Download

1 / 14

140 likes | 230 Views

Nokia cellphone financing program. objectives. To complement Mobile Phone Banking Services To increase loan portfolio To provide flexible payment facility to clients without credit cards. Brief History. Signed MOA last July 11, 2008 Partners: Nokia, Altus, Presnet & Megacellular

E N D

objectives • To complement Mobile Phone Banking Services • To increase loan portfolio • To provide flexible payment facility to clients without credit cards

Brief History • Signed MOA last July 11, 2008 • Partners: Nokia, Altus, Presnet & Megacellular • Launched in pilot branches last August 2008 • Pilot Branches: Ibaan, Batangas, Mabini • Rolled out to other branches last September 2008 • At present: 217 clients, sold 349 cellphones, disbursed P3.1M in loans

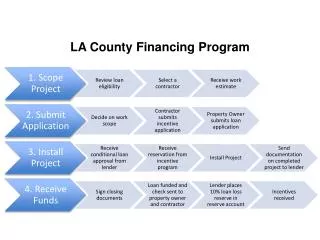

An Account Officer (AO) offers the product to an eligible borrower AO computes for maximum loanable amount. Own-a-Nokia Cellphone Loan AO prepares a Notice of Loan Approval (NLA) in triplicate. AO keeps a copy of the NLA. The 2 other copies will be given to the Nokia retailer hand carried by the client. Retailer NLA Client presents NLA to retailer. NLA NLA

Retailer verifies identification of client by asking for an ID and calling the BOH. Client picks a cellphone and signs Sales Invoice. Retailer keeps both copies of NLA. Retailer sends billing statement, sales invoice and one copy of NLA to the bank. Bank processes the loan release. Bank deposits loan proceeds to the account of the retailer. Bill Retailer S.I. Retailer issues an OR once payment is received. NLA

observations • More than 70% of clients are individual MF borrowers. Regular loan clients may have access to cheaper financing through credit cards. • Clients prefer mid-range models. • Reason for purchase is for personal use. • A good number of clients buy more than 1 cellphone.

Feedback from clients • Easy & simple terms • Affordable • No documentary requirements • Quick processing

Feedback from bank • Simple process flow • Low risk because offered to borrowers with existing relationship • Good marketing tool (incentive for good borrowers)

Areas of concern • 3 branches cannot participate due to lack of nearby retailers • Effects of business slow down felt at the start of the year • Repair of cellphone

Factors of success • Support & Strategy of Branch Manager and Account Officers • Location of Retailer • Cooperation from Retailer • Marketing Collaterals