Download

1 / 12

120 likes | 228 Views

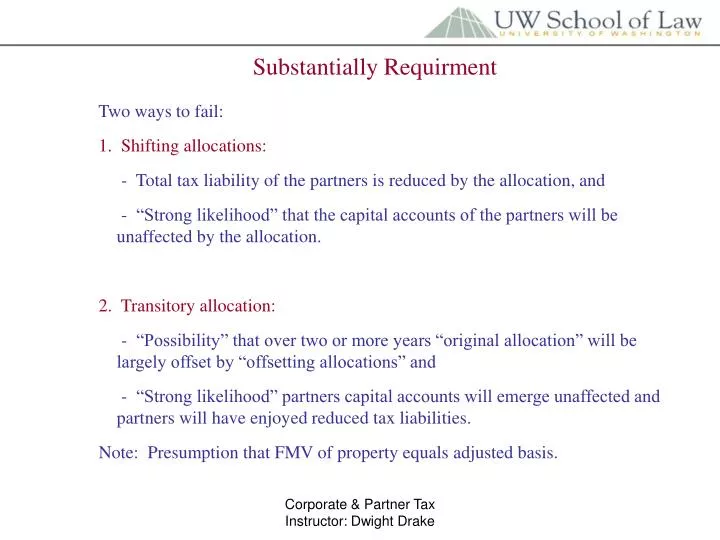

Substantially Requirment. Two ways to fail: 1. Shifting allocations: - Total tax liability of the partners is reduced by the allocation, and - “Strong likelihood” that the capital accounts of the partners will be unaffected by the allocation. 2. Transitory allocation:

E N D

Substantially Requirment Two ways to fail: 1. Shifting allocations: - Total tax liability of the partners is reduced by the allocation, and - “Strong likelihood” that the capital accounts of the partners will be unaffected by the allocation. 2. Transitory allocation: - “Possibility” that over two or more years “original allocation” will be largely offset by “offsetting allocations” and - “Strong likelihood” partners capital accounts will emerge unaffected and partners will have enjoyed reduced tax liabilities. Note: Presumption that FMV of property equals adjusted basis. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. LP buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration. (a) Breakeven except for depreciation. Capital accounts end of year: A equal 100k; B equal 80k (100k less 20k depreciation). (b) Sale building Jan 1, year 2 for 180k? How allocate proceeds? 100k A; 80k B. If sell for 200k? 20k gain allocated equally. A capital account goes to 110k and B’s goes to 90k. Proceeds distributed accordingly. (c) What if agreement says gain first allocated to extent of cost recovery deductions? Then, all 20k to B. Both capital accounts at 100k, and 200k proceeds distributed equally. Note: No “substantial” issue because of Reg. presumption that FMV of property equals basis. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. Lp buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration/ (d) No deficit restoration, but B has qualified income offset. - What effect year 1? Nothing – capital account positive. - What effect year 6? Depreciation first 5 years will zero out B’s capital account. Year 6 allocation would produce negative balance that would have no have economic effect. Thus, for year 6, must look to which partner bears loss by comparing liquidation at beginning of year with liquidation at end. Net impact is that amount equal to depreciation in year 6 is born by A (reduce positive balance), so would be allocated to A, whose account would drop to 80k. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. Lp buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration/ (e) What result in (d) if B contributed promissory note for 100k? - Note not satisfy unconditional deficit restoration obligation (primary test). Thus no impact under primary “economic effect” test until paid. - But note does constitute limited obligation to restore under alternative test if due by later of end of tax year of liquidation or 90 days after liquidation. Thus, under alternative test, year 6 depreciation allocated to A. - Note: Note not increase A’s outside basis. So, 704(d) basis limitation would kick in and require carryover until A gets some outside basis by paying note or some other means in later years. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. Lp buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration/ (f) Same as (e), but yr 6 value is 400k, partners borrow 200k recourse and distribute equally to themselves early yr 7. - Year 1 to 5 allocation to B still good because no negative capital account. - Refi proceeds distribution in yr. 7 “reasonably expected”, so under alternative test wipe out effect of B’s 100k note. So 20k deduction in year 6 can’t be allocated to B under alternative because would take negative. - Thus, both primary and alternative tests fail. Must look to partnership interests. Although 20k allocation to A would take A negative after refi proceeds, A is GP so has duty to restore to pay off recourse creditors. Thus, A gets 20k depreciation allocation in year 6. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. Lp buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration/ (g) Same as (f), but yr 6 value is 300k, partners and partners agree that when hit 400k, then will refi on recourse basis and distribute 200k. Here, the “reasonable expectation” test of future distribution not satisfied because property FMV assumed to equal basis at all times – will never get to 400k. Thus, B gets 20k year 6 depreciation under alternative test by virtue of 100k note to partnership. (h) Assume no deficit restoration or qualified income offset? Year 1 depreciation – to B if agreement says liquidate per positive capital account balances (all positive in year 1). Year 6: All to A because B account would go negative and thus no economic effect. Note: same result as under alternative test. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 -1 Basic Facts: A & B each contribute 100k cash to LP. A is GP; B is LP. Lp buys office bldg for 200k – 10 yr life straight line. All depreciation allocated to B; all other items equally shared. Complete deficit restoration/ (i) Same as (h) – no deficit restoration or qualified income offset – but B gave 100k promissory note. Issue: Is note relevant for determination the partners interests? If so, year 6 depreciation would go to B. Regs say nothing. Many think is it and that note should be considered even though not increase outside basis. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 - 2 Basic Facts: C and D equal partners of GP. D is non-resident alien. All foreign source income allocated to D, who exempt from US tax. US and foreign source income uncertain. Economic effect assumed. All US income to A and foreign source income to B? Allocation OK because income sources uncertain. No “substantial” issue if allocation may diminish after-tax yield to partners, which is possible here. What if all income shared equally, but D given priority of foreign source for D’s one-half ? Fail “substantial” requirement. This impermissible shifting. D’s taxable income goes down with not corresponding diminishing effect on any of the partners. What result in (a) if it is relatively certain US and foreign income will be roughly equal? Fail “substantial” test. Strong likelihood D will save taxes and capital accounts of the partners will not change. Impermissible “Shifting”. Corporate & Partner Tax Instructor: Dwight Drake

Problem 153 - 3 Basic Facts: E contributes 990k as LP; F contributes 10k as GP. Purchase 1 mill equipment. All 168 cost recovery deductions to E; 99% income to E until recovered cost recovery deductions and all losses. Then, 50 -50. Assume primary “economic effect” test satisfied. Any “substantial” issue? Maybe. - Note: This not gain charge back provision, which would be OK. This is shifting allocation provision and may be “transitory” and thus fail “substantial” test. - If it appears cost recovery deductions will not be recovered for at least five years, using FIFO assumption, then probably not “transitory.” If recovered within 5 year period based on projections, then run big “transitory” risk. Corporate & Partner Tax Instructor: Dwight Drake

Four Part Test For Nonrecourse Deduction Allocation 1. First two Primary requirements met. 2. Nonrecourse deductions are allocated during life of partnership on basis that is “reasonable consistent” with the manner some other significant item is allocated. 3. Partnership agreement contains minimum gain chargeback provision. 4. All other allocations and capital account adjustments are in accordance with 704 Regs. Corporate & Partner Tax Instructor: Dwight Drake

Problem 162 Basic Facts: L contributes 320k as LP; G contributes 80k as GP. Borrow 1.6 mill non-recourse and buy 2 mill property. Loan requires interest only for 5 years. - Income, gains, losses allocated 80-20 until income and gains for first time exceed losses – then 50-50. - First two primary tests met – only G has deficit restoration. L has qualified income offset and minimum gain chargeback. - Non-liquidating distributions 80-20 until return of 400k; then 50-50. - STL 10 year depreciation of building. - Clear over long-term that income and gains will exceed losses. Corporate & Partner Tax Instructor: Dwight Drake

Problem 162 Year 1 Year 2 Year s Depreciation and loss 200k 200k 200k G Capital account 40k (80-40) 0 (40-40) -40 (0-40) L Capital acount 160k (320-160) 0 (160-160) -160 (0-160) Note: Years 1 and 2: No “nonrecource deductions” because no increase in minimum gain (NR liability in excess of basis). So allocations permitted under normal rules – primary test satisfied for G and Alternative test for L. Year 3: Nonrecourse deduction of 200k – excess of NR liability over basis. This 200k allocation OK because 4 part test met. Corporate & Partner Tax Instructor: Dwight Drake