Download

1 / 51

510 likes | 915 Views

my money Investment Risk Profiler. Your investment fund choices. Passive. Active/Growth ... Sun Life Financial Money Market Fund. Sun Life Financial 1,3 & 5 year ...

E N D

1. Introduce yourself � name, background, purpose of meeting, where you want people to ask questions (throughout or wait to end)

Introduce yourself � name, background, purpose of meeting, where you want people to ask questions (throughout or wait to end)

2. Review slideReview slide

3. We will now take a look at the importance of saving for retirement and the impact that long term growth will play on achieving our retirement goals.

Let�s get started�

We will now take a look at the importance of saving for retirement and the impact that long term growth will play on achieving our retirement goals.

Let�s get started�

4. How much you need to save will depend on how much income you need after you retire.

Financial planners suggest that in most cases, Canadians will need to replace between 65% and 80% of their pre-retirement income, in order to maintain their current lifestyle.

For example, if you make a $40,000 a year income before retiring, and you want to replace your income at a 65% level, then you�ll require $26,000 each year in retirement. If you want to replace your income at an 80% level, you�ll require $30,000 each year in retirement.

How much you need to save will depend on how much income you need after you retire.

Financial planners suggest that in most cases, Canadians will need to replace between 65% and 80% of their pre-retirement income, in order to maintain their current lifestyle.

For example, if you make a $40,000 a year income before retiring, and you want to replace your income at a 65% level, then you�ll require $26,000 each year in retirement. If you want to replace your income at an 80% level, you�ll require $30,000 each year in retirement.

5. There are 3 main sources of potential income for retirees:

Primary sources of income are considered a company sponsored retirement plan, like your Friesens group RRSP and Deferred Profit Sharing Plan as well as RRSPs that you may have at financial institutions.

2. Secondary sources of income could be derived from other personal savings � such as bank accounts, stock and bonds, a long with the equity you�ve built in your home or income you generate from rental properties.

3. Suplementary sources of income could be derived from government plans like the Canada Pension Plan (CPP) or Old Age Security (OAS).

All of these sources of income together work to provide you with a certain level of retirement incomeThere are 3 main sources of potential income for retirees:

Primary sources of income are considered a company sponsored retirement plan, like your Friesens group RRSP and Deferred Profit Sharing Plan as well as RRSPs that you may have at financial institutions.

2. Secondary sources of income could be derived from other personal savings � such as bank accounts, stock and bonds, a long with the equity you�ve built in your home or income you generate from rental properties.

3. Suplementary sources of income could be derived from government plans like the Canada Pension Plan (CPP) or Old Age Security (OAS).

All of these sources of income together work to provide you with a certain level of retirement income

6. Government benefits consist of the Canada or Quebec Pension plan which all working individuals contribute to, and Old age Security, which is a non-work related pension paid to all Canadians once they reach age 65.

For 2008 the maximum monthly CPP pymt is $884.58, although the average monthly benefit paid to retired Canadians in 2007 was $480.86.

For the OAS the maximum monthly pymt is $502.31, and the average monthly benefit paid to retired Canadians in 2007 was $476.37.

The CPP payments are indexed annually, and the OAS payments are indexed quarterly based on cost of living increases.

The amount of CPP payments you will personally receive is based on how much and how long you have contributed.

To request your CPP/QPP contribution and benefits statement, check the CRA website at www.sdc.gc.ca.

Old age security is payable to all Canadians who meet certain residency requirements.

Government benefits consist of the Canada or Quebec Pension plan which all working individuals contribute to, and Old age Security, which is a non-work related pension paid to all Canadians once they reach age 65.

For 2008 the maximum monthly CPP pymt is $884.58, although the average monthly benefit paid to retired Canadians in 2007 was $480.86.

For the OAS the maximum monthly pymt is $502.31, and the average monthly benefit paid to retired Canadians in 2007 was $476.37.

The CPP payments are indexed annually, and the OAS payments are indexed quarterly based on cost of living increases.

The amount of CPP payments you will personally receive is based on how much and how long you have contributed.

To request your CPP/QPP contribution and benefits statement, check the CRA website at www.sdc.gc.ca.

Old age security is payable to all Canadians who meet certain residency requirements.

7. Time is your greatest asset when savings for the long term, and you don�t need to set aside a lot to reap the benefits.

Here we have two investors, one is 25 years old and the other is 45 year old. The 25 year old begins contributing $500 a year for 40 years and the 45 year old contributes $1000 a year for 20 years. The contribution amount is the same for both but what is drastically different is the amount of money they each have in their retirement savings at age 65. Assuming a 6% rate of return the 25 year old has $118,193 in retirement savings where as the 45 year old has $45,045, that�s a difference of $ 73,148.

It�s never too late to start contributing to a retirement savings plan but the earlier you start the more savings you will have when you retire.

Time is your greatest asset when savings for the long term, and you don�t need to set aside a lot to reap the benefits.

Here we have two investors, one is 25 years old and the other is 45 year old. The 25 year old begins contributing $500 a year for 40 years and the 45 year old contributes $1000 a year for 20 years. The contribution amount is the same for both but what is drastically different is the amount of money they each have in their retirement savings at age 65. Assuming a 6% rate of return the 25 year old has $118,193 in retirement savings where as the 45 year old has $45,045, that�s a difference of $ 73,148.

It�s never too late to start contributing to a retirement savings plan but the earlier you start the more savings you will have when you retire.

8. Now we will look a closer look at Layfield Group Ltd. Retirement savings plan and the benefits of participating

Now we will look a closer look at Layfield Group Ltd. Retirement savings plan and the benefits of participating

9. There are four key players that have different roles and responsibilities within a company plan.

The first one is your employer who provides the framework of your company�s retirement and savings plan.

An important component to your group plan is employer contributions.

Layfield has a pension committee who select the record keeper to administer your plan. Please inform members who is on the pension committee; Cam Martin; employee representative

Gary Pinkerton; CFO

Derek Bennett; HR Manager

They also select the investment managers and the funds from which you can choose.

And they are responsible for monitoring the plan and provide opportunities for member education.

As the record keeper Sun Life Financial tracks your investments and develops tools you need to be informed about your retirement savings so that you can make informed decisions about your retirement. Sun Life Financial also provides member education, prepares your statements and issues tax receipts.

The Investment Managers are the professionals who do all the of the research needed to set up the funds. From there they basically manage the funds by deciding what stocks or bonds to buy and sell.

There are four key players that have different roles and responsibilities within a company plan.

The first one is your employer who provides the framework of your company�s retirement and savings plan.

An important component to your group plan is employer contributions.

Layfield has a pension committee who select the record keeper to administer your plan. Please inform members who is on the pension committee; Cam Martin; employee representative

Gary Pinkerton; CFO

Derek Bennett; HR Manager

They also select the investment managers and the funds from which you can choose.

And they are responsible for monitoring the plan and provide opportunities for member education.

As the record keeper Sun Life Financial tracks your investments and develops tools you need to be informed about your retirement savings so that you can make informed decisions about your retirement. Sun Life Financial also provides member education, prepares your statements and issues tax receipts.

The Investment Managers are the professionals who do all the of the research needed to set up the funds. From there they basically manage the funds by deciding what stocks or bonds to buy and sell.

10. The amount you can contribute to your RRSP each year is the lesser of 18% of your previous years earnings or for 2007 $19000, minus your Pension Adjustment plus any unused RRSP room from previous years.

The amount you can contribute to your RRSP each year is the lesser of 18% of your previous years earnings or for 2007 $19000, minus your Pension Adjustment plus any unused RRSP room from previous years.

11. reviewreview

12. You are allowed to make lump sum contributions up to your CCRA RRSP limit, but will not receive a matching company contribution.

You choose which funds you want to have in your Group RRSP.

You can make withdrawals on member voluntary contributions only while in service. However, CRA treats a cash withdrawal as earnings for the year in which you made a cash withdrawal. There is a $10 administration fee for each withdrawal.You are allowed to make lump sum contributions up to your CCRA RRSP limit, but will not receive a matching company contribution.

You choose which funds you want to have in your Group RRSP.

You can make withdrawals on member voluntary contributions only while in service. However, CRA treats a cash withdrawal as earnings for the year in which you made a cash withdrawal. There is a $10 administration fee for each withdrawal.

13. You are allowed to make lump sum contributions up to your CCRA RRSP limit, but will not receive a matching company contribution.

You choose which funds you want to have in your Group RRSP.

You can make withdrawals on member voluntary contributions only while in service. However, CRA treats a cash withdrawal as earnings for the year in which you made a cash withdrawal. There is a $10 administration fee for each withdrawal.You are allowed to make lump sum contributions up to your CCRA RRSP limit, but will not receive a matching company contribution.

You choose which funds you want to have in your Group RRSP.

You can make withdrawals on member voluntary contributions only while in service. However, CRA treats a cash withdrawal as earnings for the year in which you made a cash withdrawal. There is a $10 administration fee for each withdrawal.

14. If you�re leaving Overwaitea, you have the options to:

Transfer you assets to a Group Choices plan with Sun Life Financial

Transfer your assets to another financial institution

Transfer your assets to a new employers plan (if permitted), or

Take your assets in cash, less the taxes � however, this is only applicable to RRSP plans only and not your defined contribution pension plan.

If you�re retiring from Overwaitea, you have the options to:

Transfer your Defined contribution pension plan assets to a Life Income Fund otherwise know as a LIF with Sun Life Financial or another financial institution

Transfer your RRSP assets to a Registered Retirement Income Fund otherwise know an a RRIF with Sun Life Financial or another financial institution, or

You can purchase an annuity

If you�re leaving Overwaitea, you have the options to:

Transfer you assets to a Group Choices plan with Sun Life Financial

Transfer your assets to another financial institution

Transfer your assets to a new employers plan (if permitted), or

Take your assets in cash, less the taxes � however, this is only applicable to RRSP plans only and not your defined contribution pension plan.

If you�re retiring from Overwaitea, you have the options to:

Transfer your Defined contribution pension plan assets to a Life Income Fund otherwise know as a LIF with Sun Life Financial or another financial institution

Transfer your RRSP assets to a Registered Retirement Income Fund otherwise know an a RRIF with Sun Life Financial or another financial institution, or

You can purchase an annuity

15. A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

16. A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

17. A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

18. A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

A key benefit of participating in an employer-sponsored group plan is that the investment fees charged are significantly lower than what you would pay as a retail investor.

Low investment management fees matter. You may not think these lower fees make much of a difference, but you�ll be surprised at the impact over the long term. This illustration demonstrates how higher fees can erode the value of your savings over time.

The average management fee on Canadian equity mutual funds is around 2.5%. The investment management fees charged on investment options offered through the Layfield Group RRSP range from .79 % to 1.70% . Complete fee information is available on your account statement as well as on the Sun Life Financial Plan Member services website .

19. You receive many benefits when you participate in the Layfield Group RRSP.

Review the benefits�..

You receive many benefits when you participate in the Layfield Group RRSP.

Review the benefits�..

20. Now we will take a look at the investments offered in the Layfield Group Retirement savings plan.

Now we will take a look at the investments offered in the Layfield Group Retirement savings plan.

21. There are basically 3 steps when it comes to choosing your investments. First you need to understand the different types of investments offered in your plan, the risks associated with each, and the importance of diversification. You also need to find out the type of investor you are .

Once you have done this then you are ready to choose your investments.

You have online access to Morningstar a leading provider in investment news and information. The investment reports you can access through Morningstar provide you with top-rated online investment information and analyses.

When you access Morningstar, you can view capital market performance, individual fund performance, investment style factors, fund and manager updates and much more.

To access Morningstar on the Sun Life Financial Plan Member website, click on Quick Links, click on drop down menu investment info. This will lead you to investment reports and to Morningstar.There are basically 3 steps when it comes to choosing your investments. First you need to understand the different types of investments offered in your plan, the risks associated with each, and the importance of diversification. You also need to find out the type of investor you are .

Once you have done this then you are ready to choose your investments.

You have online access to Morningstar a leading provider in investment news and information. The investment reports you can access through Morningstar provide you with top-rated online investment information and analyses.

When you access Morningstar, you can view capital market performance, individual fund performance, investment style factors, fund and manager updates and much more.

To access Morningstar on the Sun Life Financial Plan Member website, click on Quick Links, click on drop down menu investment info. This will lead you to investment reports and to Morningstar.

22. There are 4 distinct asset categories for investments, each have their own level of risk involved.

Guaranteed funds (or cash equivalents) earn a set rate of interest and give you a guarantee to receive that interest plus the money you invested at the end of a specific term. Guaranteed funds are very low risk. Money Market funds (or cash equivalents) invest primarily in short-term (under one year) government treasury bills and corporate notes. Because they are short-term, they are very low risk and also earn a fairly low rate of return.

Bonds or fixed income funds typically invest in bonds issued by governments and companies. As well as paying a rate of interest, bonds also have a market value which can rise and fall. Bond funds have the potential for higher returns than guaranteed or money market funds increasing the level of investment risk.

Balanced funds invest in a mix of stocks, bonds, and cash investments. The investment manager will adjust the mix as market conditions change, but they usually stay within pre-determined ranges. Balanced funds fluctuate in value and have a higher level of investment risk than bond funds but lower than equity funds. The potential return on balanced funds is higher than that of bonds and lower than that of equity funds.

Equity funds invest in company stock. The investment return on equity funds is determined by increases in the price of the stocks or from dividends paid on these stocks. Because stocks have traditionally outperformed other types of investments, they offer the greatest potential for long-term growth. However, stocks fluctuate more than other types of investments, increasing the level of investment risk. Most stock funds can be subdivided into three caterogies �

domestic (or Canadian stocks), U.S. stocks and International or global stocks.

International investing means you are investing in companies located outside of North America; Europe, Australia and the far East. Global investing includes companies around the world including North America.

There are 4 distinct asset categories for investments, each have their own level of risk involved.

Guaranteed funds (or cash equivalents) earn a set rate of interest and give you a guarantee to receive that interest plus the money you invested at the end of a specific term. Guaranteed funds are very low risk. Money Market funds (or cash equivalents) invest primarily in short-term (under one year) government treasury bills and corporate notes. Because they are short-term, they are very low risk and also earn a fairly low rate of return.

Bonds or fixed income funds typically invest in bonds issued by governments and companies. As well as paying a rate of interest, bonds also have a market value which can rise and fall. Bond funds have the potential for higher returns than guaranteed or money market funds increasing the level of investment risk.

Balanced funds invest in a mix of stocks, bonds, and cash investments. The investment manager will adjust the mix as market conditions change, but they usually stay within pre-determined ranges. Balanced funds fluctuate in value and have a higher level of investment risk than bond funds but lower than equity funds. The potential return on balanced funds is higher than that of bonds and lower than that of equity funds.

Equity funds invest in company stock. The investment return on equity funds is determined by increases in the price of the stocks or from dividends paid on these stocks. Because stocks have traditionally outperformed other types of investments, they offer the greatest potential for long-term growth. However, stocks fluctuate more than other types of investments, increasing the level of investment risk. Most stock funds can be subdivided into three caterogies �

domestic (or Canadian stocks), U.S. stocks and International or global stocks.

International investing means you are investing in companies located outside of North America; Europe, Australia and the far East. Global investing includes companies around the world including North America.

24. Diversifying your investments is one of the best ways to ensure steady growth. Simply put, this means not putting all your eggs in one basket.

Choosing a variety of investments can reduce your risk of loss and increase your potential for higher returns. You can diversify your investments

By Asset Class (for example. money market, bonds, balanced and equities as discussed in the previous slides),

By Manager style � each investment manager adopts a particular style of investing

By investing in foreign markets (such as the U.S. or international markets), and

Different sectors of the economy (for example, investing in manufacturing vs. corporate)

The pension committee looked at the existing fund line up and decided to make the add the new funds to provide you with more diversification; investment manager styles, foreign markets as well as different sectors.

Diversifying your investments is one of the best ways to ensure steady growth. Simply put, this means not putting all your eggs in one basket.

Choosing a variety of investments can reduce your risk of loss and increase your potential for higher returns. You can diversify your investments

By Asset Class (for example. money market, bonds, balanced and equities as discussed in the previous slides),

By Manager style � each investment manager adopts a particular style of investing

By investing in foreign markets (such as the U.S. or international markets), and

Different sectors of the economy (for example, investing in manufacturing vs. corporate)

The pension committee looked at the existing fund line up and decided to make the add the new funds to provide you with more diversification; investment manager styles, foreign markets as well as different sectors.

25. Review slideReview slide

26. Different fund managers choose stocks or bonds according to a particular investment philosophy or style. There are two main styles, active and passive.

An active manager buys and sells securities (stocks or bonds) in the fund with the objective to outperform the index. The securities that an active manager holds in their funds are based on their research of current market conditions and company prospects.

An index manager uses a passive investment style by simply buying and selling assets to match the characteristics of an index (such as the S&P 500 for U.S. equities). An investor that puts their money into a US Equity Index fund for example, is literally going to own a fractional interest in every one of the 500 stocks that make up that index. For this reason, the performance of an index fund should mimic the performance of the index. Because an index manager does not have to do their own research when selecting the stocks or bonds within their fund, index funds have lower management fees than actively managed funds.

Different fund managers choose stocks or bonds according to a particular investment philosophy or style. There are two main styles, active and passive.

An active manager buys and sells securities (stocks or bonds) in the fund with the objective to outperform the index. The securities that an active manager holds in their funds are based on their research of current market conditions and company prospects.

An index manager uses a passive investment style by simply buying and selling assets to match the characteristics of an index (such as the S&P 500 for U.S. equities). An investor that puts their money into a US Equity Index fund for example, is literally going to own a fractional interest in every one of the 500 stocks that make up that index. For this reason, the performance of an index fund should mimic the performance of the index. Because an index manager does not have to do their own research when selecting the stocks or bonds within their fund, index funds have lower management fees than actively managed funds.

29. Dollar cost averaging means investing a certain dollar amount regularly, through up and down periods.

The beauty of this system is that when the stock slumps you're buying more, and when it's pricier you're buying less. It's an especially good way to accumulate units if your budget is limited.

In this example we can see that the difference in the unit price of a fund each time the units are purchased.

At the end of a 12 month period we can calculate our cost by dividing the total investment amount, $3,000 by the total number of units 254.14, which would represent an average cost of $11.80.

To calculate the rate of return you have earned over this period of time, take your gain and divide it by the total investment amount you contributed. In this case, $557.96 divided by $3,000.

Dollar cost averaging means investing a certain dollar amount regularly, through up and down periods.

The beauty of this system is that when the stock slumps you're buying more, and when it's pricier you're buying less. It's an especially good way to accumulate units if your budget is limited.

In this example we can see that the difference in the unit price of a fund each time the units are purchased.

At the end of a 12 month period we can calculate our cost by dividing the total investment amount, $3,000 by the total number of units 254.14, which would represent an average cost of $11.80.

To calculate the rate of return you have earned over this period of time, take your gain and divide it by the total investment amount you contributed. In this case, $557.96 divided by $3,000.

31. In the investment basics section of this presentation, we went over the risks associated with different asset classes and fund types. It�s important to know what level of risk you�re comfortable with prior to choosing your funds.

A great way to determine this is with the Investment risk profiler, found online on the Sun Life Financial Plan Member website. Think of the profiler as a quiz that matches your personality with your money. You�ll have a better understanding of how much risk you�re willing to take when it comes to investing. You�ll also learn the percentage of each asset that you should be investing in.

In the investment basics section of this presentation, we went over the risks associated with different asset classes and fund types. It�s important to know what level of risk you�re comfortable with prior to choosing your funds.

A great way to determine this is with the Investment risk profiler, found online on the Sun Life Financial Plan Member website. Think of the profiler as a quiz that matches your personality with your money. You�ll have a better understanding of how much risk you�re willing to take when it comes to investing. You�ll also learn the percentage of each asset that you should be investing in.

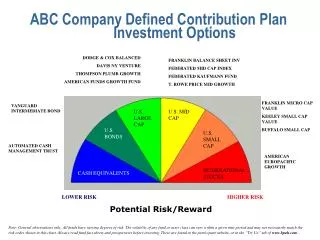

32. This chart provides you with a quick glance at the investment choices available to you under the Layfield Group RRSP. Each fund is categorized by their asset class and risk. The investment with the lowest risk are featured in the top orange bar, while the investments with the higher risk are featured in the bottom of the chart.

some of these funds benefit from a fund manager fee scale - as assets invested with that fund manager increase, the fees decrease.

For more information on the funds available in your plan, you can access Morning star on the Sun Life Financial Plan Member Services website which provides quarterly investment fund pages, detailing past performances, management style and asset mix.

This chart provides you with a quick glance at the investment choices available to you under the Layfield Group RRSP. Each fund is categorized by their asset class and risk. The investment with the lowest risk are featured in the top orange bar, while the investments with the higher risk are featured in the bottom of the chart.

some of these funds benefit from a fund manager fee scale - as assets invested with that fund manager increase, the fees decrease.

For more information on the funds available in your plan, you can access Morning star on the Sun Life Financial Plan Member Services website which provides quarterly investment fund pages, detailing past performances, management style and asset mix.

33. Here is an example of an investor who scored between 36 and 85 points on the investment risk profiler. They are categorized as a moderate investor. From the pie chart above, you can see a recommended mix of investment types and the percentage of your contribution for each. For example, if you were contributing $100 a pay to your plan, out of that $100, 15% ($15) would be directed to International Equity funds, 20% ($20) to Canadian Equities and so on.

You will notice that you have more than one option in most of the categories. For example under Canadian Equities you have 3 choices. If you scored between 36 and 85 points the investment risk profiler suggests you invest 20% in Canadian Equity. You may direct the full 20% to one of the Canadian equity funds or split it between the three fund choices available to you.

It is up to you to learn about the funds offered so that you can make informed decisions.

Here is an example of an investor who scored between 36 and 85 points on the investment risk profiler. They are categorized as a moderate investor. From the pie chart above, you can see a recommended mix of investment types and the percentage of your contribution for each. For example, if you were contributing $100 a pay to your plan, out of that $100, 15% ($15) would be directed to International Equity funds, 20% ($20) to Canadian Equities and so on.

You will notice that you have more than one option in most of the categories. For example under Canadian Equities you have 3 choices. If you scored between 36 and 85 points the investment risk profiler suggests you invest 20% in Canadian Equity. You may direct the full 20% to one of the Canadian equity funds or split it between the three fund choices available to you.

It is up to you to learn about the funds offered so that you can make informed decisions.

34. Discuss rebalancing techniqueDiscuss rebalancing technique

39. Now we will take a look as some helpful tools offered through Sun Life Financial to help you build a strong financial portfolio.

Now we will take a look as some helpful tools offered through Sun Life Financial to help you build a strong financial portfolio.

40. In order to sign into the Sun Life member website you will be required to input your access ID and password. Once you have signed in you will select the link under my financial future which will bring you to my info caf�. My info caf� is seen as your home page where you can access all your plan information and tools. On the left hand side of the screen you have direct links to your online Investment risk profiler, known as the Asset Allocation tool, the Retirement Planner and other financial planning tools. You will also find direct links to your account information from Quick links.

My info caf� features two main sections, my messages and newsstand.

my messages contains important reminders and messages specific to your situation. Ensure that you review any messages within this section each time you visit the website.

In the newsstand you�ll find helpful links to information on retirement and savings topics, including online newsletters, webcasts, your responsibilities and so much more.

Remember you can still access your plan information and tools through the drop-down menus. To access the online tools, go to the Resource Centre drop-down menu and select My Money Tools.

Under my money tools is where you will find the retirement planner��lets now take a closer look at the retirement planner. In order to sign into the Sun Life member website you will be required to input your access ID and password. Once you have signed in you will select the link under my financial future which will bring you to my info caf�. My info caf� is seen as your home page where you can access all your plan information and tools. On the left hand side of the screen you have direct links to your online Investment risk profiler, known as the Asset Allocation tool, the Retirement Planner and other financial planning tools. You will also find direct links to your account information from Quick links.

My info caf� features two main sections, my messages and newsstand.

my messages contains important reminders and messages specific to your situation. Ensure that you review any messages within this section each time you visit the website.

In the newsstand you�ll find helpful links to information on retirement and savings topics, including online newsletters, webcasts, your responsibilities and so much more.

Remember you can still access your plan information and tools through the drop-down menus. To access the online tools, go to the Resource Centre drop-down menu and select My Money Tools.

Under my money tools is where you will find the retirement planner��lets now take a closer look at the retirement planner.

41. You will first be asked to complete the �my information� screen. Some of the information on this screen will be pre-populated with information you provided to Sun Life Financial when you enrolled in the Plans.

To learn more about the sections on this first screen, just select the question mark beside each heading.

You will first be asked to complete the �my information� screen. Some of the information on this screen will be pre-populated with information you provided to Sun Life Financial when you enrolled in the Plans.

To learn more about the sections on this first screen, just select the question mark beside each heading.

42. Once you�ve determined your retirement lifestyle, you�ll be presented with an Action plan.

Think of your action plan as your retirement blueprint. Your action plan takes into account the number of years to retirement, your income, your investments and savings, your desired risk tolerance and your lifestyle goals.

In the example show here, the Action Plan informs the member that their desired retirement lifestyle is currently out of reach. Meaning, with the savings they currently have, they will not have enough money to live their desired retirement lifestyle.

Don�t get discouraged. This is why it�s called an action plan. Recommendations are provided on some possible changes you could implement to help you reach your retirement goals.

In this next example, the graph compares your estimated assets at retirement to the assets you will require to live your desired retirement lifestyle. The amounts are displayed in future dollars, meaning inflation has been calculated into the examples shown here.

The red area within this graph represents the gap between what you should have and what you will have based on your current information.

On this next screen, you see your current monthly savings, then what your project monthly savings should be to achieve your desired lifestyle and finally the additional savings you require to save each month to meet your retirement lifestyle.

This last screen shot shows how you can adjust some of your information and recalculate for other scenarios to create an alternate action plan.

As your financial situation may change, or your retirement priorities may change, it�s always a good idea to revisit your action plan periodically to ensure you�re on track or to update it with new information which may alter your action plan.

Once you�ve determined your retirement lifestyle, you�ll be presented with an Action plan.

Think of your action plan as your retirement blueprint. Your action plan takes into account the number of years to retirement, your income, your investments and savings, your desired risk tolerance and your lifestyle goals.

In the example show here, the Action Plan informs the member that their desired retirement lifestyle is currently out of reach. Meaning, with the savings they currently have, they will not have enough money to live their desired retirement lifestyle.

Don�t get discouraged. This is why it�s called an action plan. Recommendations are provided on some possible changes you could implement to help you reach your retirement goals.

In this next example, the graph compares your estimated assets at retirement to the assets you will require to live your desired retirement lifestyle. The amounts are displayed in future dollars, meaning inflation has been calculated into the examples shown here.

The red area within this graph represents the gap between what you should have and what you will have based on your current information.

On this next screen, you see your current monthly savings, then what your project monthly savings should be to achieve your desired lifestyle and finally the additional savings you require to save each month to meet your retirement lifestyle.

This last screen shot shows how you can adjust some of your information and recalculate for other scenarios to create an alternate action plan.

As your financial situation may change, or your retirement priorities may change, it�s always a good idea to revisit your action plan periodically to ensure you�re on track or to update it with new information which may alter your action plan.

43. We will now look at ways you can manage your account on a day to day basis

We will now look at ways you can manage your account on a day to day basis

44. You have access to your semi-annual statements online

Your statement is a good current snap shot of how your investments have been performing.

Full fee disclosure can also be viewed on the statements.

You have access to your semi-annual statements online

Your statement is a good current snap shot of how your investments have been performing.

Full fee disclosure can also be viewed on the statements.

45. All the information you need is only a click away. You�ll find our member site at www.sunlife.ca/member easy to navigate.

To access your account, you will need a personal access ID and password. You will receive information to register for these numbers when you first join your plan.

The website is used for 3 purposes:

Informational � account balances, statements, fee�s, etc

Transactional � transfer between funds, update investment instructions,

Educational � Morningstar, tools

All the information you need is only a click away. You�ll find our member site at www.sunlife.ca/member easy to navigate.

To access your account, you will need a personal access ID and password. You will receive information to register for these numbers when you first join your plan.

The website is used for 3 purposes:

Informational � account balances, statements, fee�s, etc

Transactional � transfer between funds, update investment instructions,

Educational � Morningstar, tools

46. By calling our 1-866 number you can access our automated telephone system 24 hours a day seven days a weeek or talk to one of our customer care centre representatives every business day from 8 am to 8 pm est.

When you call the customer care centre you will be asked to provide your Access ID and password. You will then have a choice to use the automated service or speak directly to one of Sun Life�s customer care representatives. They they will know what plan you belong to and what investment options you have available. They can provide you with information or guidance, but they are not licensed to provide advice.

�

By calling our 1-866 number you can access our automated telephone system 24 hours a day seven days a weeek or talk to one of our customer care centre representatives every business day from 8 am to 8 pm est.

When you call the customer care centre you will be asked to provide your Access ID and password. You will then have a choice to use the automated service or speak directly to one of Sun Life�s customer care representatives. They they will know what plan you belong to and what investment options you have available. They can provide you with information or guidance, but they are not licensed to provide advice.

�

47. Morningstar is a leading provider in investment news and information. The investment reports you can access through Morningstar provides you with top-rated online investment information and analyses. Tracking the performance of your plan�s investment funds have never been so easy and comprehensive.

On the plan member website, you have access to Morningstar, where you can view capital market performance, individual fund performance, investment style factors, fund and manager updates and much more under investment information.

Through the Portfolio X-ray you can analyze different combinations of funds as a single portfolio, including the effect of asset allocation and fund changes to your portfolio.

Get to know Morningstar. You can link directly to Morningstar by selecting the Investment Reports links from the Quick Links section of my info caf�, or by going to the Accounts drop-down menu and selecting Investment Reports. Select the Morningstar link or logo to access the investment information. Morningstar is a leading provider in investment news and information. The investment reports you can access through Morningstar provides you with top-rated online investment information and analyses. Tracking the performance of your plan�s investment funds have never been so easy and comprehensive.

On the plan member website, you have access to Morningstar, where you can view capital market performance, individual fund performance, investment style factors, fund and manager updates and much more under investment information.

Through the Portfolio X-ray you can analyze different combinations of funds as a single portfolio, including the effect of asset allocation and fund changes to your portfolio.

Get to know Morningstar. You can link directly to Morningstar by selecting the Investment Reports links from the Quick Links section of my info caf�, or by going to the Accounts drop-down menu and selecting Investment Reports. Select the Morningstar link or logo to access the investment information.

48. Other financial tools you may find helpful can be found in the Financial Planning tools link directly from my info caf� or by going to the Resource Centre Drop-down menu and selecting Tools from the My Money Tools link.

Featured here are just a few:

Withdrawal calculator shows you the current and future impact of withdrawals from your RRSP. Remember withholding taxes may be withheld.

Mortgage vs. RRSP calculator helps you decide whether it�s more advantageous to contribute to an RRSP or pay down your mortgage.

RRSP loan calculator allows you to determine if it�s in your best interest to take out a loan to make a lump sum contribution to your RRSP.

Capital gains vs. RRSP tax comparison calculator helps you determine whether you�d be better off investing inside or outside of your RRSP.

Other financial tools you may find helpful can be found in the Financial Planning tools link directly from my info caf� or by going to the Resource Centre Drop-down menu and selecting Tools from the My Money Tools link.

Featured here are just a few:

Withdrawal calculator shows you the current and future impact of withdrawals from your RRSP. Remember withholding taxes may be withheld.

Mortgage vs. RRSP calculator helps you decide whether it�s more advantageous to contribute to an RRSP or pay down your mortgage.

RRSP loan calculator allows you to determine if it�s in your best interest to take out a loan to make a lump sum contribution to your RRSP.

Capital gains vs. RRSP tax comparison calculator helps you determine whether you�d be better off investing inside or outside of your RRSP.

49. Besides the Retirement Planner, there are also some other supplementary retirement planning tools available online.

Annuity premium calculator allows you to estimate the premium (or amount) you require to provide a specified level of income, as well as estimate the monthly income that a specified lump sum will provide.

Old age security (OAS) clawback calculator explains �clawback� and provides you with an estimate as to your monthly OAS payments.

Retirement income fund (RRIF) calculator shows how much you can withdraw each year from your RRIF, and estimates how long your retirement income will last.

Besides the Retirement Planner, there are also some other supplementary retirement planning tools available online.

Annuity premium calculator allows you to estimate the premium (or amount) you require to provide a specified level of income, as well as estimate the monthly income that a specified lump sum will provide.

Old age security (OAS) clawback calculator explains �clawback� and provides you with an estimate as to your monthly OAS payments.

Retirement income fund (RRIF) calculator shows how much you can withdraw each year from your RRIF, and estimates how long your retirement income will last.

50. Review slideReview slide

51. Questions and thank plan members for coming out and participating

Questions and thank plan members for coming out and participating