise • Characteristics of an enterprise

Forms of Enterprise • There are three major forms of enterprise: • Sole-proprietorship • Partnership • Corporations

Sole proprietorships • Single person owns the business • Not separate from its owner in terms of responsibility and liability • The business is the owner and the owner is the business

Partnership • Owned by two or more people • Similar to a sole proprietorship • Not separate from the owners in terms of responsibility and liability

Corporations • Legally separate and financially separate from the owners • Ownership in a corporation is divided into units called shares of capital stock • Owners are called shareholders or stockholders • Corporations are separate legal entities

Four Types of Enterprise • Service organization – provides services (does something for you) rather than selling something • Merchandising business – buys goods, adds value to them, then sells them to customers • Manufacturer – makes the products it sells • Financial services company – doesn’t make tangible products and doesn’t sell products made by other companies; deals in services related to money

Resources in an Enterprise • Major resources: • Human resources • Properties,plant and equipment,supplies, raw materials, finished products or inventories • Financing • In cash or bank deposits • In material forms

Movements of Material Resources in an Enterprise • An example-Beauty Photo Store

Movements of Material Resources in an Enterprise • Movements in a manufacturing enterprise • cash/bank deposit→raw materials →work-in-process→finished products→fin→cash/bank deposit • Movements in a merchandising enterprise • cash/bank deposit→inventory→ cash/bank deposit

Activities of Enterprise • Three major phases of business activities: • Inception • Operating • Liquidation

Investment of owners Total funds of a firm Financing of creditors Inception of Enterprise • Inception and investment of funds • External funding • State, legal persons, privates or foreign investors; • Financing from banking institutions, other legal persons or privates • Owners’equity and liabilities

Inception of Enterprise • Forms of Investment • Monetary(cash/bank deposits) • Property, plants and equipment • Raw materials and goods,etc. • Sources and changes of funds • Increase of owners’equity or liabilities • Increase of assets

2 cameras lens +producing equipment + supplies cash photos cash Operating Activities • Operating activities and changes of asset • Changes of assets in Beauty Photo Store • Connections between Beauty Photo Store and Suppliers, clients, etc.

Liquidation of Enterprise • Liquidation of enterprise and payoff of funds • Payment of taxes • Distribution of profits • Declaration of dividends • Payoff of borrowings • Withdrawals and changes of funds • Decrease of assets • Decrease of liabilities or owners’equity

Accounting Transactions • A business transaction is an event that affects the financial position of a business and may be reliably recorded

Economic Activities and Accounting Elements • Accounting element: • Uses of funds and assets • cash • equipment,etc. • Resources of funds and equity • Borrowings and equity of creditors-liabilities • Investments and owners’equity

Uses of Funds • Uses and changes of funds • Beauty Photo Store • From cash to equipment • Using equipment to produce photos • From photos to cash

Circulation of Funds • Circulation of funds: • Uses of funds • Beauty Photo Store • Cost of equipment • Cost of supplies • Human costs? • Uses and payoff of funds • What are the operating purposes for Beauty Photo Store?

Payoff of Funds • Payoff of Funds and Revenues • Cash receptions and revenues by Beauty Photo Store • Net increase of funds and profit • Difference between uses and payoff of cash? • Nature of profit?

Accounting Transactions • Accounting transactions-Economic exchange between two different accounting entities • Mutual exchange • A purchases an asset,paying cash or bearing the responsibility of paying cash in future • B sells the asset, earning the rights of receiving or collecting cash • One-way transaction • Investments or donations to another accounting entity

Accounting Events • Accounting events-internal transferring of resources among departments of a same entity • allotments of raw materials for plants • Damages caused by earthquakes • External versus internal events • Between different entities • Within a same entity

Accounting Circumstances • Accounting circumstances-usually an outcome of collaboration of multiple events • Circumstances and their impacts • Changes in prices,exchange rates • How to determine these changes? • E.g. uncollectability of receivables due to the liquidation of the debtor • Unpredictability

Accounting Elements • Assets • Liabilities • Owners’equity • Revenues • Expenses • Profits

Assets • Assets are economic resources owned by a business that are expected to be of benefit in the future.

Further Thoughts on Assets • Human resources as an asset? • Value and labor of Manager of Beauty Photo Store? • Cameramen and shop assistants? • Natural resources as an asset?

Liabilities • Liabilities are creditor’s claims to the assets. Liabilities are obligations to outsiders

Owners’Equity • Owner’s Equity is the owner’s claim to the assets. It is the amount of assets that remains after subtracting the liabilities.

Changes in Owners’Equity • Investments by owners and revenues, amounts earned by delivering goods or services to customers, increase owner’s equity. • Withdrawals of assets from the business by owners and expenses decrease owner’s equity. Expenses occur when assets are used or liabilities increase as a result of earning revenues.

Revenue • Revenues (sales) are increases in owners' equity arising from increases in assets received in exchange for the delivery of goods or services to customers. • Revenues are increases in economic resources, either through increases to assets or reductions to liabilities

Revenue Recognition • Revenue should be recognized in the financial statement when: • the performance has been achieved • there is reasonable assurance regarding the measurement and collectability of the consideration

Expense • Expenses are decreases in owners' equity that arise because goods or services are delivered to customers. • Expenses are decreases in economic resources, either through outflows or the using-up of assets or incurrence of liabilities from delivering or producing goods, rendering services, or carrying out other activities that constitute the entity’s normal business

Expense Recognition • Cost, expenditure, and expense • General recognition criteria • Approaches to expense recognition

Cost, Expenditure, and Expense • When we agree to pay out cash (or other assets) for goods or services received, we have incurred a cost • When we actually pay the cash, we have an expenditure • When the benefits of the cost have been used and we put that cost (or a portion thereof) on the income statement, we have recognized an expense

General Recognition Criteria • Recognized items must: • meet the definition of a financial statement element • have a valid measurement basis and amount • Financial statement elements are based on future economic benefits or sacrifices; these must be probable for recognition to be appropriate

General Recognition Criteria (cont) • Expenses are decreases in economic resources, either by way of outflows or reductions of assets or incurrences of liabilities, resulting from an entity’s ordinary revenue generating or service delivery activities [CICA 1000.38] • Asset or expense? if the asset recognition criteria are met, an asset is recorded. If not, an expense is recorded

Approaches toExpense Recognition • Definitional approach: expenses are created either through the reduction of an asset or the increase in a liability • Matching approach: once revenues are determined in conformity with the revenue principle for any reporting period, the expenses incurred in generating the revenue should be recognized in that period

Profit / Loss • Income (profit or earnings) is the excess of revenues over expenses

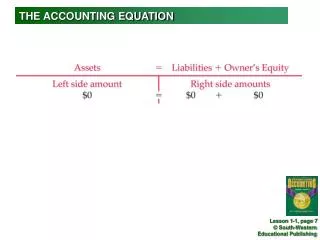

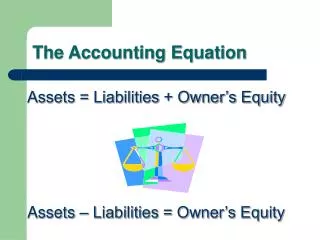

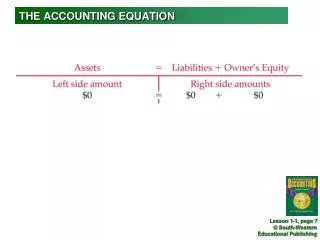

Accounting Equation • Assets – Liabilities = Owners Equity • Net Assets = Owners’ Equity • Every accounting transaction has an equal affect on both sides of the equation. • Purchase a $20,000 car for cash. • Increase asset car and decrease asset cash by $20,000. No net change to assets. • Purchase a $20,000 car on credit. • Increase asset car and increase liabilities by $20,000.

Dual Aspect ofAccounting Equation • Assets = Liabilities + Owners’ equity. • LHS = RHS. • First view: • Resources = Obligations to creditors or claims on resources + Residual claim. • Second view: • Amounts invested in resources = how these amounts were financed. • Resources = financed by creditors + financed by owners.

Asset:130000 Liability:30000 Equity:100000 + = Revenue:15000 + Expense:9000 = Profit:6000 Assets 130000+15000-9000 Owners’ equity 100000+6000 Liabilities30000 + = Beauty Photo Store-- An Illustration • Changes to the accounting equation of Beauty Photo Store:

Summary • Economic resources in the enterprise-human,financial and material resources • Economic transactions derive from the operating activities of an enterprise • Accounting elements are basic components of economic transactions • Accounting elements comprise of assets,liabilities, owners’equity, revenues, expenses and profit • Economic transactions are viewed in the forms of increase or decrease in accounting elements • Accounting equation:A=L+OE

Case for Discussion Marks and Spencer • In 1882, a Russian refugee named Michael Marks came to the North East of England. Needing work, he put a tray round his neck and started selling haberdashery in the villages around Leeds. Two years later he borrowed £5 from his friend Isaac Dewhirst to buy stock, and was able to open a stall in Leeds market. • Within ten years Marks’s success as a trader had enabled him to establish a chain of stalls in markets throughout North East England. In 1894, Marks realized that his business was getting too large for him to manage effectively on his own. He decidedto form a partnership withTom Spencer – and Marks& Spencer was born.

Case for Discussion (cont) • The business continued to thrive and grow, so in 1903 Marks and Spencer registered their partnership as a private limited company. This allowed more people to become involved with managing the growing company and increase its finances by buying shares in the company. One shareholder was Israel Sieff, who became chairman of the company in 1917. Sieff can be credited with shaping the future of Marks & Spencer. By 1926, Marks & Spencer had opened 125 stores. In order to continue its successful development the company finally registered as a public limited company (plc) in order to obtain as much capital as possible to finance its continued growth. • And the rest, as they say, is history.

Suggested Questions • How many people started the original business that eventually became Marks & Spencer? • Who owned the original business? • Who owns Marks & Spencer plc? • Why do you think Marks & Spencer became a public limited company? • Do you think the business would have developed in the way it has if it was still owned by one person?