Download

1 / 26

260 likes | 629 Views

Bank Regulators’ Standards for Commercial Real Estate Workouts. The Counselors of Real Estate 2010 Midyear Meetings. Bank Failure Stats:. In 2005 and 2006, there were no bank failures. In 2007, there were 3 bank failures. In 2008, there were 25 bank failures.

E N D

Bank Regulators’ Standards for Commercial Real Estate Workouts The Counselors of Real Estate2010 Midyear Meetings

Bank Failure Stats: • In 2005 and 2006, there were no bank failures. • In 2007, there were 3 bank failures. • In 2008, there were 25 bank failures. • In 2009, there were 140 bank failures. • Thru May 21, 2010, there have been 72 bank failures. FDIC Failed Bank List, http://www.fdic.gov/bank/individual/failed/banklist.html

Questions to ask about your bank • What’s required for my workout under the Banking Regulators’ October 2009 CRE Policy Statement on Prudent CRE Workouts? • Has shrinkage of my bank’s capital caused problems under the Banking Regulators’ 2006 Guidance on CRE Loan Concentrations as a percentage of capital? • Has my bank fallen below the “well capitalized” level and lost its ability to fund CRE loans with brokered and high-rate deposits? • Has my bank fallen below the “adequately capitalized” level, or otherwise offended the FDIC, so the bank is subject to a cease and desist order requiring changes in CRE lending procedures?

First Question: What’s required for my workout under the Banking Regulators’ October 2009 CRE Policy Statement on Prudent CRE Workouts?

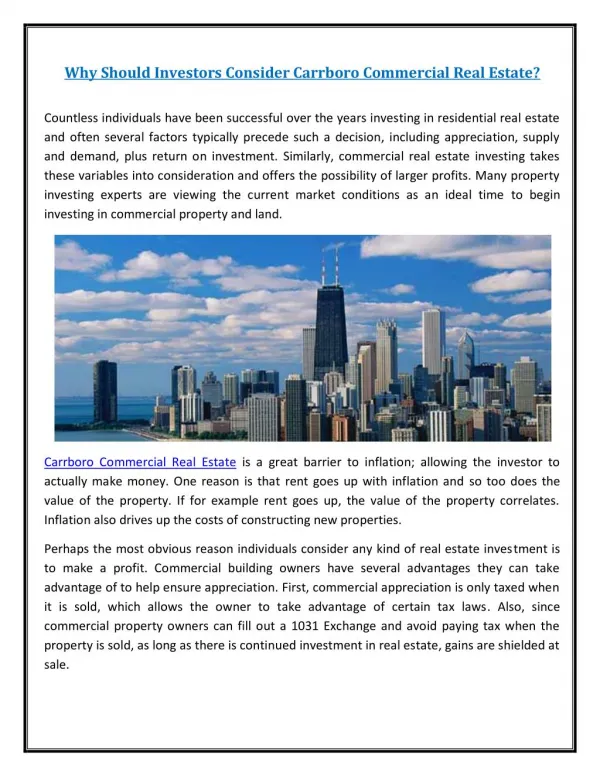

Regulators CRE Workout Guidance (Oct. 2009) • Encourages workouts with “creditworthy customers who have the willingness and capacity to repay their debts.” • Workout needs to be based on “a comprehensive review of a borrower’s financial condition.” • Renewed or restructured loans to borrowers “who have the ability to repay their debts according to reasonable modified terms will not be subject to adverse classification solely because the value of the underlying collateral has declined to an amount that is less than the loan balance.” [quoting fromPolicy Statement on Prudent Commercial Real Estate Loan Workouts (Oct. 30, 2009)[http://www.fdic.gov/news/news/financial/2009/fil09061a1.pdf]

Regulators CRE Workout Guidance (Oct. 2009) re Collateral • Probability of payment by borrower is more important than value of collateral in determining loan classification and whether examiners will criticize the loan. • Bank needs evidence that the borrower can pay both principal and interest under the terms of the restructured loan. • Decline in collateral value does not, by itself, require adverse classification. • If loan terms are unreasonable in view of borrower’s financial weakness, then a decline in collateral value is likely to result in adverse classification of the loan. [quoting fromPolicy Statement on Prudent Commercial Real Estate Loan Workouts (Oct. 30, 2009)[http://www.fdic.gov/news/news/financial/2009/fil09061a1.pdf]

Policy Requires Review of All Sources of Payment Institutions should consider loan workouts after: • “analyzing a borrower’s repayment capacity” • “evaluating the support provided by guarantors,” and • “assessing the value of the collateral pledged on the debt.” “Loan workout arrangements need to be designed to help ensure that the institution maximizes its recovery potential.” • Note: Bank must not make life too easy for the borrower.

Regulators require banks to face the truth about their loans For a troubled CRE loan, bank must develop an individual workout plan that: • “analyzes the current financial information on the borrower or guarantor” • “supports the ultimate collection of principal and interest” • includes “[u]pdated and comprehensive financial information on the borrower, real estate project, and any guarantor” • Includes “[c]urrent valuations of the collateral supporting the loan and the workout plan” • Includes “[a]nalysis and determination of appropriate loan structure (e.g., term and amortization schedule), curtailment, covenants, or re-margining requirements” • “[a]ppropriate legal documentation for any changes to loan terms” Policy p. 3 • If loan is restructured, the goal is to make it a safe and sound loan. • If loan is too weak to salvage, then bank must focus on collateral.

Collateral Value Is Critical If Loan Performance is Poor The Regulators’ New CRE Workout Guidance says: • “As the primary sources of loan repayment decline, the importance of the collateral’s value as a secondary repayment source increases.” • “The institution is responsible for reviewing current collateral valuations” • Requires review of latest “appraisal or evaluation” -- Doesn’t always require new appraisal • Purpose of review is “to ensure that their assumptions and conclusions are reasonable.” • Remember: Regulators want banks to face the truth about their loans. • Need “policies and procedures that dictate when collateral valuations should be updated” -- • “as part of its ongoing credit review,” • “as market conditions change,” or • “as borrower’s financial condition deteriorates.”

Goal of CRE Guidance: Prudent Loans • A safe and sound loan, from a regulator’s perspective, is a loan that has a high probability of being repaid according to its terms. • That’s why the regulators emphasize the necessity for evidence that the borrower can pay both principal and interest under the terms of the restructured loan. • Regulators don’t want loan terms that are unreasonable in light of the borrower’s financial weakness because then collateral value will be the controlling factor. • If the borrower is weak, then a safe and sound loan may need to be smaller than the old loan.

Regulators suggest two-note restructuring: • One note (the “A Note”) is for a reduced principal amount • LTV ratio set to fit most recent appraisal or value update of collateral • Payment terms realistic according to debtor's ability to service the debt • Goal is to produce smaller loan that can be returned to accrual status • Accrual status requires six consecutive months of payment • Regulators allow consideration of payments made prior to restructuring • Other note (the “B Note”) is for the rest of the balance due • Accounting principles will require the write-off of the B Note • Bank retains legal right to enforce the B Note • B Note might be “shared appreciation mortgage” • Instead of interest, the bank gets share of gain on sale • obligation to repay principal can’t be condition the on property appreciation

Second Question: Has shrinkage of my bank’s capital caused problems under the Banking Regulators’ 2006 Guidance on CRE Loan Concentrations as a percentage of capital?

Regulators got concerned in 2006 about CRE concentrations: • Any bank that is approaching or exceeds the following supervisory criteria may be identified for further supervisory analysis: • “total reported loans for construction, land development, and other land represent 100 percent or more of the institution’s total capital”; or • “total CRE loans, as defined in the interagency guidance, represent 300 percent or more of the institution’s total capital, and the outstanding balance of the institution’s CRE loan portfolio has increased by 50 percent or more during the prior 36 months.” Source: Commercial Real Estate Lending Joint Guidance (December 12, 2006) (emphasis added)posted at http://www.fdic.gov/regulations/laws/federal/2006/06notice1212.html) Question: Has your bank already exceeded these limits?

Boosting Loan Loss Reserves Reduces Capital • Allowance for Loan and Lease Losses (“ALLL”) > 1.25 percent of Risk-weighted Assets Is Not Included in Regulatory Capital. • If Loan Loss Provisions Can’t Be Funded From Current Earnings, then Increases In Reserves Are Deducted from Capital. • Setting up a Special Loan Loss Reserve Will Reduce Capital. • Writing Loan Down or Off When Restructuring Will Reduce Capital. • Of Course, Recent Negative Earnings Have Reduced Capital.

Making CRE Loans > Limits May Be Burdensome Or Impossible If concentration is > 100% or 300% threshold, FDIC says that, at a minimum, loan officers must: • “provide comprehensive credit memos/write-ups to the loan committee during the approval process that identify exceptions to the loan policy” • “explain why the exceptions are necessary and how the exposure is mitigated” Source: FDIC College CBT - Asset Quality (posted at www.fdic.gov/regulations/resources/directors_college/sfcb/asset/instruction.html) • Question: Is your CRE loan application an exception? Now, some bank examiners are treating the 2006 supervisory thresholds as ceilings on maximum CRE loan concentration. • Question: Can your bank make any new CRE loans?

Third Question: Has my bank fallen below the “well capitalized” level and lost its ability to fund CRE loans with brokered and high-rate deposits?

Rigid Capital Standards Control Bank Funding • Some banks financed condo loans with brokered or high-rate deposits. • Brokered deposits are funds from out-of-market customers placed by brokers. • High-rate deposits pay interest 75 basis points more than the local market rate or benchmark national rate for a deposit of similar maturity. • If a bank stops being “well capitalized,” then it needs FDIC waiver to renew brokered or high-rate deposits. • The FDIC hasn’t been granting waivers. • If a bank stops being “adequately capitalized,” then even the FDIC can’t grant a waiver to renew brokered or high-rate deposits.

If It’s Not “Well Capitalized,” aBank Needs Capital and Cash • Bank hopes to minimize ALLL growth but satisfy GAAP. • Bank hopes to minimize write-downs but satisfy GAAP. • Bank needs cash to pay off maturing brokered and high rate deposits. • Bank can’t borrow from FHL Bank without good collateral. • Bank can’t get funds by paying interest greater than FDIC cap • Bank needs collect cash on loans, or to sell loans at gain

Non-Capital Problems Also Provoke Examiners to Restrict Lending: • Revise the Loan Policy to require more stringent credit practices and loan documentation standards • Revise the Loan Policy to provide more guidance over commercial real estate and construction lending • Revise the Loan Policy to establish more prudent limits for concentrations in CRE and require more rigid monitoring and reporting processes for concentrations [Source: FDIC College CBT - Exam Discussion Points - Asset Quality (posted at: http://www.fdic.gov/regulations/resources/directors_college/sfcb/asset/discussion.html) • Your Loan Officer Worries: How can I get an extension/workout through the new underwriting requirements that the regulators made us adopt?

Fourth Question: Has my bank fallen below the “adequately capitalized” level, or otherwise offended the FDIC, so the bank is subject to a cease and desist order requiring changes in CRE lending procedures?

FDIC May Have Ordered Bank to Raise Capital and Collect Loans [C]ease and desist from ... unsafe or unsound banking practices ... [including]: • operating with an inadequate level of capital • failure to establish and enforce adequate loan repayment programs • failure to obtain current and complete financial information [S]ubmit a written plan for increasing the capital ratio ... by the following [acts]: (i) the sale of common stock and non-cumulative perpetual preferred stock; (ii) the elimination of all or part of the assets classified "Loss" as of [last exam date], without incurring loss or liability to the Bank, provided any such collection on a partially charged-off asset shall first be applied to that portion of the asset which was not charged off pursuant to this ORDER; (iii) the collection in cash of assets previously charged off; or (iv) the direct contribution of cash by [directors and/or shareholders]. Source: In the Matter of Purdum State Bank, Purdum, Nebraska, Docket No. 02-066b (6-28-02) (emphasis added) . (posted at http://www.fdic.gov/bank/individual/enforcement/11946.html#HN1)

FDIC Probably Ordered Bank to Reduce Risk of Bad Loans • “[T]he bank shall . . . submit … a written planto reduce the Bank's risk position in each asset in excess of $1,000,000 which is classified ‘Substandard’ or ‘Doubtful’" • (i) Review the financial position of each such borrower, including source of repayment, repayment ability, and alternative repayment sources; and • (ii) Evaluate the available collateral for each such credit, including possible actions to improve the Bank's collateral position. • "reduce" means to: (1) collect; (2) charge off; or (3) improve the quality of such assets so as to warrant removal of any adverse classification Source: In the Matter of Marine Bank, Wauwatosa, Wisconsin, Docket No. 04-085b (5-19-04) (emphasis added). posted at http://www.fdic.gov/bank/individual/enforcement/12213.html#HN1

Classifying Troubled loans: "Substandard," "Doubtful," or "Loss.” “A Substandard Asset is inadequately protected by the current sound worth and paying capacity of the obligor or of the collateral pledged, if any. Assets so classified must have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt.” “An asset classified Doubtful has all the weaknesses inherent in one classified Substandard with the added characteristic that the weaknesses make collection or liquidation in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable.” “Assets classified Loss are considered uncollectible and of such little value that their continuance as bankable assets is not warranted. This classification does not mean that the asset has absolutely no recovery or salvage value, but rather it is not practical or desirable to defer writing off this basically worthless asset even though partial recovery may be effected in the future. Amounts classified Loss should be promptly charged off.” [Source: Uniform Agreement on the Classification of Assets and Appraisal of Securities Held by Banks and Thrifts ” (posted at: http://www.fdic.gov/news/news/financial/2004/fil7004a.html)

FDIC Orders Restrict New Loans to Delinquent Borrower • “[T]he Bank shall not extend ... any additional credit to, or for the benefit of, any borrower whose loan or other credit has been classified "Substandard", "Doubtful" or is listed for "Special Mention" and is uncollected unless the Bank's board of directors has adopted, prior to such extension … a detailed written statement giving the reasons why such extension of credit is in the best interest of the Bank Source: In the Matter of Marine Bank, Wauwatosa, Wisconsin, Docket No. 04-085b (5-19-04) (emphasis added). posted at http://www.fdic.gov/bank/individual/enforcement/12213.html#HN1

End of the Line If Bank Can’t Turn Things Around: • Bank may fall below 2% critical capital threshold • The FDIC will seize such a “critically undercapitalized” bank. • The FDIC will seize a bank that doesn‘t listen to the FDIC

Bank Regulators’ Standards for Commercial Real Estate Workouts The Counselors of Real Estate2010 Midyear Meetings