Download

1 / 8

80 likes | 85 Views

This article discusses the benefits of extending duration in a low and rising interest rate environment. It highlights the steepness of the yield curve and the potential for yield pickup and curve flattening. The article also presents a sample scenario on how changes in rates and the steepness of the curve could affect portfolio performance.

E N D

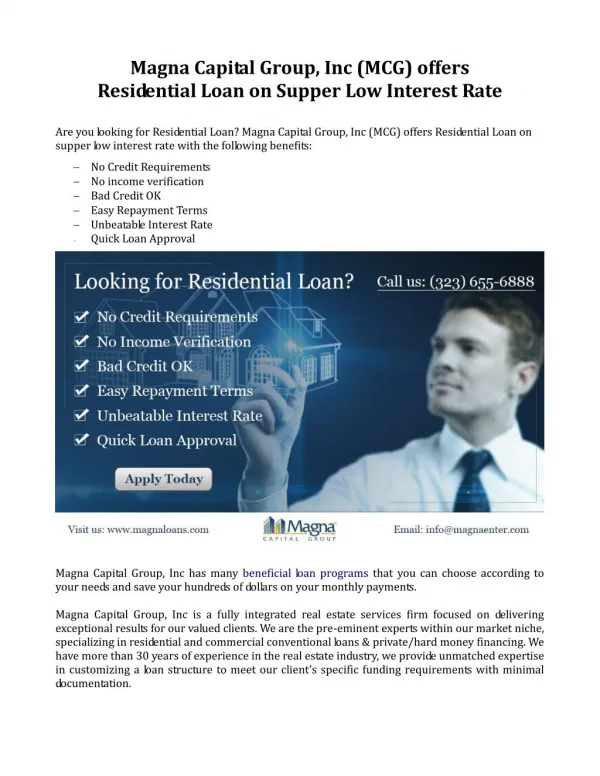

De-risking in a Low and Rising Interest Rate Environment Gary Knapp, CFA, FRMManaging Director, Liability-Driven StrategiesPrudential Fixed Income Please see “Notice Page” in the appendix for important disclosures regarding the information contained herein. The comments, opinions and estimates contained herein are based on and/or derived from publicly available information from sources that Prudential Fixed Income believes to be reliable. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. November 2011 CONFIDENTIAL – FOR EDUCATIONAL PURPOSES ONLY – NOT FOR FURTHER DISTRIBUTION

Is Now The Time To Extend Duration? Key Considerations • Long-term rates are not nearly as low as short-term rates • Treasury curve is unusually steep between intermediate and long-term bonds • Extending to long duration outperforms intermediate bonds in many scenarios • If long rates rise sharply, the effects on equities may be larger than on bonds

Is Now The Time To Extend Duration? Steepness of Yield Curve Offers Unique Opportunity • US Treasury curve remains historically steep from intermediate- to long-term maturities, the key maturity range for pension plans • Difference between 10- and 30-year US Treasury yields was 100 bps (as of 9/30/11), well above average yield differential of 30 bps since January 1980 • Historically, the curve steepens during periods of accommodative monetary policy and then flattens as the Federal Reserve begins raising short-term rates Federal Funds Rate and U.S. Treasury Yields As of September 30, 2011 Yield (%) Bps Average Spread Source of data: Bloomberg. Source of calculations: Prudential Fixed Income.

How Extending Duration Affects Asset Portfolio Risk Current Steepness of Yield Curve Compensates Investors For Extending Now • Extending from an intermediate fixed income portfolio to a long duration will increase portfolio interest rate risk • However, current steepness of the curve allows a long duration strategy to provide a much higher yield, which we believe helps compensate for this additional risk • A plan can now add more than 1.6% yield to its fixed income portfolio by moving from intermediate to long duration strategy Barclays Aggregate Bond and Long Duration Government/Credit Indices As of September 30, 2011 Yield pick-up: 1.66%Duration increase: 9.25 yrs Source of benchmark data: Barclays. Source of calculations: Prudential Fixed Income.

Long-Term Yield Differential Supports Extending Duration Now Two Key Factors: Yield Pickup and Curve Flattening • Historic yield pickup: Current yield differential of 166 bps is close to historic levels, offering 95 bps more yield than the 20 year average • Prospect for curve flattening: Yield differential lies 1.6 standard deviations from its historic average suggesting probability of curve flattening is higher than the probability it will continue to steepen Yield Differential Between Intermediate And Long Duration StrategiesBarclays Aggregate Bond Index vs. Long Duration Government/Credit Index January 1, 1990 to September 30, 2011 Bps Historically high yield differential Average Yield Differential Curve would have to flatten 95 bps to return to historical avg. Extending now to a long duration strategy could provide more attractive returns than continuing to invest in an intermediate strategy over time Source of data: Bloomberg. Source of calculations: Prudential Fixed Income.

How Changes In Rates and Steepness of the Curve Could Affect Performance Sample Scenario: Yield Curve Flattens - Short and Intermediate Rates Rise More Than Long-Term Rates • How the Asset Portfolio Would Perform: • Over one-year, intermediate portfolio and long duration portfolio would have similar returns, if long-term interest rates rise about half as much as intermediate-term rates • Over two-year, long duration portfolio would outperform provided intermediate-term rates do not rise by more than +150 bps, and long-term rates do not increase by more than +75 bps Short and Intermediate Rates Rise More Than Long-Term Rates Hypothetical Total Return of Intermediate vs. Long Duration Strategies As of September 30, 2011 Approximate breakeven points Reflects the hypothetical yield increase of each index. Source of underlying data: Barclays Capital. Source of calculation: Prudential Fixed Income. For illustrative purposes only. The total return calculations shown are hypothetical and reflect the sum of 1) the beginning yield of the index and 2) the change in value based on the duration of the index and change in the level of interest rates. Yield and duration index data is as of September 30, 2011.

Is Now The Time To Extend Duration? We Believe Extending Duration Of An Existing Fixed Income Strategy Is A Move In The Right Direction • Historically steep yield curve provides a generous yield pick-up • When the Fed begins to tighten, the curve is likely to flatten going forward, giving a long duration strategy the potential to outperform an intermediate strategy • Intervention by governments likely to keep long-term rates range-bound • A sharp rise in long-term rates could be worse for equities than long duration bonds • Corporate spreads likely to tighten as demand from pension plans increases As of September 30, 2011.

Notice Prudential Investment Management is the primary asset management business of Prudential Financial, Inc. Prudential Fixed Income is Prudential Investment Management’s largest public fixed income asset management unit and operates through Prudential Investment Management, Inc. (PIM), a registered investment advisor. Prudential, the Prudential logo and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide. The information contained herein is provided by Prudential Fixed Income. This document may contain confidential information and the recipient hereof agrees to maintain the confidentiality of such information. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of its contents, without the prior consent of Prudential Fixed Income, is prohibited. Certain information in this document has been obtained from sources that Prudential Fixed Income believes to be reliable as of the date presented; however, Prudential Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. Prudential Fixed Income has no obligation to update any or all such information; nor do we make any express or implied warranties or representations as to its completeness or accuracy. Any information presented regarding the affiliates of Prudential Fixed Income is presented purely to facilitate an organizational overview and is not a solicitation on behalf of any affiliate. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services. These materials do not constitute investment advice and should not be used as the basis for any investment decision. These materials do not take into account individual client circumstances, objectives or needs. No determination has been made regarding the suitability of any securities, financial instruments or strategies for particular clients or prospects. The information contained herein is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. Any discussion of risk management is intended to describe Prudential Fixed Income’s efforts to monitor and manage risk but does not imply low risk. All performance targets contained herein are subject to revision by Prudential Fixed Income and are provided solely as a guide to current expectations. There can be no assurance that any product or strategy described herein will achieve any targets or that there will be any return of capital. Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. The securities referenced may or may not be held in portfolios managed by Prudential Fixed Income and, if such securities are held, no representation is being made that such securities will continue to be held. These materials do not purport to provide any legal, tax or accounting advice. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation.