Download

1 / 130

1.54k likes | 3.07k Views

Federal Retirement Benefits for FERS Employees. The National Institute of Transition Planning. intro. Bob Braunstein, Federal HR Consultant. 1966-1997 Federal Government Predominantly in Treasury Department Bureaus (IRS, ATF, OCC); full range of HR positions

E N D

Federal Retirement Benefits for FERS Employees The National Institute of Transition Planning intro

Bob Braunstein, Federal HR Consultant • 1966-1997 Federal Government • Predominantly in Treasury Department Bureaus (IRS, ATF, OCC); full range of HR positions • Expertise in Staffing, Classification, Benefits, Employee Relations, Retirement Counseling, FERCCA • 1997 to present – consultant to Federal agencies for Human Resources Projects through: • National Academy of Public Administration • Kelly Anderson and Associates • Economic Systems Inc. • National Institute of Transition Planning • Latest HR projects have been with NASA, Navy, HHS, NIH, TSA, Peace Corps • FERCCA Project (OPM, USPS and DOJ cases) • Developed eSeminar application for ESI

1-1 Four sources of financial security

Module 1: Your Retirement Benefit 1-2 Step 1: Determine your eligibility Step 2: Determine your basic retirement benefit Step 3: Identify age factors that affect a benefit Step 4: Determine whether to pay a civilian deposit Step 5: Consider survivor benefits Step 6: Determine whether to pay a CSRS redeposit Step 7: Determine whether to pay a military deposit

Determine Your Eligibility 1-3 • Your retirement system • The type of retirement • Your age • Your years of creditable service

The Federal Retirement Systems 1-4 1920 1987 1984 CSRS CSRS Interim FERS/ CSRS Offset

1-5 Employee and Agency Contributions: FERS 7% to Retirement (.8 to FERS; 6.2 to SS/Matched by Agency)/TSP match $ $ $ $ $ $ $ $ Social Security CSRDF TSP

Retirement Options 1-6 • Immediate (regular) • Early (VERA or discontinued service) • Disability • Deferred • Special provisions

Creditable Service 1-7 • Civilian Service • Military service • Includes: • Part-time • Breaks in service of 3 days or less • LWOP (up to 6 mo) • Intermittent • Uncovered service (with exceptions) • Refunds for CSRS • CSRS Handbook (chaps 20-23)

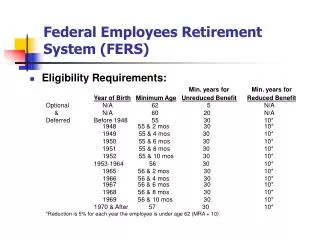

FERS Minimum Age and Service Requirements 1-9 MRA based on year born (chart on page 1-9) ORDS • LEO and FF (age 57 mandatory.) • ATC (age 56 mandatory.)

Steps for Planning Your Retirement Benefit 1-10 1: Determine your eligibility 2: Determine your basic retirement benefit 3: Identify age factors that affect a benefit 4: Determine whether to pay a civilian deposit 5: Consider survivor benefits 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

Length of Service High 3 Determine Your Basic Retirement Benefit 1-10 Formula Retirement Benefit (CSRS, CSRS Offset, FERS)

Length of Service • Retirement Date – SCD = Length of Service • Not always same as leave SCD • All months have 30 days; add one day for last day worked 1-11 31 2 19 Certified Summary on pages 1-12 and 1-13

Calculate Your High-3 Salary 1-16 Your high-3 salary is your highest average basic pay over any consecutive 3-year period in Federal service.

Regular pay Locality-based pay Premium pay Night differential for WG Special Pay for recruitment/retention Annual leave lump sum Bonuses and overtime Night differential other than WG Travel allowances Geographic/post differential Basic Pay 1-16 YES No Tip: Your % ret. Deduction is a direct fraction of your allowable base pay

Determine the Beginning of High-3 Period 1-16 31 12 2011

Determine Your Average High-3 Salary 1-17 Reference Chart on Page 1-18 for factors

FERS: Calculate Your Basic Benefit 1-22 SP PT FS

FERS Retiree Annuity Supplement 1-23 Social Security Retirement • Must be under FERS • Must be under 62 • Not age-reduced retirement • LEOs/FFs/ATCs at MRA • Earnings Tested

Disability Retirement (FERS) 1-25 • Combination of civil service and Social Security benefits • Benefit is recalculated after the first 12 months and at age 62

Example: FERS Disability 1-25 • Age: 42 • Years of service: 20 • High-3 salary: $45,000 • Denied a SS disability benefit* • *If SS disability approved: • Fully Offset by disability annuity during first year • 60% offset during years until age 62 • At age 62, no longer offset

Cost-of-Living Adjustment 1-27 Based on the change in the CPI – p 1-27 chart • Provided for all CSRS retirees • Based on CPI • Immediate • Prorated per retirement date • Generally provided for FERS retirees 62 and older • Diet Colas • Usually 1% less • Prorated per date eligible

The Best Day to Retire 1-28 & 29 Best Day for CSRS Employees • Discontinued Service and Disability – annuity begins next day • Disability – better of date after separation or last day of pay • Deferred – annuity begins on 62nd birthday for CSRS; for FERS 1st day of month after 62nd birthday or MRA (with 10 yrs or more) Best Day for FERS Employees

Steps for Planning Your Retirement Benefit 1-30 1: Determine your eligibility 2: Determine your basic retirement benefit 3: Identify age factors that affect a benefit 4. Determine whether to pay a deposit 5: Consider survivor benefits options 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

FERS MRA + 10 1-33

Steps for Planning Your Retirement Benefit 1-35 1: Determine your eligibility 2: Determine your basic retirement benefit 3: Identify age factors that affect an benefit 4. Determine whether to pay a civilian deposit 5: Consider survivor benefits options 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

Determine Whether to Pay a Civilian Deposit 1-35 • A deposit is payment for civilian service that was not covered by retirement deductions (temporary service, military service, WAE service) • Consider your retirement system, dates of service, and how much you owe

FERS Civilian Deposits 1-38 Two time periods: • Pre 1/1/89 (must be paid for credit in both SCD and annuity) • On or after 1/1/89 (deposits cannot be made; service will not count)

Example: FERS Civilian Deposit Pre-1/1/89 1-38 • 1 year of nondeduction • Total base pay = $20,000 • Deposit = $800 • Employee’s high-3 salary = $65,000

Steps for Planning Your Retirement Benefit 1-39 1: Determine your eligibility 2: Determine your basic benefit 3: Identify age factors that affect a benefit 4. Determine whether to pay a civilian deposit 5: Consider survivor benefits options 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

Consider Survivor Benefits 1-39 • Survivor Elections: • Spousal survivor benefit • Insurable interest survivor benefit • Other survivor benefits: • Child’s survivor benefit • Lump-sum payments to beneficiaries

Spousal Survivor Benefit 1-40 May elect maximum, partial, or no benefit • The retiree does not need to be in good health at the time of election • Generally, the marriage must have lasted at least 9 months or birth of first child • Ends if the survivor remarries before age 55, unless married for 30 years or more

Example: FERS Spousal Survivor Benefits 1-41 Retirement Benefit = $20,000

Death in Service Benefit for Spouse 1-42 • A lump-sum benefit of $28,093, plus 50% of your final salary with less than 10 years of service (but at least 18 mos.) • Survivor benefit paid with 10 years or more of service

Insurable Interest Survivor Benefit 1-44 Retiree must: • Be in good health • Not retire under disability • Can name only one person at time of retirement: • A close relative (OPM assumes relationship) • Someone who depends on retiree for support (affidavit needed)

Children’s Survivor Benefit 1-45 • Payable to dependent children upon the death of a retiree (page 1-45) • An automatic benefit; no election is required

Lump-Sum Payment (of Retirement Contributions) 1-46 If no one entitled to survivor annuity • Retirement contributions go to beneficiaries on SF-3102; or • Your widow or widower • Your children or their descendants • Your parents • Executor your will • Other next of kin Other beneficiary forms in Appendix B on page B-3

Steps for Planning Your Retirement Benefit 1-47 1: Determine your eligibility 2: Determine your basic retirement benefit 3: Identify age factors that affect a benefit 4. Determine whether to pay a civilian deposit 5: Consider survivor benefits options 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

Determine Whether to Pay a Redeposit (for CSRS Component) 1-47 Two time periods: • Pre 10/1/90 • On or after 10/1/90 • Time counts for SCD even if not paid • Affect on annuity will differ by period (p 1-47)

Example: CSRS ComponentRedeposit Pre 10/1/90 1-48 • Age 60 • Refund = $10,000 • Redeposit = $25,000 (principal and interest owed) * From Present Value Factor Table on p 1-49

Example: CSRS Redeposit Post 10/1/90 1-48 & 49 • Refund = $10,000 for 10 years of service • Redeposit = $25,000 (principal and interest owed) • Employee’s high-3 salary = $65,000 VC

Steps for Planning Your Retirement Benefit 1-50 1: Determine your eligibility 2: Determine your basic retirement benefit 3: Identify age factors that affect a benefit 4. Determine whether to pay a civilian deposit 5: Consider survivor benefits options 6: Determine whether to pay a CSRS redeposit 7: Determine whether to pay a military deposit

Example: FERS Military Service Deposit 1-51 & 52 • Total base pay = $20,000 • Deposit = $1,800 (principal and interest owed) • Employee’s high-3 salary = $65,000

Retired From the U.S. Military 1-53 • Combine military with civilian service • Waive military retirement annuity • May or may not benefit by combination

Example: Retired from the Military (FERS) page 1-54 • Total base pay = $200,000 • Deposit = $18,000 • Military pay = $15,000 (principal and interest owed • High three average salary: $65,000