Download

1 / 3

30 likes | 36 Views

EVERYONE PREFERS THE FHA MORTGAGE WITH A 3.5 PERCENT DOWN PAYMENT

E N D

EVERYONE PREFERS THE FHA MORTGAGE WITH A 3.5 PERCENT DOWN PAYMENT FHA loans are popular among first-time home purchasers because they address many of the new buyers’ issues. Do you have a bad credit score? FHA loans are available with credit scores as low as 580. Do you have a lot of school debt? FHA loans allow for more debt than other types of mortgages. Don’t have much money set out for a down payment? The FHA demands a 3.5 percent down payment. Of course, there is a penalty to these benefits in the shape of higher borrowing costs. However, for many first-time home purchasers, the compromise is worthwhile. If you’re looking to borrow money for a home, here are some reasons why you’ll love a Utah FHA refinance: Increased Seller Concessions Allowance Fha mortgage 3.5 down payment loans enable property sellers to pay up to 6% of the purchase price toward closing costs and other prepaid goods involved with securing the loan. When a borrower puts less than 10% down on a conventional loan, seller contributions are limited to 3%. This raised threshold might lower your out-of-pocket expenses when buying a property.

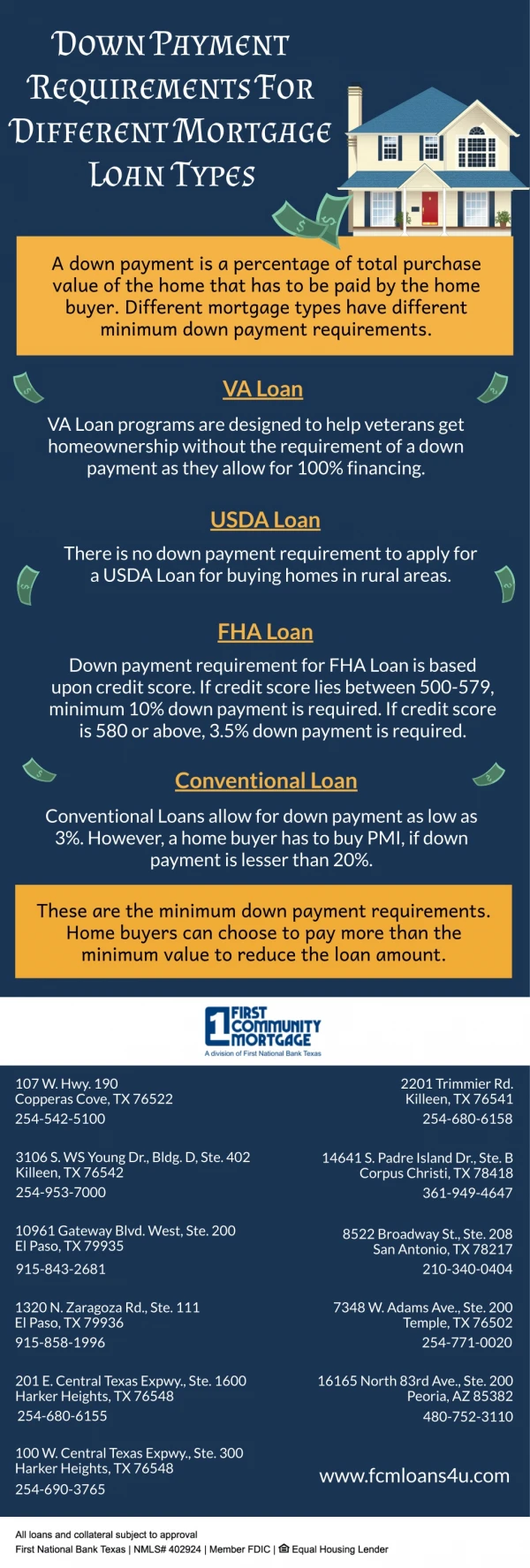

Bankruptcy or foreclosure do not exclude you from obtaining an FHA loan After a foreclosure or bankruptcy, you can qualify for FHA home loans Utah in as short as two years and three years, respectively. As a borrower, you must reestablish excellent credit or opt not to incur new credit commitments, as well as demonstrate your capacity to handle your financial affairs. The FHA is intended to make homeownership a reality Lenders like USDA home mortgage or FHA loans because they are HUD-insured. Because HUD establishes the lending rules, some qualification criteria may be less stringent than traditional loans. Excluding delayed student loan payments from debt-to-income ratios and lowering minimal credit scores are two instances. The yearly premiums for FHA insurance have just been lowered Borrowers who apply for FHA loans are eligible for the newly lowered yearly premiums offered by the FHA. HUD predicts that the decreased rates will save over two million FHA homeowners an average of $900 per year. The FHA requires a small down payment (as low as 3.5 percent of the purchase price) When you apply for an FHA loan or VA home mortgage, you also have options for approved sources of down payment. Personal savings, a gift from a family member, or approved government down payment aid programs are all possible sources. Most traditional plans need at least a 5% down payment and, depending on credit, up to a 20% down payment. An FHA loan can be used to purchase a fixer-upper The FHA understands that not all houses are ready to move into. Especially for first-time homebuyers wanting to buy at the lower end of the price range. That is why the FHA 203k loan was formed. The FHA 203k loan assists house purchasers who intend to upgrade appliances, replace the flooring, repair a roof, or paint rooms, among other things. These repairs can be funded in conjunction with the mortgage. This implies that you don’t have to pay for house repairs using cash. You may pay them off with your mortgage instead. There are no “specific rules” for qualifying for FHA loans Unlike other low- and no-down payment mortgage programs, there are no specific requirements to use an FHA home loan. Borrowers must be military members, for instance, to qualify for a zero-down VA loan. Furthermore, the USDA loan with no down payment requires property purchasers to live in less congested communities while keeping under specified income levels.

Even the typical HomeReadyTM mortgage, which allows for a 3% down payment, limits household income or census tract. The FHA does not need this type of verification. FHA mortgages are available regardless of where you reside, what you do, or how much money you make. FHA loans are available to anybody. Those with less-than-perfect credit can apply for FHA loans Borrowers with credit scores of 500 or above will be eligible for FHA loan insurance. Most other lending options need a minimum credit score of 620. FHA loans need a credit score of 500-579 and a down payment of 10% or higher. If you want a lower down payment — 3.5 percent to 9.9 percent — you must have a credit score of at least 580. The FHA provides the best and clearest road to homeownership for many house purchasers, particularly those at the bottom of the credit rating scale. FHA mortgage rates are frequently “below market” FHA mortgage rates are generally 12.5 basis points (0.125 percent) or lower than conventional 30-year fixed-rate mortgage rates. This difference can be considerably greater for loans with down payments of 10% or less and borrowers with less-than-perfect credit. It is not rare for first-time home purchasers, whose credit scores are frequently lower than normal, to receive an FHA mortgage rate quotation of more than 100 basis points (1.00 percent) cheaper than a similar conventional rate. View & Download Original Source @ https://www.staplesgroupmortgage.com/everyone-prefers-the-fha-mortgage- with-a-3-5-percent-down-payment/