Download

1 / 17

170 likes | 175 Views

Learn about expenses and revenues in accounting, including their definitions, types, and how they are reported on the income statement. Gain a solid understanding of these fundamental concepts in financial management.

E N D

Discipline: Basis of accountingTheme 2: Expenses and Revenues of companies Lecturer: Vornicova Natalia, Master of Economic Sciences Chisinau 2019

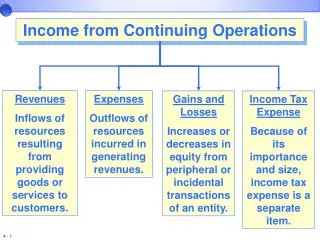

Expenses are outflows or other using up of assets or incurrence of liabilities (or acombination of both) from delivering or producing goods, rendering services, or carrying outother activities that constitute the entity's ongoing major or central operations.

Expenses represent actual or expected cash outflows (or the equivalent) that have occurredor will eventuate as a result of the entity's ongoing major or central operations. The assets that flow out or are used or the liabilities that are incurred may be of various kinds—for example,units of product delivered or produced, employees' services used, kilowatt hours of electricity used to light an office building, or taxes on current income.

Similarly, the transactions and events from which expenses arise and the expenses them selves are in many forms and are called by various names for example, cost of goods sold, cost of services provided, depreciation, interest, rent, and salaries and wages depending on the kinds of operations involved and the way expenses are recognized.

Revenues are inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity's ongoing major or central operations. Revenues represent actual or expected cash inflows (or the equivalent) that have occurredor will eventuate as a result of the entity' s ongoing major or central operations.

The assets increased by revenues may be of various kinds for example, cash, claims against customersor clients, other goods or services received, or increased value of a product resulting from production. Similarly, the transactions and events from which revenues arise and the revenues themselves are in many forms and are called by various names for example: output, deliveries, sales, fees, interest, dividends, royalties, and rent depending on the kinds of operations involved and the way revenues are recognized.

An expenseis reported on the income statement. An expense is a cost that has expired, was used up, or was necessary in order to earn the revenues during the time period indicated in the heading of the income statement. For example, the cost of the goods that were sold during the period are considered to be expenses along with other expenses such as advertising, salaries, interest, commissions, rent, and so on.

An expenditure is a payment or disbursement. The expenditure may be for the purchase of an asset, a reduction of a liability, a distribution to the owners, or it could be an expense. For instance, an expenditure to eliminate a liability is not an expense, while expenditures for advertising, salaries, etc. will likely be recorded immediately as expenses.

Here's another example to illustrate the difference between an expense and an expenditure. A company makes anexpenditure ofUSD255,500 to purchase equipment. The expenditure occurs on a single day and the equipment is placed in service. Assuming the equipment will be used for seven years, the cost of the equipment will be reported as depreciation expense of $100 per day for the next 2,555 days (7 years of service with 365 days each year).

Types of Revenue (Income) • Sale of Products-Amounts earned from the sale of merchandise. • Sale Of Services-Amounts earned from performing services. • Rental Income-Amounts earned from renting properties. • Interest Income-Amounts earned from investments.

Types of Expenses • Supplies-Expenditures for incidental materials needed in the conduct of business, such as office supplies. • Salaries-Expenditures for work performed by employees. • Payroll Taxes-Expenditures for taxes based on wages paid to employees. • Advertising-Promotional expenditures, such as newspapers, handbills, television, radio and mail.

Utilities-Expenditures for basic services needed to function, such as water, sewer, gas, electricity and telephone. • Building Rental-Expenditures paid to an owner of property (building) for use of the property. A rental agreement called a lease contains the terms. • Maintenance & Repairs-Expenditures paid to repair and or maintain buildings and/or equipment.

Profit • Profit is a financial benefit that is realized when the amount of revenue gained from a business activity exceeds the expenses, costs, and taxes needed to sustain the activity. Any profit that is gained goes to the business's owners, who may or may not decide to spend it on the business. Profit is calculated as total revenue less total expenses.

Losses • Losses are a one-time removal or decrease in a business resource or asset. Losses are unrecoverable and unanticipated

Profit/Losses – financial result • Profit/Losses are recorded and displayed in one of two reports, depending on the type of loss: • Profit/Losses that result from events that are not related to the primary operations of a business are recorded in the profit and loss statement. • Profit/Losses that do result from events that are directly related to the operations of the business are recognized in the balance sheet.