Download

1 / 8

80 likes | 220 Views

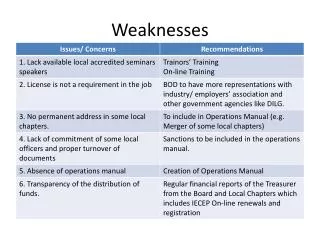

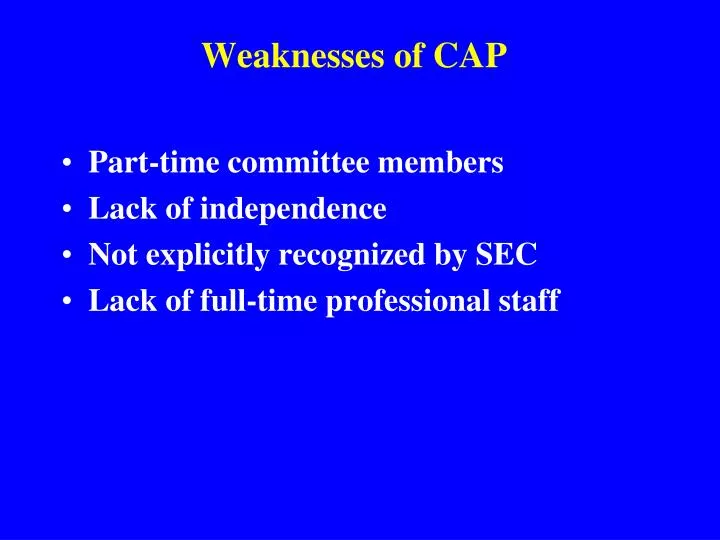

Weaknesses of CAP . Part-time committee members Lack of independence Not explicitly recognized by SEC Lack of full-time professional staff. Weaknesses of CAP (cont.) . Pragmatic approach Lack of conceptual framework No comprehensive statement of accounting principles

E N D

Weaknesses of CAP • Part-time committee members • Lack of independence • Not explicitly recognized by SEC • Lack of full-time professional staff

Weaknesses of CAP (cont.) • Pragmatic approach • Lack of conceptual framework • No comprehensive statement of accounting principles • Inconsistency (e.g., ARB 44 & ARB 44 Rev.) • No research division

Weaknesses of APB • Part-time Board members • Lack of independence • Not explicitly recognized by SEC • Inadequate full-time professional staff

Weaknesses of APB (cont.) • Investment tax fiasco • Pragmatic approach • Lack of conceptual framework • No comprehensive statement of accounting principles

FASB 1973-???? • Trueblood & Wheat Commissions • 7 full-time board members • Operational July 1973 • Independent • Full-time staff • Explicitly recognized by SEC (ASR 150) • Rule 203 acknowledgement • Conceptual framework

Pronouncements of FASB Rule 203 Category A: • FASB Statements • FASB Interpretations

Other Pronouncements Issued by or Associated with FASB • FASB Statements of Financial Accounting Concepts • FASB Technical Bulletins • EITF Abstracts • FASB Staff Positions • FASB Staff Q&As

FASB Codification - 2009 • In 2009 the FASB codified all U.S. GAAP for non-governmental entities into one location • The only authoritative U.S. GAAP is the FASB Codification