Download

1 / 15

150 likes | 162 Views

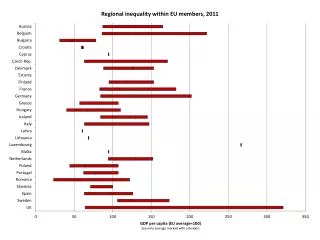

Predicting peaks and troughs in real house prices: a probit approach LIME Workshop Brussels, 8 December 2011 Paul van den Noord. Sharp rebounds Real house prices, index 2009Q1 = 100. Recent developments. Weak or faltering rebounds Real house prices, index 2009Q1 = 100. Recent developments.

E N D

Predicting peaks and troughs in real house prices: a probit approach LIME Workshop Brussels, 8 December 2011 Paul van den Noord

Sharp rebounds • Real house prices, index 2009Q1 = 100 Recent developments

Weak or faltering rebounds • Real house prices, index 2009Q1 = 100 Recent developments

Continued slides • Real house prices, index 2009Q1 = 100 Recent developments

Working off earlier busts • Real house prices, index 2009Q1 = 100 Recent developments

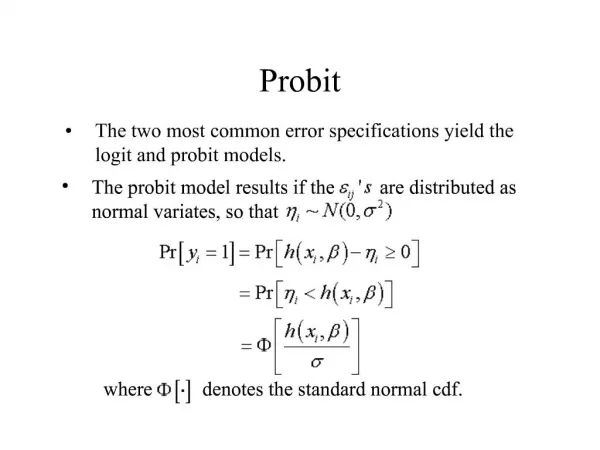

Some unpleasant maths The theoretical model

Some unpleasant maths The theoretical model

Major peaks and troughs Peaks and troughs at least 6 quarters apart “Major” if >15% up T-P and >7½ % down P-T The empirical model Financial Crisis S&L, EMS, Japan OPEC I and II Great Moderation

Estimation results 1970-2005 The empirical model 1. ***, **, * denote significance at the 1, 5, and 10% significance levels, res pectively. P-values (in parentheses) are based on robust standard errors. Explanatory variables are averaged over two quarters (the quarter prior to a peak/trough and the same quarter when a peak/trough occurs), if not stated differently. 2. Refer to changes in percentage points, not in probabilities, and evaluated at the means of the explanatory variables. Semi-elasticity rather than a marginal effect is reported for the log of the long-term interest rate. 3. Averaged over four quarters.

In-sample predictions The empirical model

Out-of-sample predictions: peaks The empirical model

Out-of-sample predictions: troughs The empirical model

Likelihood of troughs Predictions 1. Scenario 1 assumes constant real house prices over the projection period. 2. Scenario 2 assumes constant real house prices over the projection period and 2 percentage points higher interest rates than in the baseline by 2012Q4 (with the difference building up in a linear fashion from 2011Q3 onwards). 3. Scenario 3 assumes increasing real house prices by 10% over the projection period. 4. Scenario 2 assumes increasing real house prices over the projection period and 2 percentage points higher interest rates than in the baseline by 2012Q4 (with the difference building up in a linear fashion from 2011Q3 onwards).

Likelihood of peaks Predictions Note: + indicates a peak based on the cut-off level corresponding to the unconditional probability of a peak. 1. Scenario 1 assumes constant real house prices over the projection period. 2. Scenario 2 assumes constant real house prices over the projection period and 2 percentage points higher interest rates than in the baseline by 2012Q4 (with the difference building up in a linear fashion from 2011Q3 onwards). 3. Scenario 3 assumes increasing real house prices by 10% over the projection period. 4. Scenario 2 assumes increasing real house prices over the projection period and 2 percentage points higher interest rates than in the baseline by 2012Q4 (with the difference building up in a linear fashion from 2011Q3 onwards).

Forecasts Downturns ending? United States*, United Kingdom†, Italy†, Denmark†, Greece**, Ireland**, Korea†, Netherlands†, New Zealand†, Spain** Rebounds ending? France*, Canada*, Australia*, Belgium*, Finland*, Norway*, Sweden** ,Switzerland † Long-term declines ending ? Japan* , Germany** ___________ † No * Yes after a further fall (rise) in real prices ** Also at current real prices The results Source: Authors’ calculations.