Download

1 / 18

200 likes | 522 Views

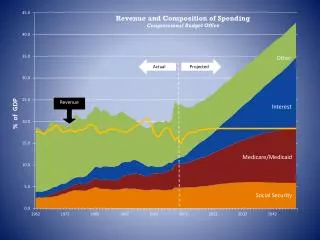

Revenue Assignment. Strengthening Fiscal Framework for Local Government Reform FDI Workshop, January 21, 2003 Gábor Péteri, OSI / LGI. Public functions. Economic stability Income redistribution Resource allocation: providing and financing public services. Principles of revenue assignment.

E N D

Revenue Assignment Strengthening Fiscal Framework for Local Government Reform FDI Workshop, January 21, 2003Gábor Péteri, OSI/LGI

Public functions • Economic stability • Income redistribution • Resource allocation: providing and financing public services

Principlesof revenue assignment • Significant (broad, buoyant) • Stability • Predictability • Accountability • No tax exporting • Political culture

Methods of tax assignment • Local tax: base, rate, administration • Surcharges: local rate setting joint base and administration 3. Sharing: formula-driven predictable local discretion indirect local influence

Local taxes in % of GDP Federal states Unitary countries Income, profit tax 4.5 3.3 Wage tax 0.3 - Property tax 1.8 0.9 Consumption tax 1.5 0.2 Sales tax 0.7 0.1 Other 0.8 0.4 Total 9.6 4.9 Source: OECD Revenue Statistics, 1965-1996, OECD, 1997

Criteria for tax assignment Corporate income tax: ·Exporting tax burden ·Cyclical changes ·High administrative costs Personal income tax: ·Benefit principle ·No income redistribution (flat rate) ·Centralized administration Workplace/residence

Criteria for tax assignment (2) Value added tax: Small number of companies Border adjustment Protectionism Sharing formula (+) Excise tax: Motor vehicle: progressive, connected to local expenditures Alcohol, tobacco

Criteria for tax assignment (3) Property tax: Immobile tax base Ad valorem: progressive Tax administration is expensive Traditions Natural resources: Unequal access Unstable Political separatism

Local shares of taxes: countries focused on income and profit Country Income & Profits Property Sweden 99.6 Finland 95.2 4.7 Denmark 92.1 7.8 Norway 87.9 8.8 Switzerland 86.9 12.7 Germany 81.8 17.8 Belgium 72.6 EU average 59.9 35.1

Local shares of taxes: countries focused on property Country Income & Profits Property United States 75.4 United Kingdom 76.7 Canada 5.7 85.1 New Zealand 92.9 Australia 99.5

User charges • Local political decision (non-budget) • Beneficiary can be identified • Full cost pricing • Social consequences

Borrowing, debt financing • Underutilized • Control over local borrowing (level, bankruptcy procedure) • Repayment: revenue making investments general taxes

Transfers and grants Objectives: 1. vertical equalization 2. horizontal equalization Types of grants: 1. Current and capital 2. Specific/Conditional grants 3. General purpose 4. Matching

Methods of grant allocation 1. Control on expenditures and revenues Decision on appropriations (Eiestimate) Individual revenue assessment (Riplanned) Negotiation and bargaining on transfers (Ti = Eiestimate -Riplanned)

Methods of grant allocation (2) 2. Control over the transfers Local authority to generate revenues (R) Normative grants (Gnormative) Autonomous decision on expenditure levels (E=R+ Gnormative)

Methods of grant allocation (3) 3. Expenditure and revenue capacity based Accepted expenditure levels (Estadardized) Required revenues(Rrequired) Calculated grant: (Gcalculated=Eaccepted-Rrequired)