Download

1 / 26

260 likes | 454 Views

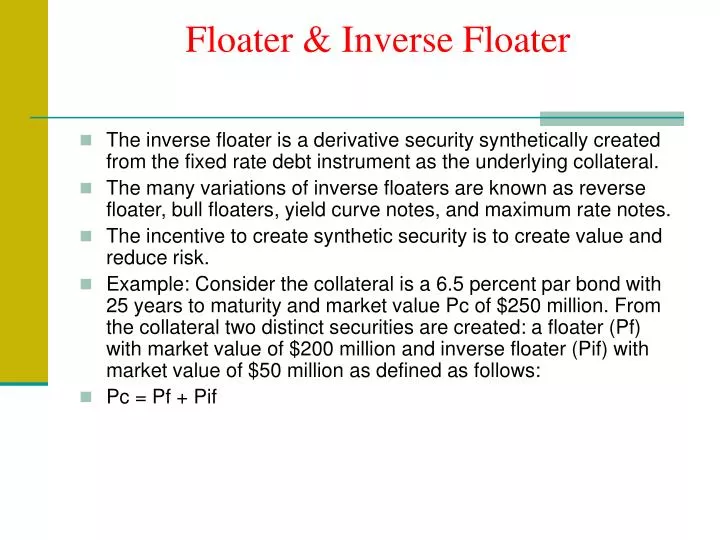

Floater & Inverse Floater. The inverse floater is a derivative security synthetically created from the fixed rate debt instrument as the underlying collateral. The many variations of inverse floaters are known as reverse floater, bull floaters, yield curve notes, and maximum rate notes.

E N D

Floater & Inverse Floater • The inverse floater is a derivative security synthetically created from the fixed rate debt instrument as the underlying collateral. • The many variations of inverse floaters are known as reverse floater, bull floaters, yield curve notes, and maximum rate notes. • The incentive to create synthetic security is to create value and reduce risk. • Example: Consider the collateral is a 6.5 percent par bond with 25 years to maturity and market value Pc of $250 million. From the collateral two distinct securities are created: a floater (Pf) with market value of $200 million and inverse floater (Pif) with market value of $50 million as defined as follows: • Pc = Pf + Pif

Suppose the coupon of the floater is set as follows: • LIBOR +1 ½ % • The coupon of inverse floater is set to take into account the amount of floater relative to an inverse floater known as leverage factor L, the index (LIBOR) as well as a constant term (q) as is defined as follows: • q – L (Index) • The floater coupon is capped and zero floor is imposed on inverse floater coupon so that weighted average coupon WAC is no greater than 6.5 % the coupon of the collateral. • WAC= .80 [LIBOR +1 ½ %] +. 20[q – 4 (LIBOR)]

Example • Orange County Retirement Fund invested in interest rates futures betting the rates are expected to go down. • It also invested heavily in the highly leveraged inverse floater. • The rates continued to go up forcing significant margin calls as the interest rate futures plummeted due to rising interest rates in 1994 and the fallout resulted in a loss of $1.7 billion. • The fund sued Merry Lynch as an investment adviser. • The inverse floater is structured to help an active portfolio manager the opportunity to bet in the direction of interest rates, particularly those with greater price sensitivity with a higher leverage factor.

Barbell & Bullet • The portfolio underlying the fixed rate is considered a bullet, while the derivative portfolio of the floater and the inverse floater is known as barbell. The barbell portfolio is embedded with option and possesses a positive convexity that is highly valuable in the active bond portfolio management. • Suppose the duration of the floater created from the collateral is six months and the duration of the inverse and the collateral is as follows: • Duration • Inverse 61.75 • Floater ½ • Collateral 12.35 • Dif = (L+1) Dc . Pc / Pif

Active Portfolio Management • Brandywine Asset Management fund has invested 5 percent of its portfolio of $1.8 billion in the inverse floater with the current yield of 18 percent. • The higher yield in the inverse floater is due to falling interest rates that make the inverse floater such an attractive issue at this time. • The portfolio manager, betting that interest rates are expected to go down, presumably has acquired the inverse floater and it appears that his bets have paid off. • However, the earlier example of Orange County reveals the other side of the bet where rates move in the direction opposite to the bet.

Creating Synthetic Fixed Rate • The investor synthetically creates a 6.5 % fixed rate by buying a floating rate note and simultaneously selling a swap that pays floating rate and receives a fixed rate as shown in the above Exhibit. • The synthetic fixed rate enables investors to adjust the portfolio position by terminating (unwinding swap) without the cost of selling and repurchasing the entire amount of the principal.

Prepayment risk • Prepayment risk exposes the investors into two types of risk: • Extension risk • Contraction risk • The extension risk arises as the pass-through underlying mortgage pays slowly as the interest rate rises. When interest rates rise, the prepayments decline, as it does not payoff to prepay the mortgages. In this scenario, as the underlying mortgage debt price falls due to rising interest rates, the price of the pass-through securities falls even more as prepayment slows. The slower prepayment under a rising interest rate scenario contributes to extension risk that is undesirable to pass-through class of securities. • For example, banks and other financial intermediaries that raise capital in the short end of the market and invest in long-term debt. The assets are long term and their liabilities are short term creating a mismatch. The pass-through security is long term in nature and exposes the financial institutions to extension risk. • Insurance companies find pass-through unattractive, exposing them to extension risk in the event rates increase and prepayment slows. • The cash flows from the pass-through securities are uncertain, making them undesirable from assets liability management for institution such as insurance companies.

Contraction risk • The contraction risk arises in the event of falling interest rates as prepayments speeds up. • The fall in interest rates makes refinancing attractive for mortgagors or individual relocating and selling property. • The pass-through life therefore shortens and subjects the investors to contraction risk. • When the rates fall the price of the plain vanilla bonds increases, however, the price of the callable pass-through is not expected to go up as much. • The upside potential of the pass-through securities is truncated due to negative convexity as the prepayment slows, this callable bond is expected to be called. • Pension funds are exposed to contraction risk, as the nature of their liabilities is generally long term. The pass-through exposes the long-term investors to reinvestment rate risk.

Mortgage and Asset Backed Derivatives • Pooling single or multi-family mortgages creates the pass-through security in a portfolio by repackaging their cash flow into new securities and selling the new securities to the broader classes of investors. • The objective of repackaging an ordinary coupon paying instrument into shares or participation certificate through securitization is aimed: • at increasing liquidity, • marketability, • as well as realizing economic rent, as investment banking firm realizes the difference between what it pays for the securities in the pool and what it receives from the shares when shares are sold in the secondary market.

PO & IO Derivatives • Stripped mortgage-backed securities issued in early 1987 separated coupons from the corpus of the underlying pool of mortgages into a class of securities known as: • interest-only (IO) securities, with all of the principal going to another class known as • principal-only (PO) securities.

Example • Suppose the pass-through underlying the collateral is $200 million mortgage securities with 6.5 percent coupon and priced at par with maturity of 25 years. • The PO backed by this pass-through is worth $50 million, since it is a deep-discount bond. The PO investors (who receive no coupon interest) will receive a dollar return of $150 million ($200 million principal less initial investment of $50 million) over 25 years, or 5.7 percent annualized return.

Collateralized Mortgage Obligations CMO • The CMO and stripped mortgage backed securities SMBS are derivatives created by redistributing cash flow underlying pass-through (the collateral) to transfer and mitigate: • The prepayment risk from some classes of bonds to other classes based on an established payment rules for disbursing the coupon interest payments, prepayments and principal repayments to different classes. • The contraction and extension risks, to the classes of bonds with risk-return characteristics different to that of the underlying mortgages that is appealing to the needs and expectations of certain segments of investors.

Sequential Pay Structure • The principal payment accrues sequentially to the first class until it is paid off, while the coupon is paid to all of the classes. • Once the first class is retired the next class receives all of the principal and prepayments until it is paid off, while other classes only receive coupon interest based on their outstanding principal in the underlying collateral at the beginning of the period.

Commodity Linked Debt • Commodity-linked debt or equity instruments provide the issuer the opportunity to hedge against the volatility of the price of its input and reduce and stabilize the volatility of its earnings. • Revenue and profit of the producer of the underlying commodity tends to go up or down as the commodity price goes up or down worldwide in good economic time or periods of recession.

Gold Linked Note • Freeport-McMoran Copper and Gold Inc. raised $230 million in 1993 by issuing gold-denominated preferred stocks for $37.8 per share in exchange for 1/10 of an once of gold in its funding of the expansion of the its gold mining operation. • To manage its exposure to commodity price changes the firm essentially sold forward 600,000 ounces of its gold at the current price of $378/ounce for delivery at the maturity of the preferred stock. • At the inception of the contract, the issuer issued 6 million shares of preferred stock at $37.80 that amounts to forward sale of 600,000 ounces of gold for $230 million net of underwriting cost.

Emerging Market Bonds & Socks • The emerging market economies provide fertile ground for diversification for investors on both sides of the Atlantic. The process of actually buying shares in these economies raises few problems for investors and portfolio managers. For example, • The bid/ask spreads are usually much higher for shares of stocks/bonds in smaller newly developing economies. • The foreign exchange rate risk adds an additional element of uncertainty for individuals and portfolio managers. • The host country may also impose capital control in order to mitigate the flight of capital that hinders the asset allocation decisions. • Total return swap Can mitigate all of the above problems. • Example: Suppose College Retirement Equity Funds (CREF) portfolio manager wishes to allocate and diversify $5 billion into stocks of emerging market economies. CREF may swap total return on its growth portfolio with that of the return on the Morgan Stanley International Index (MSII) for the emerging market over the next two years with semiannual settlement. For example, if the annualized return on NASDAQ is equal to 11 percent and the corresponding return on the MSII is equal to 14 percent, the CREF portfolio manager will receive $75 million from the counterparty.

Catastrophe Bonds • Property casualty companies issue catastrophe bonds by shifting and reallocating business risk to large classes of investors. • The yield on these bonds is slightly higher than on comparable bonds, and the bonds are embedded with an option that reduces the coupon interest or principal payments to investors should theissuer suffer large losses due to earthquake or hurricane.

Liability Management • For most corporations in the United States and for multinationals, liability management is intended to reduce the cost of borrowing through innovative derivatives. • The objectives of liability management are to organize the firm’s financing activities by blending various classes of securities to achieve the lowest cost of financing.

Exposure Management • Bank B has $200 million variable rate loan in its assets portfolio; the rate is to be reset in the next three months. The revenue is exposed to interest rate risk. • Bank B wishes to manage its exposure by selling 3x6 FRA with notional principal of $200 million. Exhibit 9.13 presents the cash flow stream that is exchanged.

Swaption • Swaptions are a right, not an obligation, to enter into interest rate swaps sometime in the future over a given period. • For example, a 2x3 swaption at a strike price of 6.75 percent is a one-year swap starting in two years, where the buyer is expecting interest rates to go up in two years. • If the rates go up the buyer of put swaption forces the seller to pay floating and receive strike price (fixed rate of 6.75 %). • Call swaptions: The buyer of the call swaptions however, has the right not an obligation to enter into an interest rate swap to pay floating and receive fixed where the buyer is expecting the rates in the future to fall below the strike price forcing the seller to pay the strike price and receive the floating rate. The seller is obligated to pay fixed and to receive float in the event the rates go down.

Spread on Treasury Yield Curve • The yield spread on the Treasury bonds and Treasury notes is expected to flatten in the next three months. • A portfolio manager buys Treasury bonds March 2003 futures and simultaneously sells Treasury notes futures for delivery in March 2003. • The ratio spread or the hedge ratio has to be estimated as the underlying futures respond differently to changes in interest rates, as the volatility of the Treasury bonds is greater than that of its Treasury notes. • The portfolio manager buys Treasury bonds March 2003 futures at 111-19, or $111.59375, and simultaneously sells Treasury notes March 2003 for113-29, or $113.90625 as quoted by the Wall Street Journal on October 12. • To estimate the ratio spread, dollar value of 1 basis point (DVO1) needs to be calculated for both futures and weighted by the respective cheapest to deliver (CTD) conversion factors for 10- and 30-years bonds. The conversion factor for the 10- and 30-year CTD bonds, respectively, is equal to .8568 and .9353 for March 2003. The DVO1 is estimated as follows: • DVO1: Treasury bonds • P = $111,430.82 Yield = 5.24 • P = $111,758.01 Yield = 5.22 • P = 327.19 327.19 /2 = $163.59 • DVO1: Treasury bonds: $163.59 / .9353 = $174.91 • DVO1: Treasury notes • P = $114,048.88 Yield = 4.26 • P = $114,224 Yield = $.26 • P = $175.12 $175.12/2 = $87.56 • DVO1: Treasury notes: $87.56/.8568 = $102.19 • Ratio spread or the hedge ratio is estimated as follows: • h = DVO1: Treasury bonds/ DVO1: Treasury notes • $174.91/$102.19 = 1.71