Download

1 / 13

130 likes | 263 Views

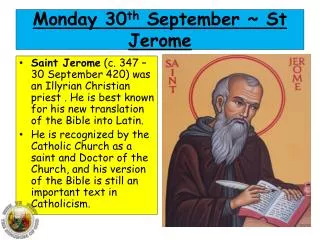

UHC :Reaching the missing middle. September 30 th , 2019. Alok Kumar Adviser Health NITI Aayog AB PMJAY ,Manthan September 30 -1 October 2019. The UHC cube. Total health expenditure. Prepaid/pooled health expenditure. Fragmented Risk Pools/ Payers. B illio n I N R s ( 2015 ). 4,980.

E N D

UHC :Reaching the missing middle September 30th, 2019 Alok KumarAdviser HealthNITI Aayog AB PMJAY ,Manthan September 30 -1 October 2019

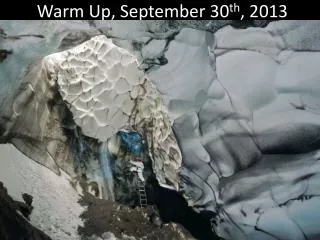

The UHC cube Total health expenditure Prepaid/pooled health expenditure

Fragmented Risk Pools/ Payers BillionINRs(2015) 4,980 5,000 4,500 4,000 3,500 -63.3% 3,150 3,000 2,500 2,000 131 84 136 1,500 20 21 67 36 143 46 233 1,000 716 67 120 10 500 0 TotalHealthExpend. OOPs PrivateEmployer PrivateOwned Publicowned CGHS Railroads*Defense OthergovernmentemployeeSHI ESIS StateVoluntaryHealthSchemes NHM OtherCentralHE PMJAY(2019) RSBY StatePublicHealth&Health CoverageCommerc.Commerc. NationalandStateNon-ContributoryPoCoenletders(PublicSubsidies) National and State Non-Contributory Pooled (Public Subsidies) NotPooled NationalandStateContributoryPooled Source:ICHSSteamanalysisbasedonmultiplepublicandinternationalsources(NationalHealthProfile2017,NationalHealthAccounts2015,Union,ESISreports)

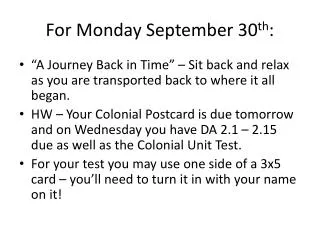

Fragmentation of Providers Large (>10) Medium (6-10) 2% % Distribution of Private Enterprises by Number of Workers Small (2-5) Single Source: Shailender Kumar (Dec 2015) Private sector in healthcare. Delivery market in India: Structure, growth and implications. Institute for Studies in Industrial Development

High OOP, High rates of Impoverishment Proportion of population pushed below the $1.90 ($ 2011 PPP) poverty line by out-of-pocket health care expenditure (%) 0.0 Russian Federation Sri Lanka Indonesia Egypt, Arab Rep. Thailand Mexico Brazil World Nepal China India Source : World bank Data Data source: World Bank Data

The case for the Missing Middle Missing Middle 80-85% population in this segment don’t have any health expenditure support. They are not covered by any public insurance scheme also More likely to fall into poverty due to catastrophic health expenditure % persons who do not have any health expenditure support for each quintile class of UMPCE ~90% of Low Income population don’t have any health expenditure support. But are likely to be covered by PMJAY Population rich enough to pay out of pocket or having Private Insurance Bottom 20% people (Poorest) Next 20% Next 20% Next 20% Top 20% people (Richest) Data source: NSSO data 2014. Data shown as a weighted average of urban and rural data UMPCE : Usual Monthly Per Capita Expenditure

The current offerings do not address the need for the ‘Missing middle’ Why focus on ‘missing middle’? • Formal sector and higher income • Commercial insurance • ESI • Risk of falling into poverty, or large catastrophic expenditure. Critical to avoid as this segment is key for economy • Could be dumped back to public sector, by insurance companies as risk increases with age • Could appropriate large share of government subsidies (national and state schemes) which should be first targeted to the poor • High nature of Informality likely to persist in Indian Economy (>80% of workers are informal in India), unlike in OECD countries, with development • ‘Missing middle’ - Informal non poor, near poor • Commercial insurance (limited) • Informal Poor • PMJAY, state schemes • Public facilities

Situation for middle India (informal non poor) today Covered today Not covered • Inadequate coverage: Multiple exclusions, waiting periods of 3-4 years, retail offerings preferably to the healthy and the young population • High premium contributions– More than Rs.15,000 per annum for a cover of Rs.5 Lakh for a family of 3 • 1.5-2x higher than group insurance • >10x higher than PMJAY • Low claims payout for individual health segment No adequate product at right price offered – Covers only IPD and day care with waiting periods Distribution limited to tier I and II cities mostly No incentives to join contributory schemes vs using fully subsidized healthcare

Design elements • Standardized, simple PMJAY+ product offering • Channeled through choice of contributory insurers via enrollment of groups • Some Government support/subsidy to stabilize the product for middle India • An institutional mechanism to ensure quick roll out • Strong governance and regulations to ensure success

Approach COLLABORATION & CONSULTATIONS EXPERIMENTATION & INNOVATION • IRDAI • Insurers (general, life, health, ESI) • Professional Groups • Digital companies • Experts • Others • Group enrollment for informal middle India • Right benefits package • Low cost distribution, exchanges • Reduced overhead costs • ..

Indirect signs of classical market failure in competing private health insurance AggregateClaimsbyAge,Gender,andDisease2014,suggestfocusonlowriskpopulationandin-patientcare,incontrasttotheoveralldemographicandBurdenofDiseaseprofileofIndia Age >70 66-70 61-65 56-60 46-55 36-45 26-35 16-25 [6-15] 0-5 Male Female TOTAL 600000 400000 200000 0 0 200000 400000 600000