Download

1 / 4

0 likes | 10 Views

small business loans<br>

E N D

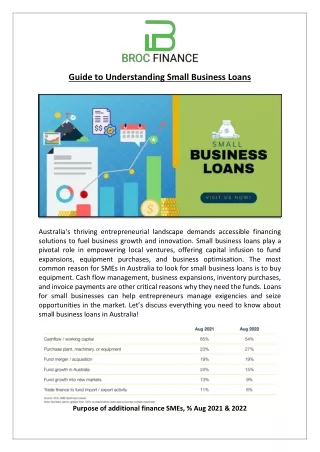

Navigating the Landscape: A Comprehensive Guide to Small Business Loans for Entrepreneurs Starting and growing a small business is an exciting venture, but it often requires a significant amount of capital. While many entrepreneurs invest their savings into their business, it may not be enough to cover all the expenses involved. This is where small business loans come into play - they provide the much-needed financial support to fuel growth and success. However, navigating the landscape of small business loans can be daunting, with various options and lenders available. In this comprehensive guide, we will walk you through the essential aspects of Trade Funding small business loans, empowering you to make informed decisions for your entrepreneurial journey. Understanding Small Business Loans A small business loan is a financial product designed to help businesses meet their working capital needs, expand operations, purchase equipment, or fund new projects. These loans can be obtained from traditional banks, credit unions, online lenders, and government-backed programs. The terms and conditions of each loan can vary significantly, so it's essential to understand the various options available to find the one that suits your business requirements.

Navigating the Landscape: A Comprehensive Guide to Small Business Loans for Entrepreneurs Types of Small Business Loans Term Loans: Term loans are the most common type of small business loans. They provide a lump sum amount that is repaid over a specific period, typically with a fixed interest rate. These loans are suitable for long-term investments such as purchasing real estate, equipment, or making significant business expansions. Line of Credit: A business line of credit functions more like a credit card. It provides access to a set credit limit, and you can draw funds as needed. Interest is only charged on the amount borrowed, making it an excellent option for managing cash flow fluctuations or short-term needs. Equipment Financing: This type of loan is specifically designed to help businesses purchase equipment or machinery. The equipment itself serves as collateral, which often simplifies the application process and may result in more favorable interest rates. Invoice Financing: If your business deals with unpaid invoices, invoice financing can be beneficial. Lenders advance a percentage of the invoice amount, and once your customer pays the invoice, the lender deducts their fees and releases the remaining amount to you. SBA Loans: The U.S. Small Business Administration (SBA) offers various loan programs to support small businesses. These loans are partially guaranteed by the SBA, making them more accessible to entrepreneurs who may not qualify for traditional bank loans. Assessing Loan Eligibility Before applying for a small business loan, it's crucial to assess your eligibility. Lenders evaluate several factors to determine if your business qualifies for a loan. Key considerations include: Credit Score: A strong personal and business credit score increases your chances of loan approval and may lead to more favorable terms. Aim to maintain a good credit history by paying bills on time and managing debts responsibly. Business History and Revenue: Lenders often prefer established businesses with a track record of generating revenue. However, some lenders cater to startups and newer ventures, so explore different options based on your business's age and revenue. Collateral: Some loans, especially traditional bank loans, require collateral to secure the loan. Collateral can be assets like real estate, equipment, or inventory. It provides the lender with a form of security if you cannot repay the loan.

Navigating the Landscape: A Comprehensive Guide to Small Business Loans for Entrepreneurs Business Plan: A well-crafted business plan demonstrates your understanding of the market and your business's future prospects. A solid plan can instill confidence in lenders about your ability to repay the loan. Debt-to-Income Ratio: Lenders consider your business's debt-to-income ratio, which compares your business's debts to its income. A lower ratio is generally more favorable to lenders. Choosing the Right Lender Once you know what type of loan you need and have assessed your eligibility, it's time to choose the right lender. Different lenders have varying approval criteria, interest rates, and loan terms. Here are some common types of lenders to consider: Traditional Banks: Banks offer a sense of security and stability but may have stricter eligibility requirements and longer approval processes. Online Lenders: Online lenders provide quick and convenient application processes with varying loan options. They are often more flexible with eligibility criteria, making them suitable for businesses with less established credit histories. Credit Unions: Credit unions are member-owned financial cooperatives that may offer competitive rates and personalized service to their members. SBA-Approved Lenders: If you're interested in an SBA loan, find an approved lender who can guide you through the application process. Preparing Loan Application Documents To increase your chances of loan approval, it's essential to prepare the necessary documents and information. Common documents required for a small business loan application include: Business Plan: A comprehensive business plan outlining your company's history, market analysis, financial projections, and growth strategies. Financial Statements: Profit and loss statements, balance sheets, and cash flow statements provide insights into your business's financial health. Personal and Business Tax Returns: Lenders often require both personal and business tax returns to assess your financial history.

Navigating the Landscape: A Comprehensive Guide to Small Business Loans for Entrepreneurs Bank Statements: Recent business bank statements demonstrate your cash flow and financial activity. Legal Documents: Incorporation papers, licenses, contracts, and other legal documents may be necessary for the loan application. Collateral Documentation: If you're applying for a secured loan, prepare documents related to the collateral you're offering. Comparing Loan Offers Before finalizing a loan, it's essential to compare offers from multiple lenders. Pay attention to the interest rates, loan terms, repayment schedules, and any additional fees. Consider the overall cost of borrowing to make an informed decision. Remember, the cheapest option may not always be the best fit for your business's needs and financial situation. Conclusion Securing a small business loan can be a crucial step in achieving your entrepreneurial goals. By understanding the various loan options, assessing your eligibility, and carefully choosing the right lender, you can navigate the landscape of small business loans with confidence. Remember, thorough preparation and research are key to obtaining the financing your business needs to thrive. Take the time to evaluate your options, prepare a solid loan application, and watch your small business flourish with the support of the right loan.