Download

1 / 18

180 likes | 290 Views

Estimation and Forecasting of Retail Sales in Florida: An Update. By: Tony Villamil The Washington Economics Group, Inc. Florida Retail Federation Annual Meeting Retailing: Sustaining Your Sails! La Playa Resort, Naples, Florida November 18, 2008.

E N D

Estimation and Forecasting of Retail Sales in Florida: An Update By: Tony Villamil The Washington Economics Group, Inc. Florida Retail Federation Annual Meeting Retailing: Sustaining Your Sails! La Playa Resort, Naples, Florida November 18, 2008

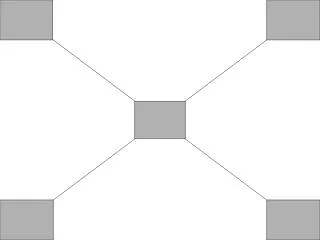

External Macroeconomic Drivers of Economic Activity and Income in Florida: A Framework FLORIDA ECONOMIC AND INCOME GROWTH DRIVEN BY: State's Business Climate US Economy & Financial Markets Developments Florida Global Economy & Financial Markets Developments

Sensitivity of Florida Retail Sales • Population and per-capita income growth accounts for a significant 87 percent of the expected change in overall retail sales • Consumer expectation and month of the year account for a 12 percent change in retail sales • The remaining 1 percent change in retail sales can be attributed to random factors, not accounted by the model

Forecast for Retail Sales in 2009, Adjusted for Inflation andBroken Down by Principal Product and Services Sectors

Statistical Analysis Indicators of Retail Sales

Florida Consumer Confidence Index:A Slight Recovery in 2009 Source: University of Florida BEBR and Forecast (F) by The Washington Economics Group, Inc. Data is based on Dec observations of each year. 2008 is based on Oct data.

$ Crude Oil/Barrel Source: Energy Information Administration (EIA) and Forecast (F) by The Washington Economics Group, Inc. Data is based on Dec observations of each year. 2008 is based on Nov data.

Florida Single-Family Median Home Prices Source: Florida Association of Realtors and Forecast (F) by The Washington Economics Group, Inc. Data is based on Dec observations of each year. 2008 is based on Sep YTD data.

Florida Unemployment Rate Source: Florida Agency for Workforce Innovation and Forecast (F) by The Washington Economics Group, Inc. Data is based on Dec observations of each year. 2008 is based on Sep data.

Declines in Florida Taxable Sales in 2008 Have Been Significant: 2009 a Modest Recovery from Low Levels

Florida Taxable Sales:A Modest Increase for 2009 Source: Florida Economic and Demographic Research Database and Forecast (F) by The Washington Economics Group, Inc. Data is based on Aug observations of each year.

Florida Growth and Total Retail Sales Source: University of Central Florida (UCF), Oct 2008 Forecast.

Florida Non-Agricultural Employment Source: Florida Agency for Workforce Innovation. Data is based on December observation of each year. 2008 growth is based on Sep vs. Sep 2007.

Florida Retail Trade Employment Source: Florida Agency for Workforce Innovation. Data is based on December observation of each year. 2008 growth is based on Sep vs. Sep 2007.

Concluding Observations • A modest recovery in Retail Sales expected in 2009, from the low levels experienced in 2008 • It is unlikely that total Retail Sales will reach 2004 levels next year, but a recovery is likely to gather momentum in the last quarter of 2009 • Monetary and fiscal policies are highly stimulative of an economic recovery late in 2009 • Financial federal package now geared to support consumer credit

The Washington Economics Group, Inc. 2655 LeJeune Road, Suite 608 Coral Gables, Florida 33134 Phone: 305-461-3811 www.weg.com info@weg.com