Download

1 / 42

420 likes | 573 Views

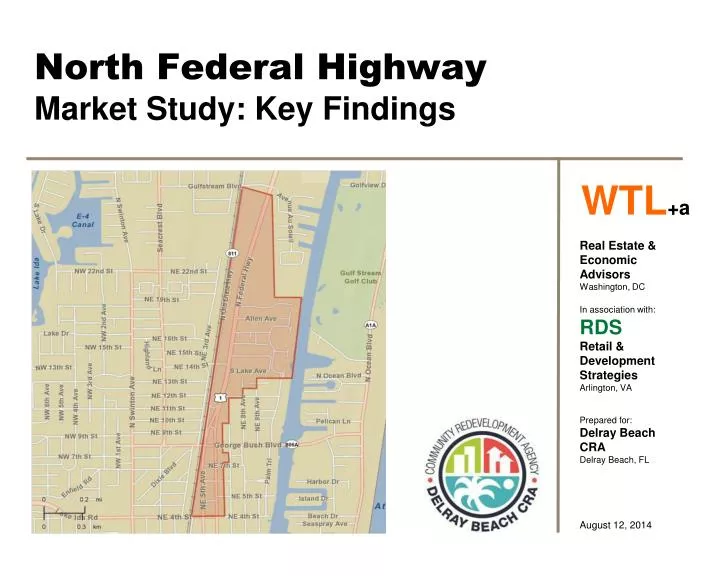

North Federal Highway Market Study: Key Findings. WTL +a. Real Estate & Economic Advisors Washington, DC In association with: RDS Retail & Development Strategies Arlington, VA Prepared for: Delray Beach CRA Delray Beach, FL August 12, 2014. Objectives of the Market Study.

E N D

North Federal HighwayMarket Study: Key Findings WTL+a Real Estate & Economic Advisors Washington, DC In association with: RDS Retail & Development Strategies Arlington, VA Prepared for: Delray Beach CRA Delray Beach, FL August 12, 2014

Objectives of the Market Study • Update 1999 market study of revitalization & redevelopment potentials • Analyze demographic & economic characteristics • Evaluate real estate market trends & conditions • Measure real estate market potentials, estimate absorption/phasing for key uses: • Residential • Speculative/multi-tenant office • Lodging/hotel • Retail & food service • Guide public decisions about zoning, additional infrastructure & other public improvements along the corridor

Study Area Context Study Area

Study Area Land Uses • 206 acres • 46+/- acres & 375,000 SF of “workplace” uses: • 153,300 SF retail (41%) • 126,000 SF auto-related (34%) • 38,400 SF warehouse (10%) • 30,100 SF demolished (8%) • 18,200 SF restaurants/food service (5%) • 8,800 SF office (2%) • 5.6 vacant acres in demolished uses (excludes Swap Shop site) • 515 housing units • 47% owner-occupied • 34% renter-occupied • 19% “unoccupied” • Traffic volumes in 2013 averaged 26,600 vehicles per day

Proposed Development Projects • Beachway Motel: 13 rooms • St. George site: • 38 townhouses • Mid-2015 delivery • Southgate Motel: 29 rooms • Goodwill of Delray: 1,518 SF addition • Delray Preserve: • 188 proposed MF units (22 units/acre) • Borton Volvo: 17,226 SF auto-related • 2645 North Federal: • 11,311 SF professional & medical office space • Gulfstream Villas: 15 townhouse units

Key Market FindingsDemographics (2000-2013) • Very strong population growth in Palm Beach County: 1.3 million residents • Population increased by 214,500 in 72,700 new HHs • Delray Beach: 61,800 residents • Added 1,780 residents = 820 HHs • Limited growth next 5 years: 855 residents in <300 HHs • Since 2000, Boca, Boynton & West Palm growing significantly faster than Delray (9,700 to 21,000 new residents) • Study area’s population stable; new housing will add new residents • Compared to City, the study area: • More affluent (annual HH incomes of $79,600 vs. $66,600) • Spend more on retail ($20,700 vs. $17,500) • Spend more on Food & Beverage ($6,700 vs. $5,700) • Has fewer unoccupied & vacant housing units

Key Market FindingsEconomic Profile • 619,000 jobs in Palm Beach County • Economy in recovery from 2007—2009 recession (49,500 jobs lost) • 20,200 new jobs created past 3 years • Strongest job growth in Professional Services, Health Care; mirrors national trends • Delray Beach contains 34,700 jobs: 6% of County • Jobs-to-population ratio: 0.58 • 45% of jobs in Services; 27% in Retail • 19% of all jobs in Retail sector are in restaurants

Key Market FindingsEconomic Profile • Job growth is a critical barometer of demand for ‘workplace’ real estate: commercial office, retail, industrial parks, etc. • State forecasts: 83,700 new jobs in Palm Beach County (2013 – 2021) • 5,000 new jobs in Delray if City maintains its current share • Citywide HH retail spending (demand) vs. retailer sales (supply): • $489 million vs. $523 million • Reflects in-flow of visitors to Delray, strength of downtown • Can HH sales (“opportunity gap”) in specific categories be recaptured?

Key Market FindingsHousing Market Performance • Delray Beach housing inventory: • 34,100 units (38% single-family; 52% multi-family) • 8,200+ unoccupied units reflects heavy seasonal occupancy • “True Vacancy” (i.e., empty & available) is low: 6.5%, suggesting stabilized occupancies • Median value: $141,000 (study area: $224,200) • Annual housing starts (2005-2013): • Palm Beach County: 4,800 units per year(62% single-family) • Delray Beach: 255 units per year (61% multi-family) • Confirms market-response to moderate-density product such as stacked-flats • Multi-family rental trends: • Higher rents achieved in Delray than Boynton ($1.57 PSF vs. $1.07 PSF) • Higher vacancy rates in Delray than Boynton (9.8% vs. 3.9%) • All comparables defined by industry as “Class A” quality

Key Market FindingsOffice & Retail Market Performance • Delray Beach office inventory (2006-2013): • 2.9 million SF in 301 buildings; comprises mix of “garden” buildings & industry-standard suburban office parks • Accounts for 12% of County’s 24 million SF inventory • Overall vacancies have jumped since 2006: from 8% to 26.5% • Significant challenges of negative absorption (leasing): (677,000) SF vacated since 2006 • Office Depot HQs relocation to Boca responsible for weakened market statistics • Job growth in office-using sectors is critical • Delray Beach retail inventory (2013): • 3.9 million SF in multiple property types • Accounts for 9% of County’s 44.4 million SF inventory • 239,000 SF of net absorption in 2013 • Strengthening regional role as retail destination • $35 million in recaptured Grocery spending: Trader Joe’s (10,000 SF) & Fresh Market (20,000 SF)

Key Market FindingsHotel Market Performance • Delray Beach hotel supply: • 887 rooms in 7 properties (as defined by STR): comprises 6.5% share of County’s 13,600+ rooms • Inventory includes 95-room Fairfield Inn under construction • Since 2010, annual occupancies have fluctuated between 58% & 70% • 4-year average occupancies: 64.9%, suggests roomnight demand is at threshold for financing new construction (65% to 72%) • Colony Hotel & Crane’s Beach Hotel do not report performance to STR • Solid annual growth in average daily rates (ADRs): $127 (2010) to $145 (2014)

What We HeardStakeholder Interviews • Study area lacks identity/brand; does not benefit from economic engine & strong identity of downtown • Land uses characteristic of aging, low-density suburban commercial corridors in south Florida • In transition: • Land values increasing due to proximity to downtown • Private investment in high-quality residential • Difficult to attract commercial re-investment at current low rents • Values driven by perceived future uses • ‘Hot button’ issues: increasing residential densities; introduction of rental housing (turnover) • Largest contiguous parcels are all auto-oriented uses • How to capture spending from high-income HHs (e.g., Gulf Stream)

What We HeardStakeholder Interviews • Desire for independent, “boutique” retail in walkable district • Narrow lot depths, fragmented ownership/parcel assemblage, adjacent rail line complicate development • Challenges of current densities/zoning: • Will not support significant retail • Precludes ‘Pineapple Grove-type’ development (i.e., surface parking required) • Costs of structured parking too high w/o additional revenues • Is there opportunity to ‘cluster’ new retail (e.g., at George Bush Blvd.)? • How can public improvements & other public policies be used to: • Enhance marketability • Generate private commercial investment • Create pedestrian-friendly areas?

Key Market FindingsMarket Directions Retail & Food Service • Success of Atlantic Avenue has created strong regional destination & identity • Challenges of maintaining specialty retail in a strong food & beverage market, higher rents • Study area retail potentials: • Affected by distance & quality of pedestrian space • Width of North Federal Highway limits easy creation of walkable retail environment • Limited residential densities cannot support walkable retail cluster on its own • Significant competitive environment & higher densities in Boynton Beach • Transitional uses characteristic of South Florida commercial strips • Several buildings worthy of preservation & re-use; “character-giving”

Key Market FindingsMarket Directions • Market-rate Housing • Forecasts suggest limited near-term population & HH growth • Near-term demand likely captured by planned projects (e.g., ZOM) • Transitional land uses in study area suggest opportunities for moderate-density infill residential development & selected mixed-use • Parcel size, ownership priorities & consolidation potential affect opportunities for multi-family housing • Increased residential densities will be critical to support new retail in study area: • Each new resident = 4 to 7 SF • Each new office worker = 2 to 5 SF • Each visitor = 0.5 to 1.5 SF

Key Market FindingsMarket Directions • Professional Office/Business Services • State (DEO) employment forecasts suggest near-term growth: • Retail/Food Service • Professional Services & Finance/Insurance & Real Estate • Job growth in office-using sectors critical to generating near-term demand • If 2,000 of 5,000 new jobs are office-using = 400,000 SF • Current office vacancies = 793,000 SF • Current zoning in most of Delray Beach (& study area) restricts higher-density office development • Suggests small-scale “garden” product & tenant mix • Limited market potentials in the near-term (3 to 5 years)

Key Market FindingsMarket Directions Hotel/Lodging • Sustained annual occupancies meet threshold required by capital markets for financing new construction (65% to 72%) • Fairfield Inn may delay near-term feasibility of new hotel in study area • Key planning question: • Where is best location for future hotel product in Delray Beach? • Locational characteristics that enhance marketability (e.g., Hyatt Place, Fairfield) • Future feasibility studies will be required to warrant conventional financing & determine product type (i.e., business vs. leisure)

Next Steps • Solicit public feedback tonight & continue stakeholder outreach • Estimate potential market demand by use & range (e.g., low/high) • Suggest potential phasing & development strategies • Consider linkages to downtown (e.g., branding/marketing, land uses) • Consider both natural market growth & “induced” markets • Prepare draft Market Study report by 9/15 for CRA review • Submit final Market Study report by 9/30

Demographic/Economic ProfileSelected Municipalities in Palm Beach County

Demographic & Economic ProfileAnnual Household Spending, 2012

Demographic & Economic ProfileCounty Employment Trends, 1995-2014

Demographic & Economic ProfileCounty Employment Forecasts, 2010-2020

Demographic & Economic ProfileCounty Employment Forecasts, 2010-2020

Demographic & Economic ProfileCity of Delray Beach Businesses & Employment, 2012

Demographic & Economic ProfileCity of Delray Beach Businesses & Employment, 2012

Demographic & Economic ProfileCity of Delray Beach: Retail “Recapture” Opportunities

Demographic & Economic ProfileCity of Delray Beach: Retail “Recapture” Opportunities

Real Estate Market Conditions Housing Profile

Real Estate Market Conditions Housing Profile

Real Estate Market Conditions Housing Starts, 2004-2013

Real Estate Market Conditions Market Performance of Selected MF Complexes

Real Estate Market Conditions Market Performance of Selected MF Complexes

Real Estate Market Conditions All Workplace Uses, 2014

Real Estate Market Conditions Office Market Performance, 2006-2014

Real Estate Market Conditions Retail Market Performance, 2006-2014