Download

1 / 5

50 likes | 262 Views

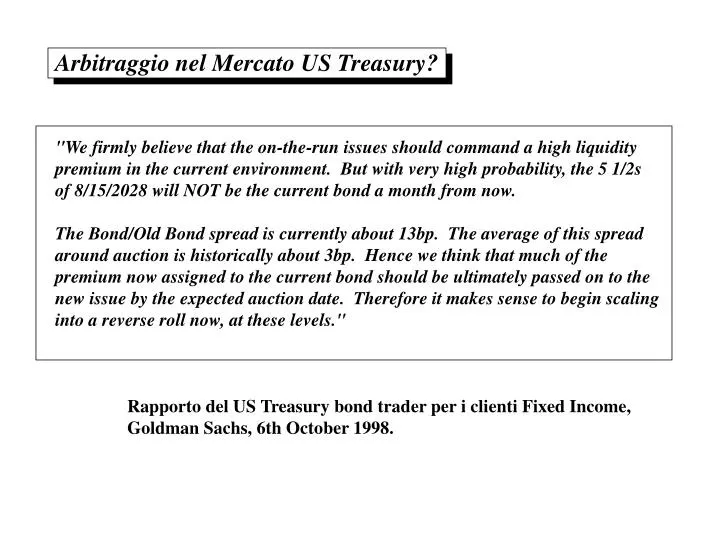

Arbitraggio nel Mercato US Treasury?. "We firmly believe that the on-the-run issues should command a high liquidity premium in the current environment. But with very high probability, the 5 1/2s of 8/15/2028 will NOT be the current bond a month from now.

E N D

Arbitraggio nel Mercato US Treasury? "We firmly believe that the on-the-run issues should command a high liquidity premium in the current environment. But with very high probability, the 5 1/2s of 8/15/2028 will NOT be the current bond a month from now. The Bond/Old Bond spread is currently about 13bp. The average of this spread around auction is historically about 3bp. Hence we think that much of the premium now assigned to the current bond should be ultimately passed on to the new issue by the expected auction date. Therefore it makes sense to begin scaling into a reverse roll now, at these levels." Rapporto del US Treasury bond trader per i clienti Fixed Income, Goldman Sachs, 6th October 1998.

TERMINOLOGIA On-the-run: L’emissione piu’ recente di un Treasury bond relativamente ad un qualsiasi settore (es. segmento 10anni, segmento 30anni) della curva dei rendimenti The Current Bond: La piu’ recente emissione del US Treasury bond Trentennale (spesso abbreviato semplicemente "The Bond"). The Old Bond: La seconda piu’ recente emissione di un US Treasury a 30 anni. Bond/Old Bond spread: La differenza di rendimento (yield) tra l’emissione piu’ recente e la precedentethe dei Treasuries trentennali. Basis point (bp): 1/10,000 = 1/100 * 1% = 0.01%

Yield Yield 3bp 2/28 5/28 8/28 Tutti questi Bonds sono nel “settore” 30anni della yield curve. 1 5 10 30 Bond Maturity (anni) Il rendimento sull’ "on-the-run" bond a 30anni é piu’ basso di altri bonds simili => vale di piu’: PERCHE’ ? Maturity diversa? Miglior Credito? Liquidità? Yield Curve NO NO SI!

Bid-offer spread piu’ contenuto Costi di transazione piu’ bassi per velocizzare e facilitare le transazioni Vale di più (=> yield più basso ) Proprietà del Bond on-the-run Questo Premio di Liquidità é storicamente stimato circa 3bp … Allora perchè oggi vale 13bp ? Perchè c’è un extra 10bp? Potrebbe trattarsi di un Arbitragggio? Il Goldman Sachs US Treasury bond trader la pensa così!

La strategia di arbitraggio OGGI UN MESE DOPO Yield Yield 13bp 13bp 2/28 5/28 8/28 2/28 5/28 8/28 11/28 Vendere 8/28 ( l’attuale bond "on-the-run“) Ri-comprare 8/28 (l’attuale"old" bond) Compreare 5/28 ( l’attuale "old bond") Vendere 5/28 (l’attuale "old old bond") Profitto Netto: 13bp (poichè l’ on-the-run è 13bp più costoso dell’old bond). Costo Netto: zero (ora il costo dei due bond è lo stesso; il premio di liquidità è ora sul nuovo bond "on-the-run"