Download

1 / 30

300 likes | 451 Views

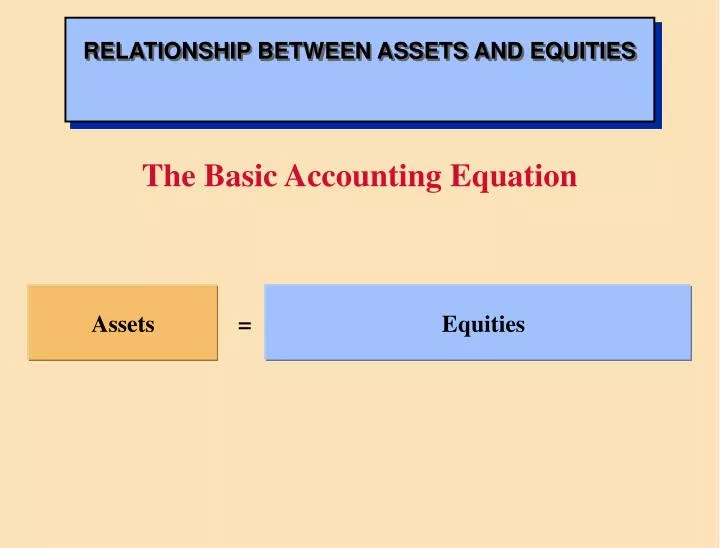

RELATIONSHIP BETWEEN ASSETS AND EQUITIES. The Basic Accounting Equation. Assets = Equities. THE BASIC ACCOUNTING EQUATION. The Basic Accounting Equation. Assets = Liabilities + Stockholders’ Equity.

E N D

RELATIONSHIP BETWEEN ASSETS AND EQUITIES The Basic Accounting Equation Assets = Equities

THE BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Stockholders’ Equity

RELATIONSHIPS AMONG SUBDIVISIONS OF STOCKHOLDERS’ EQUITY INCREASEDECREASE Dividends to Stockholders Investments by Stockholders Stockholders’ Equity Revenues Expenses

My division needs 2,500 pounds from your division We need ten cases by Friday USING THE BUILDING BLOCKS TRANSACTION ANALYSIS • Transactionsare the economic events of the enterprise. • They may be identified as external or internal. 1 External transactionsinvolve economic events between the company and some and some outside enterprise or party. 2 Internal transactionsare economic events that occur entirely within one company.

TRANSACTION ANALYSIS TRANSACTION 1 • Ray and Barbara Nealdecide to open a computer programming company to be incorporated as Softbyte, Inc. • They invest $15,000 cash in exchange for $15,000 of common stock.

Assets = Liabilities + Stockholders’ Equity Common Cash Stock TRANSACTION ANALYSIS TRANSACTION 1 SOLUTION (1)+15,000 = +15,000 Investment There is an increase in the asset Cash, $15,000, and an equal increase in the stockholders’ equity, Common Stock, $15,000.

TRANSACTION ANALYSIS TRANSACTION2 Softbytepurchases computer equipment for $7,000 cash.

TRANSACTION ANALYSIS TRANSACTION 2 SOLUTION (2)-7,000 +$7,000 Stockholders’ Assets = Liabilities + Equity Common Cash + Equipment = Stock Old Bal. $15,000 $15,000 New Bal. $ 8,000 + $7,000 = $15,000 $15,000 Cash is decreased $7,000 and the asset Equipment is increased $7,000.

Acme Supply Company Softbyte, Inc. TRANSACTION ANALYSIS TRANSACTION3 • Softbytepurchases computer paper and other supplies expected to last several months from Acme Supply Company for $1,600. • Acme Supply Company agrees to allow Softbyteto pay this bill in October, a month later. • This transaction is often referred to as a purchase on account or a credit purchase.

TRANSACTION ANALYSIS TRANSACTION 3 SOLUTION (3)+$1,600 +$1,600 Stockholders’ Assets = Liabilities + Equity Accounts Common Cash + Supplies + Equipment = Payable + Stock Old Bal. $8,000 $7,000 $15,000 New Bal. $8,000 + $1,600 + $7,000 = $1,600 + $15,000 $16,600 $16,600 The asset Supplies is increased $1,600 and the liability Accounts Payable is increased by the same amount.

Softbyte, Inc. TRANSACTION ANALYSIS TRANSACTION4 • Softbytereceives $1,200 cash from customers for programming services it has provided. • This transaction represents the principal revenue-producing activity of Softbyte.

TRANSACTION ANALYSIS TRANSACTION 4 SOLUTION (4) +1,200 +1,200 Revenue Assets = Liabilities + Stockholders’ Equity Accounts Common Retained Cash + Supplies + Equipment = Payable + Stock Earnings Old Bal. $8,000 $1,600 $7,000 $1,600 $15,000 New Bal. $9,200 + $1,600 + $7,000 = $1,600 + $15,000 $1,200 $17,800 $17,800 Cash is increased $1,200 and Retained Earnings is increased $1,200.

Bill Softbyte, Inc. Daily News TRANSACTION ANALYSIS TRANSACTION5 Softbytereceives a bill for $250 from the Daily News for advertising the opening of its business but postpones payment of the bill until a later date.

TRANSACTION ANALYSIS TRANSACTION 5 SOLUTION (5) +250 -250 Advertising Expense Assets = Liabilities + Stockholders’ Equity Accounts Common Retained Cash + Supplies + Equipment = Payable + Stock Earnings Old Bal. $9,200 $1,600 $7,000 $1,600 $15,000 $1,200 New Bal. $9,200 + $1,600 + $7,000 = $1,850 + $15,000 $ 950 $17,800 $17,800 Accounts Payable is increased $250, and Retained Earnings is decreased $250.

Softbyte, Inc. Bill TRANSACTION ANALYSIS TRANSACTION6 • Softbyteprovides programming services of $3,500 for customers. • Cash amounting to $1,500 is received from customers, and the balance of $2,000 is billed to customers on account.

TRANSACTION ANALYSIS TRANSACTION 6 SOLUTION (6) +1,500 +2,000 +3,500 Service Revenue Assets = Liabilities + Stockholders’ Equity $21,300 $21,300 Cash is increased $1,500; Accounts Receivableis increased $2,000; andRetained Earnings is increased $3,500.

$600 $900 Softbyte, Inc. $200 TRANSACTION ANALYSIS TRANSACTION7 Expenses paid in cash for September are store rent, $600, salaries of employees, $900, and utilities, $200.

Assets = Liabilities + Stockholders’ Equity TRANSACTION ANALYSIS TRANSACTION 7 SOLUTION (7) -1,700 -600 Rent -900 Salaries -200 Utilities $19,600 $19,600 Cash is decreased $1,700 andRetained Earnings is decreased by the same amount.

Softbyte, Inc. Daily News TRANSACTION ANALYSIS TRANSACTION8 Softbytepays its Daily News advertising bill of $250 in cash.

Assets = Liabilities + Stockholders’ Equity TRANSACTION ANALYSIS TRANSACTION 8 SOLUTION (8) -250 -250 $19,350 $19,350 Cash is decreased $250 andAccounts Payable is decreased by the same amount.

Softbyte, Inc. TRANSACTION ANALYSIS TRANSACTION9 The sum of $600 in cash is received from customers who have previously been billed for services in Transaction 6.

Assets = Liabilities + Stockholders’ Equity TRANSACTION ANALYSIS TRANSACTION 9 SOLUTION (9) +600 -600 $19,350 $19,350 Cash is increased $600 andAccounts Receivable is decreased by the same amount.

$1,300 Softbyte, Inc. TRANSACTION ANALYSIS TRANSACTION10 The corporation pays a dividend of $1,300 in cash to Ray and Barbara Neal, the stockholders of Softbyte, Inc.

Assets = Liabilities + Stockholders’ Equity TRANSACTION ANALYSIS TRANSACTION 10 SOLUTION (10) -1,300 -1,300 Dividends $18,050 $18,050 Cash is decreased $1,300 andStockholders’ Equity is decreased by the same amount.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS Net income of $2,750 shown on the income statement is added to the beginning balance of retained earnings in the retained earnings statement. $ 2,750 Net income of $2,750 is determined from the information in the retained earnings column of the Summary of Transactions (Illustration 1-7).

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS Net income of $2,750 shown on the income statement is added to the beginning balance of retained earnings in the retained earnings statement. 2,750 Net income of $2,750 is determined from the information in the retained earnings column of the Summary of Transactions

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS Net income of $2,750 carried forward from the income statement to the owner’s equity statement. The retained earnings of $1,450 at the end of the reporting period is shown as the final total of the retained earnings column of the Summary of Transactions $ 1,450 Retained earnings of $1,450 at the end of the reporting period shown in the retained earnings statement is shown on the balance sheet.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS Net income of $2,750 carried forward from the income statement to the owner’s equity statement. The retained earnings of $1,450 at the end of the reporting period is shown as the final total of the retained earnings column of the Summary of Transactions 1,450 Retained earnings of $1,450 at the end of the reporting period shown in the retained earnings statement is shown on the balance sheet.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS $ 8,050 Cash of $8,050 on the balance sheet and statement of cash flows is shown as the final total of the cash column of the Summary of Transactions. Cash of $8,050 on the balance sheet is reported on the statement of cash flows.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS $ 8,050 Cash of $8,050 on the balance sheet and statement of cash flows is shown as the final total of the cash column of the Summary of Transactions. Cash of $8,050 on the balance sheet is reported on the statement of cash flows.