Download

1 / 8

80 likes | 217 Views

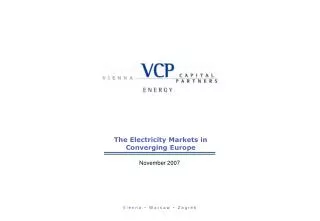

The Electricity Markets in Converging Europe. November 2007. Executive Summary . Rising electricity demand and decommissioning of outdated power plants in Converging Europe causes significant investment needs in the electricity sector of the Region

E N D

The Electricity Markets in Converging Europe November 2007

Executive Summary • Rising electricity demand and decommissioning of outdated power plants in Converging Europe causes significant investment needs in the electricity sector of the Region • Supply of renewable energy is not sufficient to comply with Kyoto targets and directives of European Commission • Convergence with the Western Europeanstandards due to market opening and elimination of market distortion mechanisms • Electricity market liberalisation and harmonisation of the frameworks with the EU standards establish the preconditions for well-functioning electricity markets • Privatisation of power plants is progressing or being prepared in many countries of the Region • Major European energycompanies (E.ON, RWE, Enel, EdF, GdF, CEZ, EVN, Verbund) are present in the Region in electricity generation and distribution sector

Electricity Prices and Consumption Electricity consumption per capita 2006 • Electricity consumption in the Region still remains up to 50% below the EU-15 average despite strong growth in recent years • Regional electricity prices are lower than EU-15 average but have experienced strong growth in recent years • Further growth of electricity prices will be caused by low efficiency levels of local electricity generators and decommissioning of old power plants • The accelerating liberalisation process will increase market efficiency Source: UCTE Electricity prices* 2006 • Source: Eurostat * Electricity prices for industrial customers with annual consumption up to 2 GWh

Net electricityexporter Energy flows in TWh Net electricityimporter Energy Flows in the Converging Europe • The main electricity importers in the Region are Hungary and Croatia and the major electricity exporters are Poland and Czech Republic. Turkey is expected to experience a significant shortage of electricity supply in the near future • The expected decommissioning of outdated power plants will influence the export/import capacities of certain countries (e.g. Bulgaria, Slovakia) • The outdated infrastructure and long-term contracts decrease cross border transmission capacities • By 2020 up to 16,400kV of cross-border transmission lines shall be added or modernised in the Region • The ongoing harmonisation of the electricity markets develops the potential for international electricity trading Energy flows in 2006 Source: UCTE * Albania is synchronised with UCTE ** Data for Montenegro is not available

Major International Players – Regional Overview Poland Czech Republic Slovakia Hungary Slovenia Romania Croatia Bosnia & Herzegovina Serbia Bulgaria Macedonia Turkey Albania Greece Source: VCP

Growth Opportunities in the Region (1) P O L A N D C Z E C H R E P U B L I C • Decommissioning of coal fired power plants (3,500 MW) until 2015 • Generation capacities are outdated (40% are more than 35 years in service) • The state-owned companies BOT Group and PKE SA possess 44% and 18% of generation capacities respectively • The dominant market position of CEZ (70% of electricity generation) affects the market attractiveness negatively PL S L O V A K I A CZ • Enel controls more than 85% of the electricity generation • The decommissioning of nuclear power plant will turn Slovakia into an electricity importer H U N G A R Y SK • Hungary is particularly attractive for Greenfield projects • 64% of the generation capacities (including NPP PAKS) belongs to the state-owned MVM. The privatisation of a minority stake (25%) via public offering is planned • The privatisation of Vertes coal PP is in process • Several power plant construction projects were announced • Strong increase of the electricity prices over the past 5 years (CAGR 6.5% ) HU SL S L O V E N I A • The electricity generation is state-owned (97% belongs to HSE) • HSE intends to expand into Balkan states and CEE markets Source: VCP

Growth Opportunities in the Region (2) EX-YUGOSLAVIA R O M A N I A • In the countries of former Yugoslavia the electricity generation is mostly state-owned • Only Macedonia is an exception: the distribution network was privatised and the Negotino TPP was acquired by „Hitch & MacDonald” (Canada) • In BiH CEZ will reconstruct and increase the capacities of Gacko coal PP • The shortage of capital (investment) in the Region creates attractive opportunities for green field projects • Privatisation of the generation capacities is envisaged to start in the coming years • Generation capacities are generally outdated and require high investments • Privatisation of generation sector is prearranged to start in 2007 with privatisation of Turceni (2,310 MW), Rovinari (1,320 MW) and Craiova (610 MW) • Privatisation of 16 small HPP (up to 10 MW) will be conducted in 2007 RO HR BiH SRB B U L G A R I A BG MNE • After the privatisation of the distribution companies, the privatisation of TPP and district heating companies is expected to be completed in the near future • High investment need due to outdated and environment-unfriendly power plants • The privatisation of Bobovdol coal PP (630 MW) is scheduled for 2008 • 48% of generation capacities (mostly HPPs) belong to the state-owned company NEK EAD • The shut down of 2 units at Kozloduy NPP (880 MW) and the gradual closing of the old TPPs coupled with the delay in the construction of NPP Belene resulted in decreasing of exports to almost zero and may turn Bulgaria into electricity importer in the coming years TR MK AL GR T U R K E Y • Electricity market with strong prospects (attractive prices and significant demand growth) • Privatisation of distribution assets is scheduled for 2008 • Generation assets are mostly controlled by local companies • Realisation of the Ilisu Dam (1,200 MW HPP) project is still debatable Source: VCP

Disclaimer This presentation was prepared by VCP Capital Partners Unternehmensberatungs AG (“Vienna Capital Partners” or “VCP”). The information in this presentation reflects prevailing conditions and our judgement as of this date, all of which are accordingly subject to change. In preparing this presentation, VCP has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. No representation or warranty, expressed or implied is given by VCP as to the accuracy or completeness of the information. No responsibility or liability whatsoever is accepted by any person for any errors, misstatements or omissions in this document.